| Home | Log In | Register | Our Services | My Account | Contact | Help |

You are NOT currently logged in

Register now or login to post to this thread.

THE TALK TO YOURSELF THREAD. (NOWT)

goldfinger

- 09 Jun 2005 12:25

- 09 Jun 2005 12:25

Thought Id start this one going because its rather dead on this board at the moment and I suppose all my usual muckers are either at the Stella tennis event watching Dim Tim (lose again) or at Henly Regatta eating cucumber sandwiches (they wish,...NOT).

Anyway please feel free to just talk to yourself blast away and let it go on any company or subject you wish. Just wish Id thought of this one before.

cheers GF.

Anyway please feel free to just talk to yourself blast away and let it go on any company or subject you wish. Just wish Id thought of this one before.

cheers GF.

Fred1new

- 26 Feb 2014 09:41

- 37140 of 81564

The truth is out.

Are Haze, Manuel and RF 5th columnists?

You never know theses days.

Have to be careful

Could asked Cruella to just lock them up before being investigated and exposed.

(Probably, not the last. It may horrify the children.)

8-)

Are Haze, Manuel and RF 5th columnists?

You never know theses days.

Have to be careful

Could asked Cruella to just lock them up before being investigated and exposed.

(Probably, not the last. It may horrify the children.)

8-)

MaxK - 26 Feb 2014 09:44 - 37141 of 81564

Lets not forget Red Ed.

Fred1new

- 26 Feb 2014 09:52

- 37142 of 81564

Or the brown shirted UKIPPERS and BNPs and Daft Nigel.

What does the latter really stand for, other than himself and a few ?s?

What does the latter really stand for, other than himself and a few ?s?

goldfinger

- 26 Feb 2014 11:21

- 37143 of 81564

Borrowers warned of £600 'drastic scenario' mortgage repayments rise in 2015

The Centre for Economic and Business Research said a rate of 1.75pc by December 2015 would push up annual costs by £576

By Andrew Oxlade10:18AM GMT 26 Feb 2014

Home owners could see their mortgage payments rise by £252 a year on average by the end of next year if interest rates start rising at a moderate pace, a report forecasts.

It also forecast that a "drastic scenario" of Bank Rate at 1.75pc by the end of 2015, which it deemed feasible, would push up typical annual repayments by £576.

Research by the Centre for Economic and Business Research (CEBR) found that average mortgage payments across the UK could rise from their current monthly levels of £666 per month to £687 a month in the most likely scenario. This would add an extra £21 a month to payments, or £252 a year.

The UK Bank Rate, which has been kept at a historic 0.5pc low for five years, has helped to keep payments relatively affordable, but signs that the economy is improving have prompted speculation about possible rises being on the horizon.

• TABLES: Today's best mortgage rates

That renewed optimism has already shifted the pricing of new mortgage deals. The best five-year fixed rate has risen from 2.44pc in July to 2.95pc (available from Natwest and Woolwich).

The Financial Flexibility report, undertaken for Barclays Mortgages, assumed that the "most likely" scenario is that interest rates will rise at a moderate pace, which for its model would involve the base rate rising to 0.75pc in May 2015 and then 1% in August before edging up again to 1.25pc in November next year.

With strong differences in house prices across the UK, the extra amount of money people would find themselves paying by December 2015 under the "moderate" model of interest rate increases varied, from an extra £32 a month in London to people living in Wales and the North West projected to be paying an extra £15 a month.

Across the income groups, high and middle income earners would see the percentage of their income that is taken up by their mortgage payments remain broadly constant, at 12% and 20% respectively if there is a moderate interest rise.

But those in the lowest fifth of the income groups could see an increase in the chunk of their income that went towards mortgage payments, from around 54pc now to 55pc.

Some experts have suggested that people who are worried about the impact of interest rate rises on their mortgages could consider locking into a longer-term fixed rate deal.

But others have suggested that with house prices strongly rising in some areas, some people may find that when a shorter-term deal comes to an end, the amount of equity they have in their home will have risen enough to push them into a higher deposit bracket, which could potentially give them access to a better range of deals and offset the impact of any gradual interest rate rises.

Andy Gray, Barclays' managing director of mortgages, said: "In working with the CEBR we have tried to model the realities that UK home owners may face in the very near future.

"In the face of a rise in mortgage rates and in the cost of living, it is vital for home owners to review their current situation."

