| Home | Log In | Register | Our Services | My Account | Contact | Help |

East Regeneration - Telford Homes (TEF)

hangon - 24 Apr 2008 18:05

The current sp 1.50 is more-or-less the price prior to the Olympic Bid, which probably gave the sp a boost, withouit looking to far to the cost involved.

It's been all downhill for the last 12-months - Oooo deary.

The yield isn't good, despite the fall.

Greyhound - 17 Feb 2016 08:46 - 137 of 260

jimmy b

- 17 Feb 2016 14:51

- 138 of 260

- 17 Feb 2016 14:51

- 138 of 260

--------------

TELFORD HOMES PLC

(the "Company")

Director/PDMR Shareholding

The Company announces that it has been informed today that James Furlong, Land Director, has today purchased 20,000 ordinary shares of 10 pence in the Company ("Ordinary Shares") at the price of 332.5 pence per share. Following this purchase, James Furlong is beneficially interested in 1,334,342 Ordinary Shares representing approximately 1.79% of the current issued share capital and total voting rights of the Company.

jimmy b

- 08 Mar 2016 09:16

- 139 of 260

mentor - 04 Apr 2016 22:34 - 140 of 260

Will London’s Sky-High Real Estate Prices Send Telford Homes Plc Soaring?

By Motley Fool | Mon, 4th April 2016 - 08:40

Shares in London home builder Telford Homes (LSE:TEF) have risen 337% over the past five years on the back of the buoyant (some would say overheating) capital property market. Yet the shares look cheap at 9 times forward earnings with a whopping 3.9% yielding dividend on offer. Have City analysts missed a stellar small cap, or is there disaster on the way for Telford?

Focusing on non-prime London locations where prices are more reasonable, and thus more sustainable in the long term, has been a solid play for Telford. Through organic growth and acquisitions the company has built up a £1.5bn development pipeline with forward sales of £700m. Charging up to 20% of the price of a home in deposits and other fees means that the company has freed up significant cash flow years before developments are even completed.

A laser focus on costs has also brought gross margins up to 27.6%, above internal long-term goals and ahead of larger competitors. However, there are some clouds on the horizon. Net debt at the last reporting period was £50.4m, representing a gearing ratio of 37.3%. This is significantly more debt than larger homebuilders have piled on, having learned the lesson during the lean years that high leverage and low demand is a bad combination.

If London housing prices go south, gearing of 37% would be a scary sight for management and shareholders alike. I may be overly cautious, but high debt levels and relying on housing prices continuing to defy gravity makes me wary of Telford's ability to continue performing as well as it has. While the company has built up a strong portfolio and relatively lean operations, housing prices will come down eventually and Telford is far too tied to them to make me consider investing in the homebuilder at this point in the cycle.

An old post back end of January 2016

TEF gets a mention in this LSE article

Some thoughts on Builders

There seems to be general agreement that there is currently a shortfall of about 1 million homes in the UK. With some estimates being quite a bit higher. Whilst politicians like to talk a lot about the situation it seems very unlikely that it is going to be solved any time soon. The two solutions being a massive change in the supply side, essentially only achieved by a move to virtually unregulated building, or some form of nationalised building plan. Or a change in the demand side caused most likely by an economic disaster removing the need for housing as people either do not/ cannot afford to move out of their parents home, or of such a nature that mass emigration occurs freeing up the current housing stock.

Given neither of the two options are very likely it seems that housebuilders are likely to be in a reasonably strong market for the next 3 - 5 years and probably beyond.

Now this has been in part reflected in the share price rises that builders have undergone over the last three years, but this does not mean that there is not more to be gained if you pick the right builder.

The reality is that prices usually move incrementally from where they are. By this I mean that if a share is priced at X today it is likely to move + or - from X tomorrow. Few people wake up and fundamentally reappraise a price each day. We have seen this with oil prices in the last year. Realistically nothing that is moving the oil price at $30 was not known at $80. But it has taken months to get where it is not because new news has occurred, but because human nature and the fact that we largely start from yesterdays number means that it had to trail though $60, $50, $40 to get to $30.

Using info from Sharepad I have created the following chart, which covers most of my favourite metrics. Particularly those I use when looking at an asset backed business.

