| Home | Log In | Register | Our Services | My Account | Contact | Help |

You are NOT currently logged in

Eureka Mining - time to spell it out (EKA)

tallsiii

- 11 Apr 2005 14:30

- 11 Apr 2005 14:30

EKA are expecting to mine 3.8 million lbs of Molybdenum this year. For the more sceptical amongst you, read this to confirm:

http://moneyam.uk-wire.com/cgi-bin/articles/200412150700023844G.html

They own the mine and the molydbenum in it has been independently varified as stated in the announcement linked above.

Molydbenum currently trades at around $38.50 per lb, you can check this at:

http://www.monterrico.co.uk/s/MetalPrices.asp

so do the sums 3.8m x $39.25 = $149m = 82m

Eureka Mining's market cap is 26m

In 2006 they expect to pull over 10,000 tonnes (20m lbs) of Moly out of that mine.

On top of all that they have recently aquired a mine in Russia with estimated contained metal of 3.32 million tonnes of copper, 3.26 million

ounces of gold and 98.9 million pounds of molybdenum. They hope to complete the feasibility study for this one in 2006:

http://moneyam.uk-wire.com/cgi-bin/articles/200501130700033169H.html

http://moneyam.uk-wire.com/cgi-bin/articles/200412150700023844G.html

They own the mine and the molydbenum in it has been independently varified as stated in the announcement linked above.

Molydbenum currently trades at around $38.50 per lb, you can check this at:

http://www.monterrico.co.uk/s/MetalPrices.asp

so do the sums 3.8m x $39.25 = $149m = 82m

Eureka Mining's market cap is 26m

In 2006 they expect to pull over 10,000 tonnes (20m lbs) of Moly out of that mine.

On top of all that they have recently aquired a mine in Russia with estimated contained metal of 3.32 million tonnes of copper, 3.26 million

ounces of gold and 98.9 million pounds of molybdenum. They hope to complete the feasibility study for this one in 2006:

http://moneyam.uk-wire.com/cgi-bin/articles/200501130700033169H.html

PapalPower

- 07 Dec 2005 12:02

- 142 of 215

News due soon I think.

tallsiii

- 08 Dec 2005 11:29

- 143 of 215

Has anyone phoned the company to recently? I am sure that Bartley or Foo might be able to either confirm or dispel rumours that are going around at the moment.

PapalPower

- 09 Dec 2005 08:15

- 144 of 215

The anti Celtic Resources rumour mill are hitting Foo's VOG and EKA with lots of negative stories, like the one recently on EKA about permits. Now they are having a go at VOG again I see.

A conspiracy going on ?

Anyway, good top up time with the price of EKA now and Molybednum production on line and generating cash in Q1 06.

A conspiracy going on ?

Anyway, good top up time with the price of EKA now and Molybednum production on line and generating cash in Q1 06.

PapalPower

- 11 Dec 2005 06:05

- 145 of 215

Major Shareholders

Celtic Resources Holdings PLC 15.02%

Gartmore 5.57%

Henderson Global Investors Ltd 4.18%

JP Morgan 4.18%

RAB Capital 3.83%

RCM 3.11% (Holdings of M James and D Bartley)

Directors

Kevin Alfred Foo 1.923%

David Bartley 1.198%

Malcolm Raymond James 1.151%

Andrzej S Sliwa 0.605%

Jonathan Scott-Barrett 0.177%

Presentation Link

Celtic Resources Holdings PLC 15.02%

Gartmore 5.57%

Henderson Global Investors Ltd 4.18%

JP Morgan 4.18%

RAB Capital 3.83%

RCM 3.11% (Holdings of M James and D Bartley)

Directors

Kevin Alfred Foo 1.923%

David Bartley 1.198%

Malcolm Raymond James 1.151%

Andrzej S Sliwa 0.605%

Jonathan Scott-Barrett 0.177%

Presentation Link

tallsiii

- 12 Dec 2005 14:24

- 146 of 215

Maybe the person putting out the rumours is topping up also!!

PapalPower

- 13 Dec 2005 00:56

- 147 of 215

PapalPower

- 13 Dec 2005 13:37

- 148 of 215

The last 2 trades at mid price look like someone went around the MM's looking for what they would sell off at mid price to allow the MM's drop their holdings down. A positive sign that someone is interested in buying large chunks.

tallsiii

- 13 Dec 2005 16:55

- 149 of 215

Would really like to know if production is still due for Q1 2006. If I could be sure of that, then i'd probably top up.

proptrade

- 13 Dec 2005 22:43

- 150 of 215

tallsiiii...this pup has cost me a few quid!

how are things old boy?