Yesterday, the Financial Conduct Authority reminded lenders of their responsibility to identify borrowers most likely to struggle with rates rise and have processes in place to ensure they are treated fairly should they fall into arrears.

---------

Here are the monthly payments that home owners could be faced with under a moderate increase in interest rates, according to the Barclays Mortgages/Cebr report, with the current monthly payments followed by those projected for December 2015 and the monthly increase in cash terms in brackets. It also includes a "drastic model", based on five rate rises, taking base rate to 1.75pc by next December:

When will the UK Bank Rate rise?

The markets currently price in the first rate rise for the second quarter of next year, so between April and June. This forecast is volatile, and only a few weeks ago suggested the first move could come as early as January.

Economists polled by Reuters earlier this month said they expect the first interest rate hike to come next year, with a majority pointing to either the second or third quarters.

Some economists believe an increase is possible toward the end of this year.

This raised anxiety in itself can raise borrowing costs – on mortgages and even on the Government's own borrowing costs. This could threaten the nascent recovery.

The Bank of England appears to have gone into overdrive to calm concerns.

Today, the Bank's chief economist, Spencer Dale, attempted to reassure the public that interest rate rises are not likely to come this year, insisting that the Bank is not even thinking about higher rates.

Speaking to BBC radio, he said rate rises will be "cautious" when they do come in order to "nurture the recovery".

He said: "We’re not planning to raise interest rates any time soon. Interest rates will have to rise at some point but not yet. And when they do they will rise very gradually and cautiously to make sure we continue to nurture the recovery we have seen in output growth and employment."

Almost simultaneously, David Miles, another member of the Monetary Policy Committee, was on BBC Breakfast and said: "We're not in a hurry to put up interest rates up. There's a lot of slack in the economy."

However, earlier this month, Mr Miles said investor expectations for a rate hike next year and for the base rate to reach 2pc by 2016 are "not unreasonable".

The Bank of England set out a new version of its "forward guidance" policy on February 12, linking its rate decisions to how quickly the economy uses up its spare capacity.

Following that Bank Governor Mark Carney told the BBC's Andrew Marr Show that a very broad recovery would be needed to trigger rate rises. He said: "The path of interest rates is going to be calibrated very carefully to ensure ... that only when we see sustainable growth in jobs, in incomes and in spending will we make adjustments."

In contrast, Martin Weale, an external member of the Monetary Policy Committee (MPC), said earlier this week that the Bank could raise rates before next May's General Election.

The Centre for Economic and Business Research said a rate of 1.75pc by December 2015 would push up annual costs by £576

By Andrew Oxlade10:18AM GMT 26 Feb 2014

Home owners could see their mortgage payments rise by £252 a year on average by the end of next year if interest rates start rising at a moderate pace, a report forecasts.

It also forecast that a "drastic scenario" of Bank Rate at 1.75pc by the end of 2015, which it deemed feasible, would push up typical annual repayments by £576.

Research by the Centre for Economic and Business Research (CEBR) found that average mortgage payments across the UK could rise from their current monthly levels of £666 per month to £687 a month in the most likely scenario. This would add an extra £21 a month to payments, or £252 a year.

The UK Bank Rate, which has been kept at a historic 0.5pc low for five years, has helped to keep payments relatively affordable, but signs that the economy is improving have prompted speculation about possible rises being on the horizon.

• TABLES: Today's best mortgage rates

That renewed optimism has already shifted the pricing of new mortgage deals. The best five-year fixed rate has risen from 2.44pc in July to 2.95pc (available from Natwest and Woolwich).

The Financial Flexibility report, undertaken for Barclays Mortgages, assumed that the "most likely" scenario is that interest rates will rise at a moderate pace, which for its model would involve the base rate rising to 0.75pc in May 2015 and then 1% in August before edging up again to 1.25pc in November next year.

With strong differences in house prices across the UK, the extra amount of money people would find themselves paying by December 2015 under the "moderate" model of interest rate increases varied, from an extra £32 a month in London to people living in Wales and the North West projected to be paying an extra £15 a month.

Across the income groups, high and middle income earners would see the percentage of their income that is taken up by their mortgage payments remain broadly constant, at 12% and 20% respectively if there is a moderate interest rise.

But those in the lowest fifth of the income groups could see an increase in the chunk of their income that went towards mortgage payments, from around 54pc now to 55pc.

Some experts have suggested that people who are worried about the impact of interest rate rises on their mortgages could consider locking into a longer-term fixed rate deal.

