| Home | Log In | Register | Our Services | My Account | Contact | Help |

Eureka Mining, the prospects are good. (EKA)

PapalPower

- 05 Feb 2006 04:44

- 05 Feb 2006 04:44

Main Web Site : http://www.eurekamining.co.uk

EKA is now a Molybdenum producer in Kazahkstan, and is in the process of bringing the Chelyabinsk Copper/Gold project into production in 2008.

Latest Presentation June 2006 : Presentation Link (10MB PPT file)

Research Report : http://www.fox-davies.com/FDC_Eureka_Report_220605.pdf

26th Jan 2006 Press Commentary : Press Link

About Eureka Mining

Key contact : Mr Kevin Foo Non-Exec Chairman

E-Mail : kevin.foo@eurekamining.co.uk

Eureka Mining Plc is a UK based mining exploration and project development company, focusing on projects in the Former Soviet Union. It is the Companys view that Kazakhstan and other central Asian FSU countries represent an area of significant opportunity. This belief is supported by the quality of the portfolio of assets which Eureka has acquired including;

the Shorskoye molybdenum deposit;

the acquisition of the Chelyabinsk Copper Project; and

the advanced exploration projects of Kentau, Mykubinsk and Central Kazakhstan projects. The Mykubinsk and Central Kazakhstan polymetallic project has assets situated in northern Kazakhstan and the Kentau exploration project has identified several gold and base metal deposits.

Shorskoye Molybdenum Project:

50/50 JV with KazAtomProm, largest Kazakhstan State Mining Company

Production projected for 1st Qtr 2006

Project Finance in place

Chelyabinsk Copper Project

Production planned for 2008

Very large resource base with with 3.57Mt Cu / 4.2Moz Au

First western group into Russian Copper Heartland and consequential opportunities in base metals

Kazakhstan Exploration Projects

At the Dostyk Copper-Gold Projects in Central Kazakhstan, we have reviewed all historical data and identified at least six drill targets, with particular focus on base metal projects. During 2004, we drilled five projects and completed significant field activity on two projects, including the high priority targets Berezky Central, Maiozek, Akkuduk (porphyry style), Ushtagan (epithermal gold), Maikain, Baygustam and Burovoy (VMS). We intend to focus on the most promising of these deposits in 2005/2006.

The Kentau Project in southern Kazakhstan has undergone an extensive data review, with a comprehensive Geographic Information Systems database being created. This has enabled us to plan a focused exploration programme on previously identified targets. Drilling is expected to commence in May 2005 at two of the best targets, using a large Reverse Circulation (RC) rig.

We entered into an option agreement to acquire the Nova Dnieprovka (Nova) Gold Mine in northern Kazakhstan. However, after a thorough assessment and reinterpretation of the project, including the completion of a drilling programme, we decided not to exercise the option and purchase agreement over the Nova project.

Our exploration and assessment teams are continuously reviewing potential projects for Eureka across the FSU and only the very best are selected for further work.

__________________________________________________________________

Some figures to think about (thanks to unionhall)

Current Market cap (@ 1.37) - 36m

Chelyabinsk NPV 508m (@ $1.60 copper and $550 Gold)

Shorskoye - 10m profit p/a @ $20 Moly

Major shareholders

Latest major holder figures are, from 26.6 million shares in issue :

Celtic Resources hold 15.02%

RAB Capital hold 6.19%

Kevin Foo holds 3.43% (Director)

David Bartley holds 3.02% (Director)

Malcom James holds 1.070% (Director)

Andrzej Sliwa holds 0.76% (Director)

JSB holds 0.177% (Director)

Latest News / Links / Research Reports

Reserach Report : http://www.fox-davies.com/FDC_Eureka_Report_220605.pdf

25th April 2006 Moly Update :

http://www.resourceinvestor.com/pebble.asp?relid=19141

2006 Moly Report : http://www.golden-phoenix.com/documents/TheEconomicsofMolybdenum.pdf

____________________________________________________________________

The Company has used an average molybdenum price of US$19/lb throughout the first year and US$12/lb thereafter to calculate cash flows arising from the project.

