| Home | Log In | Register | Our Services | My Account | Contact | Help |

Taylor Wimpey (TW.)

skinny

- 26 Jun 2014 12:12

- 26 Jun 2014 12:12

Link to old thread

About us

We are one of the UK's largest residential developers. As a responsible developer we are committed to working with local people and communities.

Company Website

Financial calendar

Recent Broker notes

BarChart Indicators

Recent Market news

Taylor Wimpey Fundamentals (TW.)

skinny

- 26 Jun 2014 12:12

- 2 of 372

midknight

- 26 Jun 2014 12:21

- 3 of 372

jimmy b

- 26 Jun 2014 15:31

- 4 of 372

midknight

- 26 Jun 2014 15:40

- 5 of 372

Skinny is just keeping everyone informed.

We're not the only ones here.

jimmy b

- 26 Jun 2014 21:14

- 6 of 372

Balerboy

- 26 Jun 2014 22:18

- 7 of 372

skinny

- 27 Jun 2014 05:36

- 8 of 372

skinny

- 27 Jun 2014 06:46

- 9 of 372

skinny

- 27 Jun 2014 07:53

- 10 of 372

jimmy b

- 27 Jun 2014 08:15

- 11 of 372

midknight

- 27 Jun 2014 13:20

- 12 of 372

jimmy b

- 30 Jun 2014 08:26

- 13 of 372

30 Jun Deutsche Bank 165.00 Buy

midknight

- 30 Jun 2014 09:40

- 14 of 372

You must have been a fan.

jimmy b

- 30 Jun 2014 09:48

- 15 of 372

midknight

- 30 Jun 2014 09:58

- 16 of 372

Surprise, surprise!

jimmy b

- 01 Jul 2014 10:01

- 17 of 372

skinny

- 02 Jul 2014 07:31

- 18 of 372

Deutsche Bank Buy 115.20 115.20 165.00 165.00 Reiterates

midknight

- 02 Jul 2014 12:24

- 19 of 372

1.54p special divi tomorrow. Jimmy

M&S cardigan on the cards.!

jimmy b

- 02 Jul 2014 16:24

- 20 of 372

skinny

- 03 Jul 2014 07:11

- 21 of 372

Jefferies International Buy 116.80 116.80 173.00 173.00 Retains

skinny

- 07 Jul 2014 07:02

- 22 of 372

Overview

We have performed strongly in the first half of 2014, with sales rates and pricing at the upper end of our expectations. We expect to report improvements in all of our key financial objectives, with good progress made towards each of our medium term targets, which we announced in May. We expect operating profit margin for the first half of 2014 to be c.16% (H1 2013: 13.1%). We remain on track to deliver an increase in operating margin of at least 300 basis points in 2014.

more....

jimmy b

- 07 Jul 2014 08:32

- 23 of 372

7 Jul Deutsche Bank 165.00 Buy

jimmy b

- 08 Jul 2014 09:20

- 24 of 372

8 Jul JP Morgan... N/A Overweight

jimmy b

- 08 Jul 2014 11:57

- 25 of 372

Thank god i was getting worried !!

hangon - 10 Jul 2014 01:14 - 27 of 372

what does "300 Basis points" mean? - is that 3%?

midknight

- 10 Jul 2014 09:41

- 28 of 372

midknight

- 11 Jul 2014 09:44

- 29 of 372

jimmy b

- 11 Jul 2014 09:54

- 30 of 372

jimmy b

- 13 Jul 2014 20:44

- 32 of 372

midknight

- 14 Jul 2014 09:36

- 33 of 372

jimmy b

- 14 Jul 2014 10:18

- 34 of 372

Fred1new

- 14 Jul 2014 11:52

- 35 of 372

Fred1new

- 15 Jul 2014 12:42

- 36 of 372

In and outside London preferably with numbers?

skinny

- 15 Jul 2014 16:48

- 37 of 372

midknight

- 18 Jul 2014 09:06

- 38 of 372

jimmy b

- 21 Jul 2014 15:49

- 39 of 372

21 Jul Deutsche Bank 165.00 Buy.

jimmy b

- 23 Jul 2014 08:45

- 40 of 372

midknight

- 23 Jul 2014 09:19

- 41 of 372

midknight

- 23 Jul 2014 09:20

- 42 of 372

jimmy b

- 25 Jul 2014 08:24

- 43 of 372

25 Jul Deutsche Bank 165.00 Buy.

midknight

- 25 Jul 2014 12:01

- 44 of 372

Jimmy, Jefferies beats Deutsche.

jimmy b

- 25 Jul 2014 12:04

- 45 of 372

midknight

- 28 Jul 2014 10:22

- 46 of 372

skinny

- 30 Jul 2014 07:18

- 47 of 372

Highlights

· Strong progress made towards medium term targets for the Group:

o Operating profit margin* up 300 basis points to 16.1% (H1 2013: 13.1%)

o Return on net operating assets** up 350 basis points to 17.8% (H1 2013: 14.3%)

o Tangible net asset value per share† increased by 9.5% to 73.6 pence (H1 2013: 67.2 pence)

· Completed 5,766 homes across the UK, up 11%, with a 10% increase in total average selling price to £206k

· Acquired 4,336 plots in the UK short term land market in quality locations

· Worked with communities, planners and landowners to convert a record 7,195 plots from the strategic pipeline in order to develop much needed new homes across the UK

· Contributed c.£116 million to local communities across the UK via planning obligations

· Maintenance dividend up 9% reflecting increase in net assets

· 2015 cash return increased by £50 million to £250 million

midknight

- 30 Jul 2014 09:57

- 48 of 372

Plus Deutsche repeats 165p.

midknight

- 30 Jul 2014 10:44

- 49 of 372

cynic

- 07 Aug 2014 12:17

- 50 of 372

jimmy b

- 07 Aug 2014 12:35

- 51 of 372

midknight

- 12 Aug 2014 11:21

- 52 of 372

Taylor Wimpey divi H1: xd 20 Aug - payday 25 Sept = 0.2400 GBX

jimmy b

- 12 Aug 2014 11:26

- 53 of 372

----------------------------

Yup that was the last one .

skinny

- 21 Aug 2014 13:15

- 54 of 372

jimmy b

- 21 Aug 2014 20:26

- 55 of 372

midknight

- 22 Aug 2014 10:17

- 56 of 372

Jimmy - Deutsche back today after three weeks' holiday:

Buy with no TP.

skinny

- 22 Aug 2014 10:35

- 57 of 372

jimmy b

- 22 Aug 2014 11:24

- 58 of 372

midknight

- 05 Sep 2014 10:15

- 59 of 372

midknight

- 08 Sep 2014 12:01

- 60 of 372

skinny

- 13 Oct 2014 12:38

- 61 of 372

Deutsche Bank Buy 108.45 109.00 165.00 165.00 Reiterates

midknight

- 13 Oct 2014 12:51

- 62 of 372

optomistic

- 13 Oct 2014 14:40

- 63 of 372

Fred1new

- 13 Oct 2014 16:30

- 64 of 372

What is up with TSB?

midknight

- 29 Oct 2014 10:57

- 65 of 372

Fred1new

- 04 Nov 2014 18:36

- 66 of 372

It seems to be breaking upwards out of its consolidation, or side ways trading pattern on a relatively tight market to-day. Volume is with it.

I have it marked for about TP 150, but it does not owe me anything and may jump earlier.

Fundies support it, if reports true.

(Bit surprised about breaking now, but DYOH.)

goldfinger

- 04 Nov 2014 18:51

- 67 of 372

Its all gone luvvy up on the top thread CHAR

skinny

- 11 Nov 2014 07:07

- 68 of 372

midknight

- 11 Nov 2014 10:23

- 69 of 372

Numis: Buy - TP: 145p

Panmure Gordon: Hold - TP: 116p

jimmy b

- 11 Nov 2014 10:28

- 70 of 372

midknight

- 12 Nov 2014 10:09

- 71 of 372

Credit Suisse : Neutral - TP: 136p

Beaufort Securities: Buy - TP: N/A

JP Morgan Cazenove: Overweight - TP: 150p

Deutsche has also weighed in, playing the same record - must be a bit worn now.

midknight

- 21 Nov 2014 10:11

- 72 of 372

Liberum Capital : Buy - TP: 130p (realised today)

Deutsche Bank ; the usual now without TP

Fred1new

- 21 Nov 2014 10:45

- 73 of 372

Try TP of 160 on PE of 10 and "promised" EPS.

midknight

- 26 Nov 2014 09:48

- 74 of 372

Nov 26: Goldman Sachs: Conviction Buy - TP: 210p

cynic

- 27 Nov 2014 13:42

- 75 of 372

just noticed that sp has just broken into new all-time high

Fred1new

- 27 Nov 2014 13:45

- 76 of 372

Ssssh!

goldfinger

- 27 Nov 2014 14:25

- 77 of 372

TW. look nailed on for FTSE100 entry.

List is announced on wed,physical change happens 2 weeks after.

You can bet tracker funds are already buying it up for entry and those short buying back.

goldfinger

- 27 Nov 2014 14:25

- 78 of 372

TW. look nailed on for FTSE100 entry.