But others have suggested that with house prices strongly rising in some areas, some people may find that when a shorter-term deal comes to an end, the amount of equity they have in their home will have risen enough to push them into a higher deposit bracket, which could potentially give them access to a better range of deals and offset the impact of any gradual interest rate rises.

Andy Gray, Barclays' managing director of mortgages, said: "In working with the CEBR we have tried to model the realities that UK home owners may face in the very near future.

"In the face of a rise in mortgage rates and in the cost of living, it is vital for home owners to review their current situation."

Yesterday, the Financial Conduct Authority reminded lenders of their responsibility to identify borrowers most likely to struggle with rates rise and have processes in place to ensure they are treated fairly should they fall into arrears.

---------

Here are the monthly payments that home owners could be faced with under a moderate increase in interest rates, according to the Barclays Mortgages/Cebr report, with the current monthly payments followed by those projected for December 2015 and the monthly increase in cash terms in brackets. It also includes a "drastic model", based on five rate rises, taking base rate to 1.75pc by next December:

When will the UK Bank Rate rise?

The markets currently price in the first rate rise for the second quarter of next year, so between April and June. This forecast is volatile, and only a few weeks ago suggested the first move could come as early as January.

Economists polled by Reuters earlier this month said they expect the first interest rate hike to come next year, with a majority pointing to either the second or third quarters.

Some economists believe an increase is possible toward the end of this year.

This raised anxiety in itself can raise borrowing costs – on mortgages and even on the Government's own borrowing costs. This could threaten the nascent recovery.

The Bank of England appears to have gone into overdrive to calm concerns.

Today, the Bank's chief economist, Spencer Dale, attempted to reassure the public that interest rate rises are not likely to come this year, insisting that the Bank is not even thinking about higher rates.

Speaking to BBC radio, he said rate rises will be "cautious" when they do come in order to "nurture the recovery".

He said: "We’re not planning to raise interest rates any time soon. Interest rates will have to rise at some point but not yet. And when they do they will rise very gradually and cautiously to make sure we continue to nurture the recovery we have seen in output growth and employment."

Almost simultaneously, David Miles, another member of the Monetary Policy Committee, was on BBC Breakfast and said: "We're not in a hurry to put up interest rates up. There's a lot of slack in the economy."

However, earlier this month, Mr Miles said investor expectations for a rate hike next year and for the base rate to reach 2pc by 2016 are "not unreasonable".

The Bank of England set out a new version of its "forward guidance" policy on February 12, linking its rate decisions to how quickly the economy uses up its spare capacity.

Following that Bank Governor Mark Carney told the BBC's Andrew Marr Show that a very broad recovery would be needed to trigger rate rises. He said: "The path of interest rates is going to be calibrated very carefully to ensure ... that only when we see sustainable growth in jobs, in incomes and in spending will we make adjustments."

In contrast, Martin Weale, an external member of the Monetary Policy Committee (MPC), said earlier this week that the Bank could raise rates before next May's General Election.

goldfinger

- 26 Feb 2014 12:45

- 37144 of 81564

Rachel Reeves @RachelReevesMP 2m

Labour with cross-party support, is forcing a vote in the Commons this afternoon on the #BedroomTax

Labour with cross-party support, is forcing a vote in the Commons this afternoon on the #BedroomTax

MaxK - 26 Feb 2014 13:00 - 37145 of 81564

How much is this bedroom tax?

goldfinger

- 26 Feb 2014 13:26

- 37146 of 81564

The cut is a fixed percentage of the Housing Benefit eligible rent. The reduction is 14% for one extra bedroom and 25% for two or more extra bedrooms.

The Government’s impact assessment shows that those affected will lose an average of £14 a week. Housing association tenants are expected to lose £16 a week on average.

The Government’s impact assessment shows that those affected will lose an average of £14 a week. Housing association tenants are expected to lose £16 a week on average.

MaxK - 26 Feb 2014 14:23 - 37147 of 81564

Ah, so it's designed to get people to downsize?

MaxK - 26 Feb 2014 14:24 - 37148 of 81564

goldfinger

- 26 Feb 2014 14:50

- 37149 of 81564

Whos that above Hannah Soubrey MP.

Debate is on Parliament channel live now.

IDS taking a right pasting.

Debate is on Parliament channel live now.

IDS taking a right pasting.

Haystack

- 26 Feb 2014 15:06

- 37150 of 81564

Labour doing very badly in its attack on the housing benefit changes. IDS pointing out all the errors spouted by Rachel Reeves.