Before making any investment I get the accounts of the company and check the information / ratios myself, but I am happy to use the information prepared by Shared or indeed other sources as it helps me screen for the companies I want to look deeper at. I work for a living so have not devoted time to analysing each company separately. Instead when I do a table like this I look for companies which might have significant additional value. And this can be found by looking for those companies whose ratios do not fit into the generality of their peers.

At this point it is only wise to put a huge note of caution. Most usually when a company has significantly different ratios from its peers it does so because it’s in a highly anomalous situation. Its either the best and everyone knows it, so it is expensive or its a dog and best avoided. Different and good are not one and the same.

Going through each individually;

Barratt; To my mind its pretty middle of the pack. On the presumption that housebuilding as a sector still has legs it should go with the sector. But there is little to commend it relative to its peers.

Bellway; To my mind Bellway is interesting. Its PE*PEG is only 5.9 and the lower this ratio the better. Its ROCE is over 20 and that is a nice (20) number to beat. Price to NTAV is sensible to its peers and the Yield* Dividend Cover is better than most. (For this ratio higher is better). Full disclosure one of my children has picked Bellway for their portfolio.

Berkley; This looks interesting. EPV is more than 10% over Mkt Cap. PE*PEG is only 3.4. ROCE is 31.8. The niggles are the price to NTAV is relatively high. I don’t buy buy much over 3 on this metric. Though a number of my long term buy and holds have grown to be above this. Yield*Div Cover is also a smudge low relative to its peers. That said I intend to do further work on Berkeley as it does look interesting.

Bovis; Given what else is available in the list it does not look particularly special. Probably better value elsewhere.

Crest Nicholson; Again its not a bad company, just not that exciting on a relative comparison to what else is available.

Galliford Try; Relatively speaking GFRD looks distinctly uninspiring. A poor PE*PEG comparative. A poor ROCE comparative and expensive on Price to NTAV. Which is one reason why you should not rely on a basic comparator but do further work on anything you may actually put your money into. I have been an on / off investor in GFRD over the last 15 years and it has historically proven to be a good investment. It is as much an engineering business as a builder and the management team are well regarded by their engineering clients. So not an investment for me today, in the terms of this exercise. But not a company I would condemn anyone for investing in.

Inland; For the purposes of this comparison its clear to see that Inland hits the jackpot. I have therefore done some further work which is covered below.

McCarthy; From the chart above McCarthy is not one to look at further. However I would point out that McCarthy has only recently come to market. IPO in November 2015 if I recall correctly. It has been in public hands before and I was a very happy investor before it was taken private. It sells into the sheltered housing market and its actual results over the next year or so can be expected to significantly change its comparative results. But without them to review not one for today.

Persimmon; Persimmon is a little bit strange. Its EPV is less than its Market cap. Its Price to NTAV is too high, but it has a great Yield*Dividend Cover. A few years ago Persimmon made a commitment to radically reforming its capital structure and to pay out its excess capital as dividends to shareholders. This it has been doing and I have been a shareholder throughout. The comparison above is why I will not be adding to my PSN position but the strong dividend is why I will not be currently selling.

Taylor Wimpey; Like PSN Taylor Wimpey has an EPV lower than Market Cap. None of its other ratios are very exciting. Though the interest cover suggests that there is some possible capital restructuring options that could be taken by management. Not a company I would avoid, but not one I feel the need to look further at.

Telford; There are a lot of people who like Telford Homes a lot. They are very London focussed and if London property continues to boom they should do well. That said I am personally not that excited by the ratios.

Some further thoughts on Inland.

Inland Homes was set up by Stephen Wicks. He had previously set up and run Country & Metropolitan plc which listed in 1999 at a Market Cap of circa £7million and was sold in 2005 for £72 million.

He then set up Inland Homes with a core team from Country & Metropolitan. They were however not intended to be a builder. When initially listed the thesis was very much that the real earnings of C&M had come from getting planning permission for land and not from building. Inland was therefore not going to be a builder but a land developer. Once planning consent had been won on a site it would then be sold to a builder for the development.

IMHO this met with only limited success. It turned out that the larger builders did not need Inland as much as Inland needed the larger builders. They had their own teams to find and consent land and their need for additional sites was set either by internal replenishment targets or for a number of years severally curtailed by the financial crisis.