List is announced on wed,physical change happens 2 weeks after.

You can bet tracker funds are already buying it up for entry and those short buying back.

midknight

- 04 Dec 2014 10:12

- 79 of 372

Liberum Capital 130.00 Buy

Panmure Gordon 120.00 Hold

Citigroup 137.00 Buy

Deutsche Bank 165.00 Buy

Fred1new

- 04 Dec 2014 14:17

- 80 of 372

145 first!

8-)

midknight

- 12 Dec 2014 12:07

- 81 of 372

Citigroup: Buy - TP: 144p

Deutsche: same tune

Fred1new

- 29 Dec 2014 11:50

- 82 of 372

StockMarketWire.com

midknight

- 09 Jan 2015 11:09

- 84 of 372

Fred1new

- 09 Jan 2015 12:00

- 85 of 372

That is not saying Jefferies are incorrect, but looking at earning "projections" and promised "yield" I would have a high valuation.

But scanning around it seems that many of the "builders" have been downgraded. =

===

The downgrade may be based on UK economic expectancy.

Anybody know what is Jefferies record like in this area is?

But I know less than Manuel. 8-{

cynic

- 09 Jan 2015 12:35

- 86 of 372

given that the country certainly needs many more houses and, whatever you may say when flying your political banner, the economy is certainly on the up and assuredly much stronger than elsewhere in europe

with that in mind, i am seriously considering adding MBH to my sipp, though i have a natural aversion to MM-only stocks

skinny

- 09 Jan 2015 12:43

- 87 of 372

midknight

- 09 Jan 2015 12:50

- 88 of 372

the stocks Jefferies has savaged are down considerably, some drastically.

Fred1new

- 09 Jan 2015 13:16

- 89 of 372

I may be unsure about the economic future of UK at the moment, but think it is improving. My real gripe is that it could be better than it is, and the vicious "austerity" application was not the best route to take over the last 4 years.

My feelings about TW. are similar to yours and it is one of my biggest holds from well back and I also hold SBs. which I increased earlier this am.

I have my legs crossed routinely.

cynic

- 09 Jan 2015 13:21

- 90 of 372

legs x'ed? .... have you had your psa levels checked recently?

Fred1new

- 09 Jan 2015 14:23

- 91 of 372

-------------------------

Anyway.

"(Reuters) - Britain's housing market cooled further in the three months to December as house prices rose by 7.8 percent compared with the same period last year, the smallest increase since last January, mortgage lender Halifax said on Thursday.

In December alone, prices rose by a stronger-than-expected 0.9 percent after a 0.5 percent increase in November, marking the biggest monthly increase since July.

Economists had expected prices to rise by 8.0 percent on the year and 0.3 percent on the month, according to a Reuters poll.

Halifax reiterated that it expects house price growth to moderate this year to between 3 and 5 percent.

"The deterioration in housing affordability as a result of rising house prices, earnings growth that has been consistently below ... inflation until very recently and speculation of an interest rate rise, have combined to temper housing demand since the summer," said Martin Ellis, Halifax's housing economist.

The Bank of England has welcomed signs that Britain's housing market is cooling off after double-digit price gains in the middle of last year, restrained at least in part by new controls on mortgage lending.

Halifax's quarterly rate of house price growth slowed to 0.3 percent, the lowest reading since November 2012.

Last week Nationwide, another mortgage lender, said house prices rose at the slowest annual rate in more than a year, but it expected the market to recover in 2015 if the economy improves as expected.

(Reporting by Andy Bruce; Editing by William Schomberg and Toby Chopra)"

cynic

- 09 Jan 2015 14:33

- 92 of 372

skinny

- 09 Jan 2015 15:45

- 93 of 372

skinny

- 12 Jan 2015 07:02

- 94 of 372

Trading Statement

Overview

Pete Redfern, Chief Executive, commented:

"As we enter 2015, we are encouraged by the more balanced market conditions, with a lower rate of price growth, which should create a healthy and more sustainable housing market. This is good news for homebuyers and underpins our confidence in developing and growing our business.

Taylor Wimpey starts the year in an excellent position and whilst the global economic outlook is uncertain, in the UK we have an environment of sensible mortgage regulation and a reduced risk of UK interest rate increases in the near term. Overall we believe that the market and political risk for our sector is balanced and will allow Taylor Wimpey to continue to make significant progress towards our medium term targets."

UK current trading

During the second half of 2014 we saw a return to a healthier and more balanced housing market after a very strong first half of the year. The UK housing market continues to grow and, since our interim management statement on 11 November 2014, we have continued to see positive signs, with prices increasing slowly as previously described. This is underpinned by solid consumer confidence and good mortgage availability and affordability.

Against this backdrop, and in line with our strategy, we have continued to grow steadily and sustainably, delivering increased completions and creating additional value.

In 2014, total home completions increased by 6% to 12,454 (including our share of joint venture completions), up from 11,696 in 2013, of which 17% were affordable home completions (2013: 18%). Our net private reservation rate for the full year was 0.64 homes per outlet per week (2013: 0.62) with cancellation rates of 14% still at low levels (2013: 13%).

Average selling prices on private completions increased by 11% to £234k (2013: £210k). This increase is both a result of our underlying shift to better quality locations and capturing market sales price increases. Our overall average selling price has increased by 12% to £213k (2013: £191k).

We enter 2015 with a record order book, which has increased in value by 12% to £1,397 million as at 31 December 2014 (31 December 2013: £1,246 million), excluding joint ventures, driven largely by the strength of private reservations. This order book represents 6,601 homes (31 December 2013: 6,627 homes). We view this as the optimum size for the business at this point in the cycle.

Land portfolio, planning and outlets

The short term land market remained balanced and disciplined throughout 2014. As stated previously, whilst we continue to source and invest in short term value-creating land opportunities at similar margins to 2013, we have reached our optimal short term landbank size and so our strategy is to maintain, rather than grow, this proportion of our landbank.

The strength and quality of our strategic land pipeline is a key differentiator for Taylor Wimpey. We are particularly pleased to report a record performance during 2014, where we converted over 9k plots from the strategic pipeline into the short term landbank.

We enter 2015 with 305 outlets (31 December 2013: 314), with the decrease due to faster outlet closings in a healthier market and the time required to meet additional planning permission requirements to start working on site. We expect the total number of outlets to increase in 2015, reflecting our success in the land market and our continued focus to get newly acquired sites and phases opened properly and efficiently.

Spain current trading

The Spanish market remains stable. Our newly acquired sites performed well during 2014 due to their better quality locations and have driven a significant improvement in performance. During 2014, we completed 164 homes (2013: 118) at an average selling price of €250k (2013: €229k). The total order book as at 31 December 2014 stands at 233 homes (31 December 2013: 195 homes). The Spanish business will deliver an improved operating profit* for 2014 (FY 2013: £0.1 million operating profit*).

Group financial position

The Group will report an improved full year operating margin of slightly over 400 basis points ahead of FY 2013 operating profit* margin (FY 2013 13.6%).

We are pleased to report that we ended the year with net cash of c.£113 million, which is slightly ahead of expectations and significantly ahead of the prior year (31 December 2013: £5.4 million net cash). This is largely as a result of outperformance in underlying trading, whilst at the same time continuing to invest in our landbank as we approached our optimal scale.

Outlook

We welcome the Government's Autumn Statement announcement of a reform of Stamp Duty Land Tax payments to a more progressive system, which we believe will help more homebuyers to get onto and move up the property ladder. With the upcoming General Election in May, housing continues to remain high on the political agenda with recognition of the importance of housebuilding to the economy and the need for more quality homes in the UK. Whilst the macro economic outlook is uncertain, with a reduced risk of UK interest rate increases in the near term and sensible mortgage regulation, we believe that the market and political risk for our sector is balanced as we enter 2015, and the outlook remains positive.

We start the year in an excellent position, with our active sites and future outlets in great quality locations where people want to live. Our strategy has been and remains to deliver ongoing and sustainable increases in volume and margin over the medium term. We are confident that in current market conditions we can deliver significant progress against these objectives in 2015.

2015 is the first year of our 2015 - 2017 medium term targets, which we announced in May 2014. We are well placed to make a strong start to 2015 and are confident that we will continue to demonstrate significant progress through the year.

* Operating profit is defined as profit on ordinary activities from continuing operations before net finance costs and exceptional items, after share of results of joint ventures.

-Ends-

midknight

- 12 Jan 2015 12:13

- 95 of 372

JP Morgan : Overweight - TP: 150p

Panmure Gordon: Hold - TP: 120p

Liberum Capital: Buy- TP: 130p Buy

Citigroup: Buy - TP: 144p

Deutsche Bank: Buy - TP N/A

skinny

- 29 Jan 2015 15:52

- 96 of 372

HARRYCAT

- 03 Mar 2015 08:19

- 97 of 372

Taylor Wimpey has hiked its FY pretax profit to £468.8m, from £306.2m. Revenue was £2.69bn, from £2.3bn. Its total maintenance dividend was 1.56p a share, from 0.69p, with the final dividend at 1.32p, from 0.47p.