Overall, Labour took quite a bashing over their failure to build social housing when in power. It was the lowest level since the 1920s.

Overall, Labour took quite a bashing over their failure to build social housing when in power. It was the lowest level since the 1920s.

goldfinger

- 26 Feb 2014 15:22

- 37151 of 81564

Exit Poll shows opposition have won.

Hays stop drinking, its clouding your judgement.

Hays stop drinking, its clouding your judgement.

Haystack

- 26 Feb 2014 15:32

- 37152 of 81564

A silly debate and pointless vote. Even the Libs support the measures and it is very popular with the public. Once again Labour are on the wrong side of history.

Labour lost the vote easily by 51.

Labour lost the vote easily by 51.

cynic

- 26 Feb 2014 15:45

- 37153 of 81564

no idea what all the above is about and the vote in question, but if the gov't majority was indeed 51, then clearly labour must have been on its own in opposing the motion

i wonder how sticky concluded that black was white?

i doubt we'll never know - perhaps a conspiracy

i wonder how sticky concluded that black was white?

i doubt we'll never know - perhaps a conspiracy

goldfinger

- 26 Feb 2014 15:55

- 37154 of 81564

Tories chickened out Hays.......no doubt the Whips were very busy this morning.

Was at least 50 saying they would vote with opposition.

Spineless barstewards.

If I was an MP and any Whip came near me they would know to stay away in the future.

Was at least 50 saying they would vote with opposition.

Spineless barstewards.

If I was an MP and any Whip came near me they would know to stay away in the future.

Fred1new

- 26 Feb 2014 16:07

- 37155 of 81564

Haze,

Still in cloud cuckoo land!

Overall, Labour took quite a bashing over their failure to build social housing when in power. It was the lowest level since the 1920s.

Which silly B. sold the social housing off and stopped the money raise being put into building replacement stock?

Money was poured into building replacement schools and hospitals deliberately run down and neglected by the Nasty Party!

Still in cloud cuckoo land!

Overall, Labour took quite a bashing over their failure to build social housing when in power. It was the lowest level since the 1920s.

Which silly B. sold the social housing off and stopped the money raise being put into building replacement stock?

Money was poured into building replacement schools and hospitals deliberately run down and neglected by the Nasty Party!

MaxK - 26 Feb 2014 16:09 - 37156 of 81564

How the Government will gradually abolish the state pension

By David Craig, on February 26th, 2014

http://www.snouts-in-the-trough.com/

cynic

- 26 Feb 2014 16:24

- 37157 of 81564

sticky obviously has an inside line - aka inside leg measurement - of someone's busty PA ...... she steered him to the wrong hole so to speak!

anyway, i thought it was the EXIT poll he was gibbering on about

perhaps a busload voted twice :-)

anyway, i thought it was the EXIT poll he was gibbering on about

perhaps a busload voted twice :-)

Fred1new

- 27 Feb 2014 09:13

- 37158 of 81564

No 10 The remnants of Maggie

=======

The reappearance of Maggie

Be careful Wavy Davey she may eat you!

=======

The reappearance of Maggie

Be careful Wavy Davey she may eat you!

Fred1new

- 27 Feb 2014 09:17

- 37159 of 81564

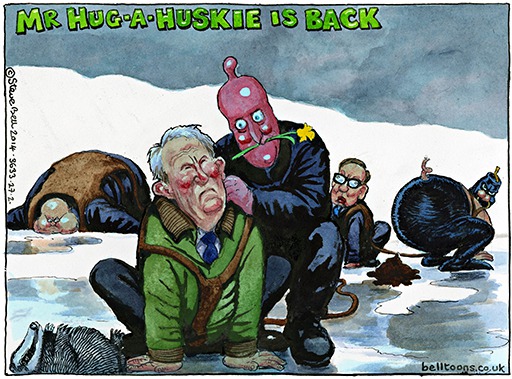

Somebody is looking for the greenest PM ever, taking his husky for a walk, looking for something else to mess up!

| About MoneyAM | Ts and Cs | Privacy Policy | Investment Warning | Content Standards | Corporate Solutions | Advertise With Us | Site Map | © 2026 MoneyAM |

Register now for FREE

Share Prices,

Stock Quotes,

Charts, Bulletin Boards, Indices, Watchlists, Portfolio, Market News, Research

or see our Premium Services including Level 2, Terminal and much more.