This encouraged - forced Inland to extend its range of operations and to begin building in its own right.

Inland remains a minnow in this arena. As a consequence there is a real risk that revenue will be volatile. The larger players are bringing on hundreds of developments, Inland has a couple of dozen and a couple of key revenue generators within that. One major problem on a key site and the numbers will be impacted,

The company is small so there is a limited base of professional investors. (Only Henderson Global Investors has a holding over 3%). This means that there is limited trading in the shares and they can be very volatile on limited news. The spread can also widen and close as the broker sees fit, rather than to reflect any underlying factor.

That said business is currently going well and Inland has proven themselves capable of finding, consenting, developing and selling sites.

Compared to its peers Inland is lowly rated against the real results that it is delivering. The problem for Inland is getting the attention of the larger investors who could help it become rated more closely to its peers. Its market cap is currently just too small for many funds and there is no specific catalyst that would cause it to rerate any time soon. However given the delivery is currently real and management have in the past delivered shareholder value there does seem to be a limited downside with decent upside potential. I also note that management have significant positions in the business and they are not getting any younger so have an interest in delivering a catalyst event. I also do believe that over time the rating should close in part as Inland continues to validate the building and sales side of the operation.

I have therefore initiated a position in Inland with a DCF valuation £215m - £255m. With a possible break to the upside.

http://www.lsesharetalk.com/investmentreports/some-thoughts-on-builders.php

cynic

- 05 Apr 2016 09:02

- 141 of 260

i have a holding in my sipp and intend to hang on to it

jimmy b

- 05 Apr 2016 09:35

- 142 of 260

mentor - 05 Apr 2016 10:39 - 143 of 260

More lies from you know who

mentor - 07 Apr 2016 23:00 - 144 of 260

London calling - By Motley Fool | Thu, 7th April 2016 - 09:20

The big housebuilders are often in the news, but we don't hear so much about Telford Homes (LSE:TEF), which specialises in non-prime locations in London. Fears of overheating of prices in the capital have led to a 32% share price fall since last May's peak, to 333p, but we're still looking at a quadrupling over the past five years.

But what interests me here is the company's strongly rising dividend, which has been growing well ahead of inflation -- and there are further inflation-busting increases forecast for this year and the next two. In terms of yield, we'd be seeing 4.1% for this year, rising to 4.8% by March 2018, with cover by earnings comfortably in excess of 2.5 times.

The risk is that if the feared London slowdown should happen, Telford's relatively high debt, of £50.4m at 30 September, could start to hurt. But with a significant portion of its forward sales already secured by deposits, the dividend income might still be safe. I'm cautious on this one.

mentor - 11 Apr 2016 12:25 - 145 of 260

MARKET REPORT

FTSE dips as house builders fall, miners rise

London equities were sideways with a slight negative bias to midday, falling house builders providing blue-chip ballast.

Berkeley (BDEV) shed 2.67% to 3040.p, and was followed by Taylor Wimpey (TW.), lower 1.85% to 182.75p. Also down were Persimmon (PSN) and Barratt Developments (BDEV). Commercial property was guided by Hammerson (HMSO), off 0.47% to 587.25p, but was off the overall pace.

jimmy b

- 11 Apr 2016 12:29

- 146 of 260

jimmy b

- 13 Apr 2016 08:09

- 147 of 260

TEF sees FY pretax profit slightly ahead of views

StockMarketWire.com

Telford Homes anticipates its FY 2016 pretax profit will be slightly ahead of current market expectations.

"The Group was already over 90 per cent forward sold at the start of the financial year but has improved on original forecasts due primarily to initial profit recognition on the PRS sale announced in February 2016," the company said.

