| Home | Log In | Register | Our Services | My Account | Contact | Help |

You are NOT currently logged in

AIM listed telecoms/tech company - astounding growth (GBO)

Greyhound - 14 Apr 2011 21:53

chessplayer - 29 Sep 2014 07:32 - 160 of 250

GLOBO plc

INTERIM RESULTS FOR THE SIX MONTHS ENDED 30 JUNE 2014

Globo PLC (LSE-AIM: GBO), the international provider of enterprise mobility management solutions and software as a service, is pleased to announce its unaudited interim results for the six months ended 30 June 2014.

Financial highlights

• Revenue up 45% to €46.5 million (H1 2013: €32.0 million)

o GO!Enterprise revenue up 95% to €19.9 million (H1 2013: €10.2 million)

o CitronGO! and GO!Social revenue up 12% to €20.1 million (H1 2013: €17.9 million1)

• EBITDA increased 23% to €22.0 million (H1 2013: €17.9 million)

• Profit before tax up 11% to €16.1 million (H1 2013: €14.5 million)

• Earnings per share increased 5% to €0.043 (H1 2013: €0.041)

• Free Cash Flow2 of €4.2 million (H1 2013: €(3.7) million)

o Last Twelve Months Free Cash Flow €13.1 million

• EBITDA Cash Conversion Ratio3 of 83% (H1 2013: 15%)

• Net cash position of €46.0 million as at 30 June 2014 (H1 2013: €10.8 million)

Operating highlights

• Significant growth in licence and end user base:

o GO!Enterprise Enterprise Mobility Management ("EMM") business-to-employee device licences up 67% to 569,500 at the half year (31 December 2013: 340,600)

o GO!Enterprise Mobile Application Development Platform ("MADP") business-to-consumer licences up 90% to 24.9 million (31 December 2013: 13.1 million)

o CitronGO! and GO!Social monthly active users up 13% to 3.4 million (31 December 2013: 3.0 million)

• Additional enterprise customer wins, including new GO!Enterprise EMM licence customers such as Siemens, TUI, TNT, PeopleCert and Intracom Telecom.

• Integrated contract win for licences, application development, consulting and services with new customer, the New South Wales Health Administration, in Australia

• Acquisition of mobile applications developer Sourcebits Inc., for a cash consideration of US$12 million brings integrated MADP capability and access to new customers

• Significant expansion of US operations following acquisition of Notify Technology Inc.; CEO relocation to the US to focus on US operations and growth opportunity

• Launch of new products and services: GO!AppZoneStudio and GO!Enterprise WorkSpace

Post period end highlights

• €7.5 million integrated product project win with new customer, the Greek Ministry of Public Order and Citizen Protection

• Additional project work with existing Sourcebits customers Intel, McKinsey, SAP, EMC and ING

• Globo included in Ovum's Decision Matrix report 2014-15, with recognition as a market challenger amongst the top 11 EMM vendors globally

Trading outlook

• Trend of growth in enterprise customer and new project wins during H1 expected to continue

• Strong business momentum expected due to traditionally stronger second half and continued US expansion

Commenting on the results, Costis Papadimitrakopoulos, CEO of Globo, said:

"Globo's growing reputation in the enterprise mobile markets around the world is translating into strong growth in revenue and profits. Demand for our market-leading products and services is being supported by positive industry trends, particularly the growth of Bring Your Own Device. Globo continues to invest in developing new products to strengthen our offering and I am confident that Globo is well positioned to continue the positive growth story reflected in these results."

INTERIM RESULTS FOR THE SIX MONTHS ENDED 30 JUNE 2014

Globo PLC (LSE-AIM: GBO), the international provider of enterprise mobility management solutions and software as a service, is pleased to announce its unaudited interim results for the six months ended 30 June 2014.

Financial highlights

• Revenue up 45% to €46.5 million (H1 2013: €32.0 million)

o GO!Enterprise revenue up 95% to €19.9 million (H1 2013: €10.2 million)

o CitronGO! and GO!Social revenue up 12% to €20.1 million (H1 2013: €17.9 million1)

• EBITDA increased 23% to €22.0 million (H1 2013: €17.9 million)

• Profit before tax up 11% to €16.1 million (H1 2013: €14.5 million)

• Earnings per share increased 5% to €0.043 (H1 2013: €0.041)

• Free Cash Flow2 of €4.2 million (H1 2013: €(3.7) million)

o Last Twelve Months Free Cash Flow €13.1 million

• EBITDA Cash Conversion Ratio3 of 83% (H1 2013: 15%)