CEO Pete Redfern said 2014 was an excellent year for Taylor Wimpey, delivering a 54% increase in operating profit whilst contributing £300m to communities via planning obligations, providing key infrastructure, education and affordable housing.

"The beginning of spring selling season has seen trading at the better end of expectations. Customer confidence is high with good levels of employment and an affordable mortgage environment.

"The UK housing market remains healthy and we are very confident in our ability to maximise returns on our investments whilst continuing to invest in the underlying quality of the business.

"We believe that the current strong performance can be sustained and improved and therefore we have proposed a doubling of the 2014 maintenance dividend pay-out to the top end of our dividend policy range."

Looking ahead, Redfern said:

"We are currently operating in a housing market underpinned by a significant structural demand and supply imbalance. Housing remains high on the political agenda with recognition of the importance of housebuilding to the economy and the need for more quality homes in the UK by all of the main political parties.

"Whilst there remains uncertainty around the outcome of the General Election in May, consumer confidence remains solid and is supported by healthy underlying demand, low interest rates and high levels of employment. We therefore consider that the UK near term market risk is low.

"The beginning of the spring selling season has seen both demand and trading at the better end of our expectations. Net private sales rates for the year to date (w/e 1 March 2015) of 0.70 are at healthy levels (2014 equivalent period: 0.72) and within the range we see as sustainable.

"With slower market growth, we anticipate reducing build cost pressure in 2015.

"As at 1 March 2015, we are 51% forward sold for private completions for 2015 with a strong total order book of £1,657 million (2014 equivalent period: £1,529 million). This together with our strong landbank, with over 50% of plots sourced from the strategic pipeline, positions us well for 2015 and beyond.

"We remain confident that our long term strategy, enhanced by the stretching medium term targets we announced in May 2014, will enable us to maximise the best quality returns from our investments on a sustainable basis across the housing cycle."

Fred1new

- 03 Mar 2015 16:13

- 98 of 372

Thanks for the direct to Where next for the housebuilding sector?

Interesting, I am heavy on builders and relieved not to be out on a limb.

Fred1new

- 03 Mar 2015 16:13

- 99 of 372

Thanks for the direct to Where next for the housebuilding sector?

Interesting, I am heavy on builders and relieved not to be out on a limb.

skinny

- 03 Mar 2015 16:17

- 100 of 372

midknight

- 16 Mar 2015 16:07

- 101 of 372

Goldman Sachs: Conviction Buy: TP: 202

Deutsche; Buy - TP now 173p

skinny

- 16 Mar 2015 16:17

- 102 of 372

cynic

- 16 Mar 2015 16:18

- 103 of 372

a good place to be both before the budget and the election

Balerboy

- 16 Mar 2015 18:17

- 104 of 372

Fred1new

- 16 Mar 2015 18:36

- 105 of 372

Buy both.

I hold TW since 2009 and BDEV for a shorter period.

Also, hold SBs with wide stops for trading.

skinny

- 17 Mar 2015 08:54

- 106 of 372

cynic

- 17 Mar 2015 09:00

- 107 of 372

hangon - 17 Mar 2015 11:29 - 108 of 372

What I don't understand is why on the one hand we need so many Houses, yet we ( Govs ) fail to build them. Never understood "Affordable", either - surely that means a modest multiple of Wages?, That varies across the Country...forget London/SE and elsewhere houses should be starting at £100k for a 2-bed with parking on the drive. That's hardly enough for a modern family with 2+ children and 2x cars . . . . meaning they need something like 4-bed with double garage.. ~£150k - but with land in such short supply, that price would be impossible...

Do we need to have a better/cheaper/faster method of building?

cynic

- 17 Mar 2015 13:59

- 109 of 372

just as pre-fabs were put up just after the war, and lasted many many years longer than anticipated, so now we could use 20/40' shipping containers

these are already used as temporary accommodation and offices all over the world including uk, and nor need they be visually ugly

unfortunately, and it is a sad fact, the current wannabe house owner wants (tries to demand) accommodation that is far beyond realistic expectations, let alone income

we should also be doing far more to regenerate existing but empty but (relatively) derelict stock

HARRYCAT

- 17 Mar 2015 15:38

- 110 of 372

http://www.marcityhomes.com/mar-city-homes/unique-modular-homes/

cynic

- 17 Mar 2015 15:48

- 111 of 372

a major downside is that the walls are about a foot thick, so the footprint is much greater than for a traditional house

skinny

- 17 Mar 2015 15:52

- 112 of 372

skinny

- 17 Mar 2015 15:56

- 113 of 372

{kind=link}

midknight

- 17 Mar 2015 16:01

- 114 of 372

So we're back to square one.

skinny

- 17 Mar 2015 16:03

- 115 of 372

cynic

- 17 Mar 2015 16:05

- 116 of 372

of course, first time buyers would help themselves if they weren't quite so precious with sights set on 3-4 bedrooms + garage + garden! .... oh, and of course a really nice neighbourhood with first class schools

HARRYCAT

- 17 Mar 2015 16:34

- 117 of 372

https://twitter.com/adaptcbe/status/575675323704078337/photo/1

cynic

- 17 Mar 2015 16:51

- 118 of 372

Balerboy

- 17 Mar 2015 19:04

- 119 of 372

cynic

- 17 Mar 2015 19:48

- 120 of 372

skinny

- 18 Mar 2015 06:45

- 121 of 372

Balerboy

- 18 Mar 2015 09:21

- 122 of 372

cynic

- 18 Mar 2015 09:38

- 123 of 372

The BBC visited, what is believed to be, the worlds first commercially available houses built using straw. The seven houses being built in St Bernards Road, Shirehampton Bristol, use the ModCell prefabricated straw bale panel system as the main envelope of the building.

Fred1new

- 18 Mar 2015 10:41

- 124 of 372

8-)

cynic

- 18 Mar 2015 10:48

- 125 of 372

these houses have great longevity and have now been approved for long term mortgages

:-)

Fred1new

- 18 Mar 2015 11:10

- 126 of 372

cynic

- 18 Mar 2015 11:19

- 127 of 372

it really is a very interesting concept, the only serious downside being the larger footprint required due to the wall thickness

i guess they're very cheap and probably quite easy to repair

categorically they are highly energy efficient

the basic straw bales, though they must be treated in some way, are cheap, plentiful and a renewable source

i'ld be interested to know what they do for foundations and/or how the house itself is attached to this

cynic

- 18 Mar 2015 11:27

- 128 of 372

or just look up "straw house project bristol"

skinny

- 18 Mar 2015 12:48

- 129 of 372

Fred1new

- 18 Mar 2015 13:34

- 130 of 372

kernow

- 18 Mar 2015 13:40

- 131 of 372

midknight

- 10 Apr 2015 11:09

- 132 of 372

Deutsche on 173p

Apr 10: Jefferies; Buy - TP; 189p

hangon - 22 Apr 2015 23:52 - 133 of 372

We should not forget that the "insulation" isn't the plastic/straw - rather it is the lack of air-circulation . . . if this can be reduced ( as in Thermos Flask), then the heat transfer can be surprisingly small. However, building it into a wall is "risky" IMHO, since you cannot inspect it ( Nor change anything, if a better material comes round.)

Of course the primary purpose of the wall is to support the structure - but it has a duty to keep us dry and any insulation must remain "dry" to fulfil its purpose.

Good to see the sp rise, even during the Election run-up . . . always a time of uncertainty. It would be nice to see the yield greater than 1% - that's really too little.

skinny

- 23 Apr 2015 07:08

- 134 of 372

HARRYCAT

- 23 Apr 2015 09:41

- 135 of 372

midknight

- 23 Apr 2015 09:55

- 136 of 372

Balerboy

- 08 May 2015 08:51

- 137 of 372

cynic

- 08 May 2015 10:04

- 138 of 372

however, have added BVS to my trading portfolio this morning

Nar1

- 18 May 2015 09:09

- 139 of 372

Storming ahead -

midknight

- 18 May 2015 09:55

- 140 of 372

May 21: xd for special dividend 7.68p

Balerboy

- 18 May 2015 10:03

- 141 of 372

Fred1new

- 18 May 2015 10:55

- 142 of 372

At the moment TW is my largest hold over 5 years. Restored my faith in the market.

midknight

- 26 May 2015 10:13

- 143 of 372

Fred1new

- 26 May 2015 10:15

- 144 of 372

:-)

skinny

- 26 May 2015 13:44

- 145 of 372

Balerboy

- 26 May 2015 19:21

- 146 of 372

midknight

- 28 May 2015 10:09

- 147 of 372

midknight

- 29 May 2015 16:42

- 148 of 372

16:35:07 183.50 170,703,934 UT 183.20 183.50 Buy

midknight

- 03 Jun 2015 09:48

- 149 of 372

midknight

- 06 Jul 2015 09:51

- 150 of 372

Trading statement on Wednesday.

T

midknight

- 06 Jul 2015 10:04

- 151 of 372

it has become too expensive.compared with its peers.