(*Note : Molybdenum does not trade on the London Metals Exchange or any other publicly traded commodity exchange. Its price is determined solely by supply/demand in the marketplace and supply contracts. In a report dated Oct. 28, 2005, RBC Capital Markets forecast that 2006 and 2007 molybdenum prices would be approximately US$25/lb and US$15/lb, respectively [source: RBC Capital Markets, Global Base Metal Equity and Commodity Report Card, company reports].*)

How will the Moly be processed ? Eureka pulled off a deal with KazAtProm.Eureka has 15-year access to state-owned KazAtomProm's processing facilities, which will allow the company to start producing molybdenum concentrate in February.The processing plant also handles other minerals.The proximity of the plant to the Chinese border, allows for quick, cheap and simple transport links to a major demand area for Moly

Implementation and schedule of Moly production

Utilising the Stepnogorsk processing facility allows Eureka to develop the Shorskoye asset and take advantage of the buoyant molybdenum market, commencing mining in Q3 05 and saleable concentrate by Q1 06. The key project milestones are:

August 2005 - award contracts

August 2005 - first blast and ore to crusher

September 2005 - first ore to Stepnogorsk

October 2005 - first equipment to Stepnogorsk

February 2006 - concentrator commissioning (Stepnogorsk)

February 2006 - Chelyabinsk 100% purchased by Eureka

May 2006 - first production from Stepnogorsk (Skorshoye)

____________________________________________________________________

Molybdenum Information Links

http://www.freemarketnews.com/Analysis/60/3742/2006-02-10.asp?wid=60&nid=3742

http://www.gold-eagle.com/editorials_05/reser092205.html

http://321energy.com/editorials/fross/fross120605.html

http://www.cozine.com/archive/cc2005/01370511.html

At 25$ / lb Moly prices : (Shorskoye Project)

2006 Moly production = 600,000 lbs = 14.7 million dollars sales price

2007 Moly production = 1,200,000 lbs = 29.4 million dollars sales price

2008 Moly production = 1,200,000 lbs = 29.4 million dollars sales price

2009 Moly production = 1,200,000 lbs = 29.4 million dollars sales price

2010 etc etc etc

___________________________________________________________

Recent Director Buying :

Kevin Foo BUY 5,000 on 21 June 2006 @ 81p

Kevin Foo BUY 18,000 on 21 June 2006 @ 90.3p

Kevin Foo BUY 9,000 on 22 June 2006 @ 92pb>

PapalPower

- 05 Feb 2006 04:47

- 4 of 213

Extract from an 18th Jan The Australian report :

"A year ago copper was forecast to average $US1.23 a pound but came in at $US1.66 a pound. The red metal is now at a record high around $US2.15.

In a report from London last week, Credit Suisse First Boston warned that the market could be seriously underestimating the strength of the metal price outlook.

According to CSFB's scenario, mining executives remain scarred by past busts and are too focused on value, so they are reluctant to commit themselves to new mines, the costs of which have jumped 20-50 per cent in the past five years. That means supply simply won't ramp up quickly enough and the market is in for further metal price spikes in the next two years.

CSFB estimates that in metals such as copper, zinc, nickel and aluminium new supply won't be enough to cover demand growth of 3 per cent.

"Mining executives today are too focused on returns and aren't incentivised to take risk to build new mines or smelters. Share buybacks and mergers and acquisitions are a lower-risk strategy than developing a mine with four-year lead times and the uncertainty of where prices will be once the project is finished," it says.

CSFB says that while Rio Tinto and BHP Billiton are pulling out all stops to expand iron ore production following a 71 per cent price leap last year, growth plans are generally characterised by smaller brownfield expansions rather than large new projects.

CSFB estimates that for a new copper mine to earn a 20 per cent return, it needs a long-term price of about $US1.50 a pound, up from current thinking of US90c a pound.

CSFB sees copper prices averaging a whopping $US2.30 a pound this year.

The wide range in forecasts makes it tough for investors. Diversified majors such as BHP and Rio Tinto are trading at 10-11 times earnings, which is approaching the high side, if commodity prices are peaking. But if you plug in spot prices, they are trading closer to an attractive 8 times earnings.

According to UBS, the sector's quarterly reporting season, which kicks off with Rio's production report, could trigger a fall in prices if the reports highlight continued cost pressures.

But it says any fall should be seen as a buying opportunity. "Whereas we believe the market is lagging on updating for rising costs, we believe it is also lagging on upgrading for higher commodity prices," UBS says. "

PapalPower

- 05 Feb 2006 04:49

- 5 of 213

unionhall - 1 Feb'06

Meanwhile, Phelps Dodge Senior Vice President for Marketing Arthur Miele Tuesday forecast a $2 per pound copper price during the first quarter, along with a 3.5%-4% growth in copper consumption this year. He also predicted an $18 to $25 per pound average molybdenum price during 2006 with a first-quarter average price of $22/lb.