HIGHLIGHTS:

� Market remains strong for typical Telford Homes product from UK investors, overseas investors and owner-occupiers

� Successful launch of The Liberty Building, E14 selling 68 of the 105 open market apartments in the last four weeks with a combined sales value of over �40 million

� More than 50% of the cumulative revenue expected in the next three financial years up to 31 March 2019 has already been secured through forward sales

� First Private Rented Sector ("PRS") development contracted with L&Q for �66.75 million

� Terms agreed on a second PRS transaction with significant potential for more over the next few years

� Development pipeline as at 31 March 2016 of over �1.5 billion of future revenue

� Many opportunities continue to be appraised and negotiated to further strengthen the development pipeline, utilising the �50 million placing funds raised in October 2015

� Longer term growth expectations have increased during the year with profit before tax now forecast to exceed �50 million in the year to 31 March 2019.

jimmy b

- 13 Apr 2016 17:16

- 148 of 260

jimmy b

- 22 Apr 2016 14:10

- 149 of 260

mentor - 29 Apr 2016 14:23 - 150 of 260

“The month-on-month fall in the average house price is not a surprise as the market is gearing up for a change.”

The TELEGRAPH - Anna White, head of property - 28 APRIL 2016 • 12:09PM

House prices fall almost everywhere as property market takes on 'uncomfortable' feel

For sale signs

New data from the Land Registry shows house prices falling in March across the majority of regions

House prices in all the regions in England and Wales apart from London and the East fell in March, according to new data from the Land Registry.

Considered by industry experts to be the most accurate of all the house price indices, fresh figures showed that property values edged down across the country, even in the high-demand South East.

Where prices have fallen

Overall house prices in England and Wales fell 0.5pc in March, taking the average paid price to £189,901. The biggest drop was in Yorkshire and Humberside (-2.6pc).

Values dipped 2pc in the West Midlands and 1.2pc in the North East.

The potent cocktail of a growing population and a lack of stock continued to push London prices up in the mainstream market, negating the 10pc price falls at the luxury end of the sector. House prices in the capital inched up 0.2pc to £534,785. Homeowners in the East of the country saw the same rise in February.

"Why I am troubled"

While monthly fluctuations, especially in a dreary March, are to be expected, these numbers could also come as a precursor to a period of significant uncertainty in the housing market.

"I have worked through three property recessions and this has an uncomfortable yet familiar feel. I think the market is on the turn," said independent buyer and industry commentator Henry Pryor . ............

house-prices-fall-almost-everywhere-as-property-market-takes-on

cynic

- 29 Apr 2016 14:49

- 151 of 260

however, i think TEF is positioned correctly ...... and ditto BVS and to a lesser extent TW. ..... not sure about BDEV as it's not one i follow

mentor - 04 May 2016 16:23 - 152 of 260

mentor - 13 May 2016 09:27 - 153 of 260

Is the share price tells you something or is the negative news about buyers? .....

New buyers deserted housing market in April, says Rics

BBC - By Brian Milligan - Personal Finance reporter - 12 May 2016

The number of people interested in buying a house in April fell to its lowest level for nearly eight years, according to surveyors across the UK.

Those who saw a drop in enquiries last month outnumbered those who saw a rise by 22%.

That is the highest figure reported by the Royal Institution of Chartered Surveyors (Rics) since August 2008.

Rics said the main reason was the stamp duty rise on 1 April, and the uncertainty around the EU referendum.

The number of new enquiries fell most dramatically in London, but also fell in nine other regions of the UK.

Enquiries rose only in East Anglia, the North and Scotland.

Most surveyors also reported a fall in new instructions to sell, and most expect prices to rise over the next three months.

Rics chief economist Simon Rubinsohn said the market was characterised by uncertainty.

"More ominous is the expectation that both prices and rents will head materially higher over the medium term," he said.

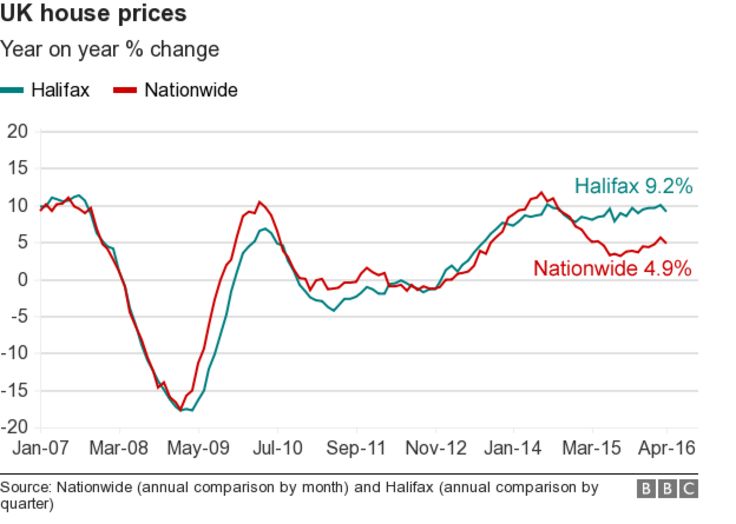

Earlier this week the Halifax reported that annual house price inflation fell from 10.1% in March to 9.2% in April.