HARRYCAT

- 09 Jul 2015 14:57

- 152 of 372

"Our key picks in the sector are Persimmon, where we have raised 2016 EPS forecasts by c6%, Taylor Wimpey which also has very strong cash flow characteristics, and Redrow. We are especially attracted to PSN and TW which offer dividend yields of 5.9%, and 7.9% respectively. Redrow, pays a very modest dividend, but on a PE basis is the cheapest stock in the sector on 8.4x 2016E."

midknight

- 14 Jul 2015 10:02

- 153 of 372

HARRYCAT

- 29 Jul 2015 08:15

- 154 of 372

Taylor Wimpey has advanced its H1 pretax profit to £237.2m, from £197.3m. Revenue totalled £1.34bn, from £1.19bn. Interim dividend was 0.49p a share, from 0.24p a year ago.

CEO Pete Redfern commented:

"We have used the opportunity of a stable and positive housing market to make significant progress towards our medium term financial and quality objectives.

"We are confident of achieving the three year financial targets that we established in 2014, and continue to invest in recruiting and developing our people and enhancing the quality of our homes.

"In line with our strategy, we have proposed a cash return of £300 million to be paid in July 2016, which takes our total cash returns to shareholders since we started the programme in 2014 to £600 million."

Highlights:

· Strong 2015 first half performance: Completed 5,842 homes (excluding joint ventures) across the UK, with a 9.2% increase in total average selling price to £225k (H1 2014: 5,695 homes at £206k), in a resilient and growing housing market; Record contribution of £55.9k per completion (H1 2014: £45.3k per completion)

· Significant progress made towards the Group's three year medium term targets: Operating profit margin up 310 basis points to 19.2% (H1 2014: 16.1%); Return on net operating assets up 540 basis points to 23.2% (H1 2014: 17.8%); Tangible net asset value per share⬠ increased by 11.5% to 82.1 pence (H1 2014: 73.6 pence), with 15.6% growth in net assets before cash distributions; Converted 45% of operating profit* to operating cash flow*** (H1 2014: 27%) on a rolling 12 month basis

· Further cash return of £300 million proposed, to be paid in July 2016, 20% ahead of the 2015 payment (July 2015: £250 million), reflecting increased cash generation and profitability.

midknight

- 29 Jul 2015 10:03

- 155 of 372

midknight

- 30 Jul 2015 09:57

- 156 of 372

Deutsche: Buy - Raises TP from 210p to 231p

Beaufort: Buy

JP Morgan: Overweight

midknight

- 03 Aug 2015 16:12

- 157 of 372

midknight

- 24 Aug 2015 12:00

- 158 of 372

TP raised from 190p to 220p.

Fred1new

- 24 Aug 2015 12:52

- 159 of 372

Which year?

Fred1new

- 30 Sep 2015 15:28

- 160 of 372

jimmy b

- 30 Sep 2015 15:52

- 161 of 372

Fred1new

- 18 Dec 2015 16:40

- 162 of 372

206p seems a resistance?

Think I will hold having Director Deals - Taylor Wimpey PLC (TW.)

BFN

Humphrey Singer, Non Executive Director, bought 25,000 shares in the company on the 18th December 2015 at a price of 196.60p. The Director now holds 25,000 shares representing 0.00% of the shares in issue.

Story provided by StockMarketWire.com

Director deals data provided by www.directorsholdings.comread:

-=-=-=-

Could be right!

2517GEORGE

- 18 Dec 2015 16:54

- 163 of 372

2517

Fred1new

- 19 Dec 2015 15:00

- 164 of 372

Fred1new

- 01 Mar 2016 11:58

- 165 of 372

StockMarketWire.com

Taylor Wimpey has hiked its FY pretax profit to GBP603.2m, from a profit of GBP468.8m. Revenue had improved to GBP3.14bn, from GBP2.67bn. Total maintenance dividend was 1.67p a share, from 1.56p.

It completed a total of 13,219 homes (excluding joint ventures) across the UK, up 7.5% from the prior year's 12,294 homes. There was an 8.0% hike in total average selling price to GBP230,000, from GBP213,000.

Taylor Wimpey said it had a record year-end order book representing 7484 homes, from 6601 at end-2014, with a total value of GBP1.78bn, from GBP1.4bn, excluding joint ventures

CURRENT TRADING AND OUTLOOK

"The UK housing market remained robust during late 2015 and has strengthened into the beginning of 2016. The market continues to show price growth and very good sales rates across most geographies.

"In central London, the market is stable, with flat prices and sales rates returning to a more normal level.

"The net private sales rate for the year to date (w/e 21 February 2016) is 0.77 (2015 equivalent period: 0.68). As at 21 February 2016, we are c.50% forward sold for private completions for 2016 with an excellent total order book of �2,030 million (2015 equivalent period: �1,630 million), excluding joint ventures.

"We have been successfully operating to our strategy for five years now, running the business according to our underlying principles. During that time we have invested heavily in land and people development.

"In 2015, we delivered record operating results, and returned over �308 million to shareholders by way of total dividend. Today, Taylor Wimpey has one of the largest strategic land pipelines in the sector with c.107k potential plots, together with a high-quality short term landbank of c.76k plots.

"The success of our strategy over the last five years, partially helped by a stable and positive market, has given us the opportunity to focus on continuously improving our business processes and systems, including our customer service, ensuring consistency across our 24 business units."

HARRYCAT

- 02 Mar 2016 09:05

- 166 of 372

Fred1new

- 12 Apr 2016 19:32

- 167 of 372

HARRYCAT

- 13 Apr 2016 08:34

- 168 of 372

Fred1new

- 13 Apr 2016 08:47

- 169 of 372

06-Apr-16 Charles Stanley Buy 193.70p - - Reiteration

24-Mar-16 Goldman Sachs Neutral 186.80p - 231.00p Reiteration

17-Mar-16 HSBC Buy 188.50p - 210.00p Reiteration

02-Mar-16 JP Morgan Cazenove Overweight 182.30p - 220.00p Reiteration

02-Mar-16 Canaccord Genuity Buy 182.30p - 210.00p Reiteration

From EPS projections 210- 230 (if you believe them).

Future Yield promises are good!

Shortage of housing, and drop due to over sale before recent change of taxation.

Cockeyed market due to Brexit.

Could be wrong.

Claret Dragon

- 13 Apr 2016 11:31

- 170 of 372

May be thıs ıs the top!!! For now.

2517GEORGE

- 14 Apr 2016 16:10

- 171 of 372

Fred, brokers rec's to be taken with a huge block of salt, why would they post their rec's for all and sundry to digest, is that not disloyal to their fee paying clients' ?

2517

Fred1new

- 14 Apr 2016 16:28

- 172 of 372

But this market is all over the place.

Another, interest to me is sales posted past the close.

jimmy b

- 14 Apr 2016 16:30

- 173 of 372

Fred1new

- 28 Apr 2016 09:46

- 174 of 372

Taylor Wimpey remains on track

StockMarketWire.com

Taylor Wimpey said it remains on track to deliver good progress towards all of its medium-term targets in 2016. The company was performing well against a positive housing market, it said.

"The UK housing market continues to be underpinned by good mortgage availability and employment prospects," it said in a trading update.

"As at 24 April 2016 we are c.70% forward sold for 2016 private completions, positioning us well for the remainder of the year and beyond. As expected, the rate of build cost inflation has reduced, and we continue to anticipate underlying build cost increases of 3-4% in 2016.

"We believe that the recent House of Lords amendments to the Starter Homes provisions in the Housing and Planning Bill reduce the future risk of the scheme. If passed, these changes will ensure that the Starter Homes initiative provides an incremental improvement to the housing market.

"The uncertainty surrounding the European Union (EU) referendum has not impacted trading to date, and underlying demand remains solid across all of our geographies.

"Due to our customer base and supply chain being based principally in the UK, together with our strong order book, we are well equipped to react to any potential changes in the market that may be caused by the EU referendum."

Story provided by StockMarketWire.com

hangon - 29 Apr 2016 13:59 - 175 of 372

The Annual Report sp-graph conveniently forgets these shares were close to £4 prior to 2005.

EDIT(25Jn2016)-Well "BrExit" has done for us! TW down ~30% allowed DIR Baroness to buy 2x£20k-worth - a nice discount.....

I read ( see posts below), from FT..... "....UK housebuilders – including Taylor Wimpey – have seen their share prices pare back since January after a three-year winning streak, due to concerns that foreign investors would be deterred from the property market it Britain’s left the EU....."

So it is particularly odd that TW has been so severly punished - but that's Markets for you. Did anyone else buy . . . -or maybe wait for a further fall, if/when the French get nasty?

cynic

- 29 Apr 2016 14:01

- 176 of 372

Fred1new

- 17 May 2016 08:41

- 177 of 372

http://www.ft.com/fastft/2016/05/17/taylor-wimpey-upgrades-forecast-raises-dividend/

Taylor Wimpey, one of the UK’s largest housebuilders, has upgraded its profit guidance and said it will boost its dividend payout, citing a “very positive” housing market with “high” consumer demand and confidence.