I understand Shorskoye production mid-April.

Stockpiled ore from mining confirms required grades.

All equipment in country following delay at customs. Clear for takeoff.

Trying to force final positive confirmation re Chelyabinsk while work continues on site.

3rd Feb

David Bartley was in Russia beginning of week trying to finalise Chelyabinsk.

In all day meeting in London today.

Back in Russia next Monday and Tuesday.

PapalPower

- 05 Feb 2006 05:00

- 6 of 213

Link Click Here

PapalPower

- 05 Feb 2006 12:51

- 7 of 213

We also must not forget the bullish outlook on copper, which if Chelyabinsk news is good, then demands that EKA takes a serious re-rating upwards.

PapalPower

- 05 Feb 2006 23:07

- 8 of 213

Link for latest prices

From the link you provided :

Indium

99.99%min European market

950-990 usd/kg

Manganese Flake

99.7%min European market

1280-1330 usd/mt

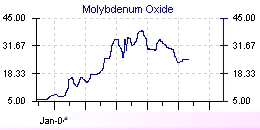

Molybdenum Oxide

57%min European market

25.5-26.5 usd/lb Mo

Selenium

99.9%min European market

31-33 usd/lb

Silicon

4-4-1 European market

1250-1280 eur/mt

Tungsten APT

88.5%min European market

265-275 usd/mtu

Vanadium Pentoxide

98%min European market

8.0-9.0 usd/lb VO5

PapalPower

- 06 Feb 2006 09:40

- 9 of 213

PapalPower

- 06 Feb 2006 15:47

- 10 of 213

silvermede

- 06 Feb 2006 16:29

- 11 of 213

Thanks for the work on this new thread, succint repository of info.

PapalPower

- 06 Feb 2006 16:39

- 12 of 213

http://www.fox-davies.com/FDC_Eureka_Report_220605.pdf

Here we go, up through 200p and more to come...............the full RNS is much longer than the highlights below and full of information !

RNS Number:9954X

Eureka Mining PLC

06 February 2006

Eureka Mining PLC

("Eureka" or "the Company")

06 February 2006

Eureka acquires 100% ownership of the

Chelyabinsk Copper/Gold Project, Russia and announces results of Scoping Study

* Ownership increased to 100% by payment of US$6 million

* Confirmation of good and unencumbered title received

* Miheevskoye Scoping study demonstrates robust economics

* NPV(10%) of US$257m and IRR of 23.6%, at US$1.00/lb copper and US$400/oz gold

* Capital cost estimate US$342m and cash costs of US$0.39/lb before credits

* Start-up scheduled for 2008

Acquisition of 100% of Chelyabinsk Copper Company

tallsiii

- 06 Feb 2006 16:47

- 13 of 213

tallsiii

- 06 Feb 2006 16:51

- 14 of 213

tallsiii

- 06 Feb 2006 17:01

- 15 of 213

So with a copper price of $1.70 and a gold price of $575, you could add 7 times $109 to the NPV of $257m. That would give a total NPV of over $1000m (580m), 17 times the current Market Cap (34m) of EKA. The copper price is in fact way above $1.70 at the moment, but using that price allows for a simple calculation.

PapalPower

- 06 Feb 2006 17:13

- 16 of 213

The figures are mind boggling, VOG had its day in the sun, now its sister company EKA to have the fun.

silvermede

- 06 Feb 2006 17:14

- 17 of 213

tallsiii

- 06 Feb 2006 17:21

- 18 of 213

PapalPower

- 06 Feb 2006 17:27

- 19 of 213

The Fox Davies reports gives target prices, and its all in the link above.

tallsiii

- 06 Feb 2006 17:37

- 20 of 213

PapalPower

- 06 Feb 2006 17:50

- 21 of 213

Some figures to think about (thanks to unionhall)

Current Market cap (@ 1.37) - 36m

Chelyabinsk NPV 508m (@ $1.60 copper and $550 Gold)

Shorskoye - 10m profit p/a @ $20 Moly

PapalPower

- 07 Feb 2006 00:09

- 22 of 213

PapalPower

- 07 Feb 2006 11:18

- 23 of 213

| About MoneyAM | Ts and Cs | Privacy Policy | Investment Warning | Content Standards | Corporate Solutions | Advertise With Us | Site Map | © 2026 MoneyAM |