mentor - 17 May 2016 16:26 - 154 of 260

jimmy b

- 17 May 2016 16:28

- 155 of 260

mentor - 17 May 2016 16:44 - 156 of 260

How long can house prices keep rising?

TELEGRAPH - Isabelle Fraser - 17 MAY 2016 • 10:33AM

House prices jumped in March, fuelled by a buy-to-let surge that sparked huge increases in London and the south east – but experts have warned this might be the last rise for some time.

The UK’s average house price grew by 9pc in March, from 7.6pc in February - the highest rate since the same month last year. Prices fell dramatically in Scotland, by 6.1pc compared to the same month last year, according to figures from the Office for National Statistics.

Average house prices in seven of the nine English regions are at record levels, with the price in London up 2.2pc on its previous record in January.

This growth means house prices have risen more than five times faster than wages in the last five years, according to analysis by the Resolution Foundation.

The problem is even more acute in London, where house prices have risen by 57pc in five years, but average weekly earning have actually fallen slightly during the same period.

The ONS said that high levels of house price growth in March were most likely due to investors bringing forward purchases before stamp duty on buy-to-let properties was hiked by 3pc. HMRC said that housing transactions surged by 70pc in March from a year ago.

“This is likely to be the last big rise for a while as more realism enters the market, although a shortage of listings and low transaction levels may underpin house price increases in future," said Jeremy Leaf, a former Royal Institution of Chartered Surveyors chairman and north London estate agent.

House prices are still increasing annually at a rate that sits well above any rise in average earnings, making our housing market even less affordable as each month goes by Jeremy Duncombe, Legal & General’s Mortgage Club

“Lack of supply continues to be a huge concern, and while the ONS takes some comfort from recent UK construction output figures which showed that house building was the bright spot for the industry in the first quarter, this is potentially a last hurrah as confidence is likely to dip in response to weakening activity."

Rics last week reported a fall in the number of new buyer inquiries in April, to the lowest level since 2008. Home hunters were put off by uncertainty surrounding the referendum on EU membership and affordability concerns, according to Rics.

Mr Leaf added: “People are nervous: there are short-term concerns about the market but longer-term fears about the strength of the economy. Brexit is a bit of a smokescreen - the strength of the economy is a bigger issue.

“While in the suburbs and outside the centre of London the housing industry is still confident, in the centre of London where there is oversupply and a lot of cranes, they are not.”

The top quarter of London's housing market saw an annual fall of 2.4pc, according to estate agency Stirling Ackroyd, but it said that a slowdown was a "myth" for the majority of London.

The buy-to-let industry by numbersPlay! 01:13

Andrew Bridges, managing director, said the London property market was "undergoing a serious readjustment".

Richard Snook, economist at PwC, said: "There are no signs of any Brexit-related slowdown in this month’s figures, although the underlying trends are masked by the effects of the stamp duty change.”

The Council for Mortgage Lenders revealed that house purchase lending was up 60pc in March compared to the same month last year. This was due largely to the rush to beat the stamp duty increase, but there was a boom in home movers securing mortgages as well.

Jeremy Duncombe, the director of Legal & General’s Mortgage Club, said: “Given that these figures cover the period leading up to the buy-to-let stamp duty rise, it’s no surprise that they show another strong monthly increase in house prices.

“However, even without this surge in buy-to-let activity, house prices are still increasing annually at a rate that sits well above any rise in average earnings, making our housing market even less affordable as each month goes by."

House prices hit record highs - but could this be a 'last hurrah'?

| About MoneyAM | Ts and Cs | Privacy Policy | Investment Warning | Content Standards | Corporate Solutions | Advertise With Us | Site Map | © 2026 MoneyAM |