The FTSE 100 group said ahead of an investor day that it was confident in its business “against the backdrop of a strong, growing housing market”, after last month reporting that its order book was up 7.5 per cent from the same time last year.

It raised its guidance on operating profit margins to 22 per cent for the period between 2016 and 2018, and said that it will boost its total dividend payout for 2017 by 26 per cent to 13.8p a share, subject to shareholder approval. In 2015 its operating profit margin was 20.3 per cent and its total dividend payout 11p a share.

Taylor Wimpey said:

We believe that the land market is structurally different in this cycle, with fewer players and higher barriers to entry with increased upfront capital costs and expertise required to progress sites through the planning system.

The construction company said last month that its trading has been unaffected by the upcoming referendum on European Union membership, despite a series of estate agents warning of a fall-off in transactions.

UK housebuilders – including Taylor Wimpey – have seen their share prices pare back since January after a three-year winning streak, due to concerns that foreign investors would be deterred from the property market it Britain’s left the EU.

Analysts have warned that uncertainty around the referendum could damp demand for property assets just as the supply of high-end homes increases.

Fred1new

- 18 May 2016 13:00

- 178 of 372

Worth a look!

Date Broker New target Recomm.

18 May Beaufort... N/A Hold

18 May JP Morgan... 250.00 Overweight

18 May Deutsche Bank 261.00 Buy

17 May Canaccord... 210.00 Buy

17 May Peel Hunt 205.00 Hold

17 May Liberum Capital 161.00 Sell

16 May Deutsche Bank N/A Buy

10 May Canaccord... 210.00 Buy

9 May Deutsche Bank N/A Buy

4 May Canaccord... 210.00 Buy

2517GEORGE

- 19 May 2016 15:26

- 179 of 372

2517

Fred1new

- 19 May 2016 17:08

- 180 of 372

mentor - 27 Jun 2016 12:34 - 181 of 372

They have been falling heavily for the last couple days and at 115p they seem having some support at the moment

as they move up and down from 113 to 116p

jimmy b

- 27 Jun 2016 12:45

- 182 of 372

Barratt the same.

hlyeo98 - 27 Jun 2016 13:26 - 183 of 372

HARRYCAT

- 27 Jun 2016 13:44

- 184 of 372

Defensives for the moment are companies with $ earnings.

mentor - 27 Jun 2016 13:47 - 185 of 372

Had to go to the MM as a long settlement T +15 was not accepted on the Platform

jimmy b

- 27 Jun 2016 14:10

- 186 of 372

mentor - 27 Jun 2016 15:31 - 187 of 372

For the last 15 minutes the bid side has change and the DEPTH (no. orders ) is well ahead of the offer side.

I hope is the starting of a bounce back

mentor - 27 Jun 2016 16:33 - 188 of 372

The chart does not work properly and showing 112.15p, it looks like is 15 minutes behind or just stop working

cynic

- 27 Jun 2016 16:38

- 189 of 372

logic says that the markets must surely have fallen enough, but logic and reality have little correlation these times

mentor - 27 Jun 2016 16:45 - 190 of 372

2 directors bought shares last Friday and one today paying much higher prices 145, 146p and 134.76p today

mentor - 27 Jun 2016 16:49 - 191 of 372

That is a very large trade at the end

16:35:16

115.80p

11,532,827 UT

edit 11:12pm

Questor share tip: Housing stocks creaking under Brexit uncertainty

House prices have continued to rise this year, even with the EU vote looming

Marion Dakers - 27 JUNE 2016 • 6:36PM

Taylor Wimpey £1.16 -20.3p

Questor says Avoid

The dust is far from settled following the Brexit vote last Thursday, and stocks are in flux throughout banking, property and transport.

Housing developers have been on the receiving end of some particularly aggressive selling in recent days, as investors fret that the decision to leave the EU will curb domestic appetite and scare off overseas buyers.

Questor warned last week that the property sector was one of the most exposed industries to the pain of Brexit, as a vote to leave could put the brakes on demand, particularly in the booming London market.

Taylor Wimpey shares have now almost halved since May 24, when they hit 210.3p, the highest point since the 2007/8 house price bubble burst.

On Monday, the stock was also among the unhappy group that triggered the London Stock Exchange’s circuit breakers, intended to pause shares for several minutes when they become overheated.

But is the sell-off justified?

The state of the market

Taylor Wimpey had a lot going for it: a solid presence across the country, 7.5pc sales growth last year and a penchant for special dividends.

The firm makes around a third of its sales in London and the South East, and relied upon the Government’s Help to Buy scheme to subsidise mortgages for 37pc of its customers last year.

Taylor Wimpey is not the only housebuilder propped up by Help to Buy, and it’s not even the most aggressive in this slice of the market. Persimmon, for example, sold 6,110 of its 10,043 homes last year to customers with Help to Buy mortgages, while Barratt Developments reported that 31pc of its sales relied on the scheme.

However, both the international London market and first-time buyers are now particularly vulnerable to the economic lurches that Brexit brings. Analysts at Liberum said that slowing economic growth, rising long-term interest rates and political uncertainty “is like Kryptonite” for housing stocks.

Forecasters have already lowered their outlooks. The CEBR think-tank still expects prices to rise 4.5pc this year, down from a 4.9pc growth prediction before the referendum,

Even before the outcome of the vote, Berkeley Group had sent a chill through the market earlier this month by suggesting that reservations were down 20pc on uncertainty about the referendum. This warning was followed by official figures showing a 13.8pc fall in house sales in May compared to a year ago, partly because many rushed to sell in March ahead of a new 3pc stamp duty on second homes.

Supply problems

Taylor Wimpey has a land-bank of about 76,000 plots, but how quickly will it convert that potential into cash flows?

The ability to supply the housing market with more stock could also be at risk. The CEBR think-tank estimates that one in 20 construction workers come from other EU countries, who came to fill an acute skills shortage in the British building industry.

Their right to work in the UK could be limited or removed, depending on the terms of Britain’s exit from the EU, which is at least two years away. Even if their status is unchanged, the uncertainty could prompt many to leave the country for a more stable region.

Rising house prices have so far outstripped growing labour costs, which were expected to increase by 4pc this year. A crash in prices could turn this on its head.

Economic gloom

The swaps market is now pricing in a 15pc chance of UK interest rates turning negative over the course of the next year, according to Hargreaves Lansdown, signalling a period of weak economic growth and uncertainty for the housing market.

Taylor Wimpey has fortified its balance sheet to hunker down in the event of a downturn, having cut its net debt to £94.8m last year and doubled its net cash to £223.3m, even as it paid a £308m special dividend. The firm also enjoyed an operating profit margin of 20.3pc last year, meaning prices would have to take a substantial dive before it swings to a loss.

So the company seems capable of weathering economic headwinds. For now, though, the market is ill-equipped to price property stocks given so many uncertainties about supply, demand and the overall economy. Avoid.

Foxtons

£1.04 -30.5p

Questor says SELL

Foxtons’ profit warning meant the estate agent was also in the dumps on the market, losing 22.6pc and leaving the firm at its lowest ever closing price. The heady days when the stock was pushing £4 less than a year after the initial public offering in September 2013 seem like a distant memory.

Peel Hunt analysts were particularly gloomy about the firm, saying its annual profit forecast of £42m could be halved, and that even a recovery in the London market would not be enough to revive the estate agent when its competitors are eager to undercut it on commission.

The Questor column advised selling in March, after Foxton posted a 2.6pc fall in annual profits as cheaper rivals sprang up across its London heartland.

The firm has previously managed to balance falling sales with the growing lettings market, but this equation no longer works if there is a broader draining of activity from the capital city. We see no reason to take the plunge, even at the current rock-bottom price. Sell.

Claret Dragon

- 28 Jun 2016 05:47

- 192 of 372

hlyeo98 - 28 Jun 2016 10:00 - 193 of 372

mentor - 28 Jun 2016 10:01 - 194 of 372

mentor - 28 Jun 2016 10:17 - 195 of 372

Brexit vote wipes $130 bln off FTSE 100 in 2 days;

Housebuilders also fell sharply, with Taylor Wimpey, Persimmon and Barratt Developments all down 13.8 to 19.4 percent.

That is today........

LONDON MARKET OPEN: Stocks Rebound;

Among the best performers In London's blue-chip index were housebuilders. Persimmon was up 6.6%, Taylor Wimpey up 6.2%, and Barratt Developments up 5.4%. They had been amongst the hardest hit stocks in the Brexit aftermath.

hlyeo98 - 28 Jun 2016 10:34 - 196 of 372

mentor - 28 Jun 2016 11:33 - 197 of 372

you post are worth nothing to me for start, as I think you still have plenty to learn, take your own decisions not what the papers say will be my advise.

we are here to make money and so buy cheap ( I did ) and sell high (I will )

re - London financial hub

London hub will or not be as before but TW. build houses not Property for rent on the City, and many of the houses are abroad, so as £ is lower profit will be higher.

House prices over here most likely will come down as they are staggering at the moment, but that takes time and as Redrow said today they are bullish so far and more to come.

So a slow down is OK for the business and share price, but a fall from 190p to 110p, on a couple days, is for me an opportunity not to be missed.