Rgds

PT

how are things old boy?

Rgds

PT

tallsiii

- 14 Dec 2005 08:54

- 151 of 215

Hi Prop, things are good on the whole. The new issue hit this one quite badly. But at the moment there is no reason for it to be 20% below the original float price when they are now in a so much better position than they were then. They have delayed moly production from the Q4 2005 that we had expected, but if they are in line for next quarter, then they are severly underated at the moment.

PapalPower

- 14 Dec 2005 09:17

- 152 of 215

Moving up now, bid rumours hotting up for the Chelyabinsk license ???

tallsiii

- 14 Dec 2005 09:52

- 153 of 215

During writing the last post, I managed to talk myself into buying another 10K. So that explains some of the move.

What rumours are about at the moment?

What rumours are about at the moment?

PapalPower

- 14 Dec 2005 09:57

- 154 of 215

The Times one, stating they were close to buying the remaining percentage of Chelyabinsk so that EKA then holds 100% of it.

tallsiii

- 14 Dec 2005 10:22

- 155 of 215

This is cut from RNS on 15th June regarding government co-operation:

On 13th January 2005, Eureka announced the acquisition of 51% of the Chelyabinsk

Copper/Gold Project in the southern Urals region of Central Russia and, subject

to the satisfactory conclusion of a feasibility study, the Company has the

exclusive option to acquire 100% of the project.

To me it looks that if the rumour about aquiring the remaining 49% is true, then it is likely that the feasability study has arrived at a positive result.

On 13th January 2005, Eureka announced the acquisition of 51% of the Chelyabinsk

Copper/Gold Project in the southern Urals region of Central Russia and, subject

to the satisfactory conclusion of a feasibility study, the Company has the

exclusive option to acquire 100% of the project.

To me it looks that if the rumour about aquiring the remaining 49% is true, then it is likely that the feasability study has arrived at a positive result.

PapalPower

- 27 Dec 2005 14:45

- 156 of 215

Production and sale of Moly is now within three months, so January/Feb should see this go significantly higher !

PapalPower

- 28 Dec 2005 05:52

- 157 of 215

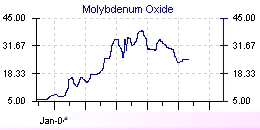

This is the only free graph I know of, its small though, but you can see the price is still well above 19$ and demand will cut in late Jan/Feb again to boost the price, so on that score its looking very good.

and from the company on Moly cash generation targets for first year (Q1 06 to Q1 07);

The Company has used a molybdenum price of US$19/lb throughout the first year and US$12/lb thereafter to calculate cash flows arising from the project.

and from the company on Moly cash generation targets for first year (Q1 06 to Q1 07);

The Company has used a molybdenum price of US$19/lb throughout the first year and US$12/lb thereafter to calculate cash flows arising from the project.

PapalPower

- 28 Dec 2005 05:53

- 158 of 215

Once Moly is being delivered the cash flow from this will give EKA a very low PER ratio going forward, so this alone is one area where there is massive upside to come.

PapalPower

- 30 Dec 2005 00:16

- 159 of 215

Excellent write up and full blown buy rating from the IC just released.

Also house broker Ambrian says Moly at 20$ should generate for EKA cash flow of 21.8m $ in 2006 and Ambrian has a price target of 175p.

Also house broker Ambrian says Moly at 20$ should generate for EKA cash flow of 21.8m $ in 2006 and Ambrian has a price target of 175p.

PapalPower

- 30 Dec 2005 07:37

- 160 of 215

Should be blue today with the IC tip.

The article also says EKA "vehemently denies" the rumours of troubles with the Chelyabinsk license.

The article also says EKA "vehemently denies" the rumours of troubles with the Chelyabinsk license.

tallsiii

- 30 Dec 2005 08:15

- 161 of 215

Cheers Papal, piled in for a load more this morning at 94/95. I pretty confident that that was the bottom. Worth getting out of bed for!

| About MoneyAM | Ts and Cs | Privacy Policy | Investment Warning | Content Standards | Corporate Solutions | Advertise With Us | Site Map | © 2026 MoneyAM |

Register now for FREE

Share Prices,

Stock Quotes,

Charts, Bulletin Boards, Indices, Watchlists, Portfolio, Market News, Research

or see our Premium Services including Level 2, Terminal and much more.