Bye, bye

cynic

- 28 Jun 2016 15:12

- 198 of 372

i'm fortunate to have made a couple of shillings on the indices, but for sure I am only taking very small positions and being damned careful not to get greedy

there will be many good and many very scary times ahead

my gut feeling is that in the long term - ie within the next 2 years - an agreement between uk and eu will be brokered

for sure the eu plutocrats are shitting themselves, as well they might, for there is a very real danger of the whole enterprise imploding if there not some radical reform

hlyeo98 - 28 Jun 2016 16:27 - 199 of 372

mentor - 28 Jun 2016 16:40 - 200 of 372

That is why you do not make any money ( I mean losing money ) reading papers........

,,,,,,,, and I make plenty with my own ideas that make sense

mentor - 28 Jun 2016 16:45 - 201 of 372

for the day

122.10p +6.30p +5.44%

hlyeo98 - 28 Jun 2016 17:28 - 202 of 372

cynic

- 28 Jun 2016 17:41

- 203 of 372

mentor - 28 Jun 2016 17:45 - 204 of 372

Well we know a ... Hurrah, that not have even balls, mind you of steel

hlyeo98 - 28 Jun 2016 17:52 - 205 of 372

cynic

- 28 Jun 2016 18:15

- 206 of 372

with regard to this particular stock, i reckon it's one of the better housebuilders - and also TEF - and do so in my sipp for the longer term

if you don't hold already (not for quick profit) then perhaps consider doing so, the timing being difficult to judge - ie there could be many bad days in the coming weeks and months

hlyeo98 - 29 Jun 2016 08:16 - 207 of 372

jimmy b

- 29 Jun 2016 08:26

- 208 of 372

mentor - 29 Jun 2016 08:46 - 209 of 372

You have nothing to agree, stop talking bull sh!t, - cynic is telling you to buy TEF, that I played all the time,

last time late May I come out with over 10% gain in two weeks.

cynic

- 29 Jun 2016 11:21

- 210 of 372

i hold both TEF and TW. but not for short-term trading

much as i am deeply relieved to see this sharp rally, i am wondering if it has about run its course for now

Balerboy

- 29 Jun 2016 11:27

- 211 of 372

mentor - 29 Jun 2016 11:28 - 212 of 372

cynic

- 29 Jun 2016 12:02

- 213 of 372

meanwhile have done nicely (in a modest way) from trading DAX and DOW long over the last few days

have now encashed all as i have sunshine waiting for me

mentor - 29 Jun 2016 15:13 - 214 of 372

mentor - 29 Jun 2016 15:31 - 215 of 372

TEF Telford Homes . 293.75 10.54%

TW. Taylor Wimpey 132.10 8.28%

RDW Redrow ....... 325.10 8.19%

PSN Persimmon ... 1,429.00 6.32%

BDEV Barratt Devel. 404.10 6.12%

BDEV Barratt Devel. 402.10 5.54%

CRST Crest Nicholson 359.50 4.72%

mentor - 29 Jun 2016 16:49 - 216 of 372

Once again someone wants the stock or most likely more than one.

16:35:09

132.90p

7,374,197 UT

CC

- 29 Jun 2016 19:31

- 217 of 372

It is my view that whilst the housing and construction sector will be held back somewhat, it doesn't result in this sort of fall.

So, I have to decide where to sell and that I'm struggling with.

The trades on all the builders suggest and tonight's UT trades suggest to me this is going higher at least in the short term. There are lots of large UT trades on lots of stocks tonight - not sure if this is buyers seeing value or shorters now getting fried.

cynic

- 29 Jun 2016 21:22

- 218 of 372

hangon - 30 Jun 2016 13:47 - 219 of 372

I have TW. from lower ( ~2008 ), and am not about to cash-in at these blip-depressed levels. It will come back . . . . . yield says so.... even if any Bonus is cut short-term ( because they can, etc. )

However, for some Europe-focussed businesses there might be some hostility to Orders in the next few Months . . . . but only id we let our product quality slip as any £/$ woes assist our Exports.

Where we will be depressed is in Food/Oil/Energy costs, which wholesalers will mark-up quickly so they don't get caught . . . and having a near-need we cannot argue. Expect Tesco-Shopping and their Petrol to rise maybe 10-15% ( er, but not their Profits ! ).

Fred1new

- 30 Jun 2016 18:23

- 220 of 372

If you are not short term trader, previous two posts appear sensible.

But, if timed it was a nice trade over last month.

CC

- 30 Jun 2016 19:21

- 221 of 372

mentor - 01 Jul 2016 15:25 - 222 of 372

Taylor Wimpey plc 95.8% Potential Upside Indicated by Deutsche Bank

Taylor Wimpey plc using EPIC/TICKER code LON:TW had its stock rating noted as ‘Reiterates’ with the recommendation being set at ‘BUY’ today by analysts at Deutsche Bank. Taylor Wimpey plc are listed in the Consumer Goods sector within UK Main Market. Deutsche Bank have set their target price at 261 GBX on its stock. This is indicating the analyst believes there is a potential upside of 95.8% from today’s opening price of 133.3 GBX. Over the last 30 and 90 trading days the company share price has decreased 64.4 points and decreased 57.7 points respectively.

Taylor Wimpey plc LON:TW has a 50 day moving average of 185.07 GBX and the 200 Day Moving Average price is recorded at 189.06 GBX. The 52 week high for the stock is 211.9 GBX while the 52 week low for the stock is 109.44 GBX. There are currently 3,264,960,695 shares in issue with the average daily volume traded being 24,164,201. Market capitalisation for LON:TW is £4,272,540,538 GBP.

Taylor Wimpey plc is a national developer operating at a local level from over 24 regional businesses across the United Kingdom. The Company also has operations in Spain. Its segments include Housing United Kingdom and Housing Spain. The Housing United Kingdom segment includes North, Central and South West, and London and South East (including Central London) divisions.

hlyeo98 - 01 Jul 2016 16:06 - 223 of 372

jimmy b

- 01 Jul 2016 16:11

- 224 of 372

hlyeo98 - 04 Jul 2016 13:18 - 225 of 372

hlyeo98 - 04 Jul 2016 18:23 - 226 of 372

mentor - 08 Jul 2016 12:22 - 227 of 372

Another good day for the builders

CC

- 08 Jul 2016 21:44

- 228 of 372

colinspurr - 09 Jul 2016 10:21 - 229 of 372

Fred1new

- 09 Jul 2016 11:01

- 230 of 372

I am. 8-(

Claret Dragon

- 09 Jul 2016 11:21

- 231 of 372

Fred1new

- 09 Jul 2016 11:36

- 232 of 372

I bought back in 2009.

Also, expect to hold for next 6-12months plus.

Claret Dragon

- 09 Jul 2016 12:11

- 233 of 372

There margıns wıll erode very quıckly.

Just my take.

mentor - 10 Jul 2016 23:49 - 234 of 372

mentor - 11 Jul 2016 23:00 - 235 of 372

Absolute dividend policies

Until recently, Taylor Wimpey (LSE:TW) and Persimmon (LSE:PSN) were two dividend growth darlings. Income investors flocked to them because of their rapidly growing dividend yields and low valuation multiples. Right now, everyone is worried that dividend cuts are inevitable.

But there's no real risk of dividend cuts in the short term. Both housebuilders have very strong cash balances and very little debt on their balance sheets. Both companies also have absolute dividend policies based on excess capital on their balance sheets rather than pegged to future earnings.

A dividend cut in the longer term may not be inevitable either. While investor demand in the commercial property sector has taken a very big hit, the residential market is quite different. Long-term fundamentals are better for the residential market because there remains a chronic housing shortage. The number of new houses being built remains well below their pre-recession highs, and that's unlikely to change any time soon.

Housebuilders can also do more to conserve cash and prioritise dividends by reducing investment in land banks, delaying new construction and cutting back on share repurchases. Taylor Wimpey and Persimmon already have very large strategic landbanks, with both companies having around six years of supply at current build rates. What's more, Taylor Wimpey and Persimmon's 20%-plus margins mean they can withstand a modest house price shock and remain very profitable.

For 2016, shares in Taylor Wimpey have a prospective dividend yield of 7.8%, while Persimmon's shares yield 7.3%.

mentor - 12 Jul 2016 08:47 - 236 of 372

Well ahead once more after the overdone mark down

a very strong order book just now 150 v 100

mentor - 12 Jul 2016 09:23 - 237 of 372

mentor - 12 Jul 2016 10:21 - 238 of 372

a gain of 37.20p or 32.92 % on 11 working days

cynic

- 12 Jul 2016 11:17

- 239 of 372

amazingly high volume today (already 56m+), but suspect it's just a freaky day rather than anything of note

HARRYCAT

- 13 Jul 2016 11:37

- 240 of 372

mentor - 26 Jul 2016 23:59 - 241 of 372

By Harriet Mann | Tue, 26th July 2016 - 13:44

For a sector partially demolished by Brexit uncertainty, analysts remain confident a turn in the current cycle will not be anything like as severe as the aftermath of 2008. Downgrades this time reflect just a "modest" 10% fall in volumes and prices.

Given price targets were too optimistic ahead of the EU referendum, one analyst has decided now is a convenient time to bring sky-high expectations more in line with reality, although they still expect 40% upside and blockbuster dividend yields sector-wide.

Despite claiming a downturn would be "moderate", Deutsche Bank has slashed its 2017 cash profit estimates by 50% and pre-tax profit guidance by 60%. This risk to profit should weaken from 2018, as the sector benefits from cost-cutting and cheaper land, although pre-tax profit is still expected to fall 40% and 30% in 2018 and 2019.

"Whether this proves to be a correct assumption or not only time will tell - but it enables us to explore valuation in such a downside scenario and participate in the debate," explains analyst Glynis Johnson.

Deutsche Bank still reckons dividends can be maintained, confident the sector yields an attractive 5.2%. Even with reduced forecasts, Taylor Wimpey (TW.) leads the way with a 9% yield thanks to its special dividend commitment.

"However, for many of those with dividend policies based on P&L pay-out ratios, our forecasts suggest significantly excess cash accumulation, which could provide scope for significant higher returns to shareholders, with Barratt (BDEV) proving a strong example, with net cash in FY 2018 equivalent to a 16% yield," adds Johnson.

Identified as a driver of economic growth, government policy has prioritised housebuilding since 2007, with plans to build one million new homes from 2015-2020 reiterated post- referendum.

This commitment provides serious upside to the sector after decades of chronic undersupply. There's a chance the Help to Buy equity loan scheme could also be increased to 30%, too, which Johnson reckons will provide meaningful support to volumes.

Value opportunitiesThere is still opportunity to capture value in the sector, however. Collapsing after the referendum 'Leave' result, the housebuilders now trade on a price/net asset value (NAV) ratio of 1.4 times, although there is significant range within the sector - from 1-2.1 times. After downgrades, return on equity is expected to trough at 15% in 2017, indicating a 50% premium to cost of capital.

"We believe this suggests there remains significant value in the sector, particularly for those trading in the lower ranges of the peer group. Our pick in this category is Bovis (BVS)," says Johnson.

The analyst has her eye on the three big housebuilders she thinks offer good scope for return.

Barratt Developments

Reducing their target price by 13%, Johnson's team now reckon Barratt is worth 575p, which offers 40% upside to its current 410p price. It's yielding 7%, too.

Bovis Homes

Suffering a double-digit target price downgrade, Bovis could still be worth 55% more at 1,190p and there's a 5% yield for 2016.

Taylor Wimpey

Now worth 147p, Taylor Wimpey has 48% potential upside with its new 218p target price and offers with a 7.4% prospective yield, which grows to a sector-leading 9.1% in 2017 and 10% in 2018.

http://www.iii.co.uk/articles/341463/three-bargains-bricks-and-mortar

Nar1

- 27 Jul 2016 13:55

- 242 of 372

skinny

- 27 Jul 2016 14:02

- 243 of 372

Peel Hunt Hold 153.95 215.00 215.00 Reiterates

mentor - 27 Jul 2016 22:33 - 244 of 372

Taylor Wimpey housebuilder profits increase good trading post Brexit earnings More than a month has passed since the UK decided to leave the European Union and, despite the rhetoric of uncertainty, lots of us are still buying Taylor Wimpey (TW.) homes. The group is more profitable than this time last year, its new £450 million dividend scheme is safe, and the share price continues to make a comeback, too.

Despite macro uncertainty, demand for homes and the government's Help to Buy scheme have underpinned the housing market since the referendum. There was a brief blip in the average cancellation rate immediately following the Brexit vote, although this is back in line with low levels, and the wider London market remains robust, says Taylor Wimpey.

"One month on from the EU referendum, current trading remains in line with normal seasonal patterns. Customer interest continues to be high, with a good level of visitors," said chief executive Pete Redfern.

"Whilst it is still too early to assess what the longer-term impact from the referendum result on the housing market may be, we are encouraged by the first month's trading and by continued competitive lending from the mortgage providers as well as the positive commentary from government and policymakers."

.jpg)

Taylor Wimpey built over 6,000 new homes in the six months to 3 July and its order book has swollen to over £2.2 billion, with 90% of its properties for 2016 already sold. Its homes sold for an average £238,000, 5.8% higher than this time last year, driving a 9.1% increase in revenue to £1.5 billion and 12% increase in pre-tax profit to £266.6 million. Earnings per share (EPS) rose 14% to 6.6p.

Taking the total payout to around 10.91p per share this year (£356 million), investors will get a 0.53p interim dividend in October. And, crucially, the company said it remained "fully committed" to the dividend policy announced in May.

Shareholders are promised an enhanced ordinary dividend in 2017, representing 5% of group net assets and at least £150 million each year through the cycle. They'll also get a special dividend of £300 million, or about 9.2p a share, next July.

Tangible net asset value per (TNAV) share rose 7.8% to 88.5p in the half-year to 3 July and net cash jumped by a third to £116.7 million. Return on net operating assets has increased by 2 percentage points to 25.2%.

.jpg)

Taylor Wimpey stuck within a solid trading channel for the 12 months before June's referendum, after which the housebuilder collapsed to a two-year low of 109p. Leaping 5% to 153p Wednesday, the shares have now recovered by 40% and are firmly above the significant 38% Fibonacci retracement level from its pre-referendum high.

In a research note yesterday, Deutsche bank analyst Glynis Johnson slashed price targets across the sector. However, she still thinks Taylor Wimpey will be worth 218p target price and offers a 7.4% prospective yield.

mentor - 29 Jul 2016 09:58 - 245 of 372

UK mortgage approvals slip in June

UK mortgage approvals slipped to their lowest level since May in 2015, with just 64,766 approved in June,

from 66,722 in May. The market had expected 65,650 approvals.

Meantime, M4 Money supply climbed to 8% on a 3-month annualised basis.

cynic

- 29 Jul 2016 10:25

- 246 of 372

FOXT's lousy figures and comment show a deeper malaise i fear

nevertheless, the country still needs an awful lot more housing and TW (in particular) offers a really good yield

grannyboy

- 01 Aug 2016 11:33

- 247 of 372

mentor - 08 Aug 2016 23:21 - 248 of 372

Shares in Taylor Wimpey (LSE:TW) crashed by more than 40% on the day after the Brexit vote, and while the shares have regained some of their losses over the past month, it still looks as if the company is undervalued compared to both its peers and the wider market.

Indeed, Taylor's shares currently trade at a forward P/E of 8.9. According to current City estimates the company's earnings per share are set to grow by 14% this year, indicating that the shares trade at a PEG ratio of 0.6. A PEG ratio of less than one implies that the shares offer growth at a reasonable price. Further, the wider FTSE 100 currently trades at a P/E ratio of 38.67 so compared to the UK's leading index, shares in Taylor look exceptionally cheap.

An attractive long-term investment

Even after Brexit Taylor remains an extremely attractive investment. The UK is facing a structural housing shortage and this deficit won't disappear following the country's decision to leave the EU.

The country needs hundreds of thousands of new houses every year, and Taylor is one of the few large homebuilders that can be relied on to contribute significantly to this growth. The Bank of England's decision to ease credit conditions further last week, lowering interest rates and increasing the volume of funds available for lending by banks, should only increase the demand for new homes.

In a trading statement published on 27 July, Taylor's management announced that one month after the EU referendum, trading conditions remained in line with normal seasonal patterns. In other words, it seems as if Taylor's sales are unlikely to be impacted by Brexit in the near term. For the first half of 2016 pre-tax profit increased 12.1%.

So overall, shares in Taylor look undervalued at current levels, and the company's trading performance is still going strong.

mentor - 11 Aug 2016 09:50 - 249 of 372

The UK housing market paused for breath after the Brexit vote, but could take off again over the next 12 months, a poll of surveyors suggests.

The Royal Institution of Chartered Surveyors (Rics) survey showed house price rises slowed significantly in the three months to the end of July.

The surveyors said new buyer enquiries, home sales and new instructions all fell over the period.

The number reporting price increases dropped to its lowest in three years.

They outnumbered those seeing price falls by 5%, compared to 15% in June.

And the survey found prices had fallen outright in London, East Anglia, the North of England and the West Midlands.

'Rebound'

However, the Rics survey suggests that house price inflation could resume its upward path within a year.

A month ago - in the wake of the EU vote - surveyors were evenly divided about whether prices would rise or fall over the next 12 months.

Now a clear majority of them - 23% - expect prices to go up.

However, any such growth is likely to be modest compared to 2015, or the start of 2016, when prices were rising by up to 10% a year.

"It is not altogether surprising that near term activity measures remain relatively flat," said Rics chief economist Simon Rubinsohn.

"However, the rebound in the key twelve month indicators in the July survey suggests that confidence remains more resilient than might have been anticipated."

Inflation

Most surveyors responded to the questionnaire before the news came through last week that the Bank of England was cutting base rates by 0.25%.

Cheaper mortgages - if they happen on a significant scale - are likely to boost house prices.

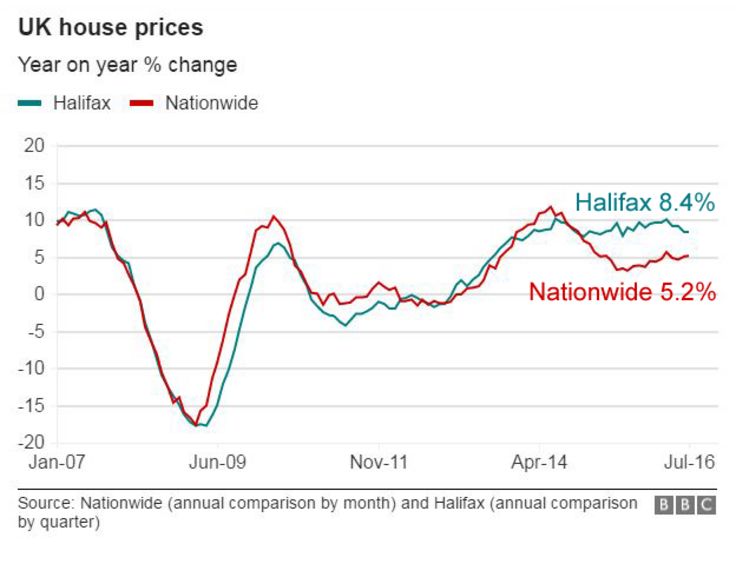

The Halifax said last week that it was still too early to say how the Brexit vote would affect values.

However, its figures show that prices fell during the month of July by 1%.

Conversely, the Nationwide Building Society said prices rose by 0.5% during the month.

Annual house price inflation is running at 8.4% according to the Halifax, and 5.2% according to the Nationwide.

cynic

- 11 Aug 2016 10:13

- 250 of 372

sooner or later this will be broken, and my guess would be to the north as houses are still desperately needed - as mentioned by many sources

HARRYCAT

- 11 Aug 2016 10:18

- 251 of 372

CC

- 11 Aug 2016 12:29

- 252 of 372

Chris Carson

- 11 Aug 2016 12:36

- 253 of 372

mentor - 15 Aug 2016 13:21 - 254 of 372

The average asking price for a house in the UK slipped 1.2% on month in August, property tracking

website Rightmove said on Monday - coming in at GBP304,222. That follows the 0.9% decline in July.

On a yearly basis, house prices advanced 4.1%, slowing from 4.5% in the previous month.

"Many prospective buyers take a summer break from home-hunting, and those who come to market at

this quieter time of year tend to price more aggressively," Rightmove Director Miles Shipside said.

mentor - 22 Aug 2016 23:15 - 255 of 372

Shares of UK-focused housebuilders such as Persimmon (LSE:PSN), Taylor Wimpey (LSE:TW) and Bovis Homes Group (LSE:BVS) continue their recovery today after falling earlier in the year.

Is this a bounce you should hop aboard or is more caution warranted?

Declining earnings

I'm cautious on the housebuilders and won't be rushing to buy their shares.

Looking back to the aftermath of the financial crisis, the housebuilders have travelled a long way in terms of rebuilding and growing their profits and in the way their share prices recovered from the depths that saw them trade with penny share status.

However, the halcyon days of double-digit growth in earnings year after year appear to be over -- at least for this wider economic cycle. City analysts following these three firms predict declines in earnings per share for 2017, Persimmon's to fall by 9%, Taylor Wimpey's by 6%, and Bovis Homes' by 6%.

The big advances as earnings recovered look done and forward growth seems set to become much harder for the housebuilders to achieve. Perhaps we're already seeing peak earnings for the sector in this wider macroeconomic cycle, despite a favourable interest rate environment and an ongoing need for further housing in Britain.

Downside risk

Affordability will likely act as a brake on demand at some point. House prices won't go up forever and people can't buy houses if they can't afford them, even if they need somewhere to live. Perhaps the ramifications of the process of Britain leaving the European Union will upset the balance of variables that has hitherto kept property prices rising. If it does, and property prices start to ease in a significant way, I can't see such a situation doing the housebuilding firms' profits and share prices any good whatsoever.

I think it's dangerous to flirt with out-and-out cyclical businesses after a long period of robust profits. When profits and share prices are elevated, as now, the risk to the downside for investors is at its most acute and the upside potential at its most limited. The stock market as a whole isn't as stupid as we might sometimes think. The market figured out cyclicality long ago and tries to mark down the valuations of cyclical firms as their profits rise in anticipation of the next cyclical down-leg.

Such valuation-compression will likely drag on investor total returns from here, so is it really worth flirting with the unknown location of the next cyclical plunge that could take away years of dividend gains in capital losses? I don't think so, especially when there are so many other less cyclical investment opportunities available on the London stock market paying more reliable dividends than the housebuilding companies right now.

The time to invest in uber-cyclical housebuilding firms is when their profits have vanished and their share prices are under the floorboards, such as in the immediate aftermath of the financial crisis. Right now, their businesses look far too healthy, so I'm avoiding them.

CC

- 24 Aug 2016 15:02

- 256 of 372

I think the dividend yield supports the price regardless of the economic and political dynamics.

hlyeo98 - 26 Oct 2016 10:32 - 257 of 372

jimmy b

- 26 Oct 2016 10:41

- 258 of 372

Claret Dragon

- 26 Oct 2016 10:57

- 259 of 372

jimmy b

- 26 Oct 2016 11:06

- 260 of 372

(Property prices are totally out of kilter with economic reality),

however we are short of housing , the problem could be that it's becoming too expensive and at some point sales will slow.

cynic

- 26 Oct 2016 11:17

- 261 of 372

my contacts in kent tell me houses at the lower end - ie say £230/250k - are being snapped up and elsewhere, properties at £1m+ are also getting interest

obviously location is everything (a true truism!) but a weak £ will also excite overseas investors

Claret Dragon

- 26 Oct 2016 11:52

- 262 of 372

cynic

- 26 Oct 2016 12:30

- 263 of 372

jimmy b

- 10 Nov 2016 17:23

- 264 of 372

optomistic

- 11 Nov 2016 08:50

- 265 of 372

jimmy b

- 11 Nov 2016 08:53

- 266 of 372

mentor - 11 Nov 2016 11:08 - 267 of 372

The 'capacity fund' is designed to tackle planning issues that can hold up projects. "We want to turbo-charge house building on large sites to get the homes built in the places people want to live, so that this country works for everyone, not just the privileged few," Housing Minister Gavin Barwell said.

optomistic

- 11 Nov 2016 12:01

- 268 of 372

jimmy b

- 14 Nov 2016 08:02

- 269 of 372

StockMarketWire.com

Taylor Wimpey said H2 trading into the autumn selling season has been strong, with good levels of customer confidence and demand underpinned by a wide range of mortgage products.

"While there remains some uncertainty following the UK's vote to leave the European Union, we are encouraged to see that the housing market has remained robust and trading has remained resilient," said CEO Pete Redfern.

"We have a strong order book position for 2016 and going into 2017, and we will maintain our focus on delivering our medium term targets.

"Looking ahead, we continue to implement our disciplined strategy which ensures that we are well placed to perform well through all market conditions and deliver enhanced value through the cycle."

OUTLOOK

Whilst the implications following the EU Referendum are still unclear, the UK housing market has remained resilient, with long term fundamentals underpinned by strong demand, the company said.

"Looking ahead, we remain confident that our business model and strategy focused on managing the business through the cycle positions us to perform well through all market conditions.

"We continue to focus on delivering our enhanced medium term financial and quality objectives, embedding our customer service processes and driving improvement in operational discipline.

"We expect to deliver an improvement in operating profit margin in 2016 (FY 2015: 20.3%), as previously guided, and a return on net operating assets** of around 30%. We remain committed to the announced £450 million total dividend payment to shareholders in 2017."

HARRYCAT

- 14 Nov 2016 08:02

- 270 of 372

niggle

- 14 Nov 2016 08:58

- 271 of 372

skinny

- 14 Nov 2016 09:01

- 272 of 372

mentor - 18 Nov 2016 12:48 - 273 of 372

Nov 18 (Reuters) - UK housebuilders, particularly those operating in central London, are finding lenders are giving out less finance for new projects since Britain's vote to leave the European Union, according to a report by property consultant Knight Frank.

Heightened caution among lenders is causing many to scrutinise deals for longer and reduce the amount of their lending by 5-10 percent of the project cost, Peter Macallan, head of structured development finance at property consultant Knight Frank told Reuters.

"So what that means is that effectively developers are having to put more cash equity into the deals upfront, giving lenders a bit more comfort in an uncertain market with Brexit, the U.S. election and what demand for UK housing stock is going to look like in 3-5 years," Macallan said.

The Residential Development Finance Report 2016/17 by Knight Frank, which surveyed the industry's 50 major operators, said over a quarter of respondents expected the loan-to-value on development projects to fall.

The result could be that builders offer bigger discounts to cash buyers to lure landlords and overseas buyers that might have limited purchases due to Brexit uncertainty and an increase in tax on buy-to-let and second homes.