• Net cash position of €46.0 million as at 30 June 2014 (H1 2013: €10.8 million)

Operating highlights

• Significant growth in licence and end user base:

o GO!Enterprise Enterprise Mobility Management ("EMM") business-to-employee device licences up 67% to 569,500 at the half year (31 December 2013: 340,600)

o GO!Enterprise Mobile Application Development Platform ("MADP") business-to-consumer licences up 90% to 24.9 million (31 December 2013: 13.1 million)

o CitronGO! and GO!Social monthly active users up 13% to 3.4 million (31 December 2013: 3.0 million)

• Additional enterprise customer wins, including new GO!Enterprise EMM licence customers such as Siemens, TUI, TNT, PeopleCert and Intracom Telecom.

• Integrated contract win for licences, application development, consulting and services with new customer, the New South Wales Health Administration, in Australia

• Acquisition of mobile applications developer Sourcebits Inc., for a cash consideration of US$12 million brings integrated MADP capability and access to new customers

• Significant expansion of US operations following acquisition of Notify Technology Inc.; CEO relocation to the US to focus on US operations and growth opportunity

• Launch of new products and services: GO!AppZoneStudio and GO!Enterprise WorkSpace

Post period end highlights

• €7.5 million integrated product project win with new customer, the Greek Ministry of Public Order and Citizen Protection

• Additional project work with existing Sourcebits customers Intel, McKinsey, SAP, EMC and ING

• Globo included in Ovum's Decision Matrix report 2014-15, with recognition as a market challenger amongst the top 11 EMM vendors globally

Trading outlook

• Trend of growth in enterprise customer and new project wins during H1 expected to continue

• Strong business momentum expected due to traditionally stronger second half and continued US expansion

Commenting on the results, Costis Papadimitrakopoulos, CEO of Globo, said:

"Globo's growing reputation in the enterprise mobile markets around the world is translating into strong growth in revenue and profits. Demand for our market-leading products and services is being supported by positive industry trends, particularly the growth of Bring Your Own Device. Globo continues to invest in developing new products to strengthen our offering and I am confident that Globo is well positioned to continue the positive growth story reflected in these results."

Greyhound - 29 Sep 2014 08:19 - 161 of 250

Good results. Broker updates today, RBC tp 120p and Canaccord 90p

chessplayer - 29 Sep 2014 15:45 - 162 of 250

A very poor do when such good results lead to a fall of 1.75 points!

chessplayer - 06 Oct 2014 09:57 - 163 of 250

Currently trading on a PE of just over 6 and a sector average of 20 we ought to be in for quite a price riose on this little beauty.

chessplayer - 21 Oct 2014 09:55 - 164 of 250

21 October 2014

Globo receives United States NIST Data Security Certification

Globo meets highest industry standard for application security, supporting its growth into highly regulated markets such as government, finance and healthcare.

Globo Plc (LSE-AIM: GBO), the international provider of enterprise mobility management (EMM) solutions and software as a service (SaaS), is pleased to announce that the United States National Institute of Standards and Technology (NIST) Cryptographic Module Validation Program (CMVP) has validated Globo's cryptographic modules as per Federal Information Processing Standards (FIPS) 140-2 Security Standard for Cryptographic Modules. FIPS 140-2 validated encryption has been added to the entire Globo solution suite, which consists of GO!Enterprise EMM and GO!AppZone MADP (Mobile Application Development Platform) offerings, which means that Globo's offering now satisfies the highest level of security required in the United States.

This certification gives Globo a competitive advantage in addressing commercial opportunities in highly-regulated markets such as government, finance and healthcare, which demand the highest level of validated encryption. Within Globo's EMM and MADP ecosystem thiscertificationapplies equally to functions such as email, messaging, file access or browsing, and connection to back-end systems or databases. FIPS validation represents an important milestone for Globo'sstrategy for expansion on the United States.

Further, Globo is the only vendor cited in Gartner's 2014 Magic Quadrant for Enterprise Mobility Managementthat has received US NIST FIPS 140-2 validation for each major operating environment; iOS, Android, Windows Phone and Windows Server. Globo is also unique in being the first MADP software vendor able to offer the ability to develop mobile applications that are suitable for these regulated markets and which require FIPS 140-2 Validated Cryptography.

Costis Papadimitrakopoulos, CEO of Globo, said:

"Globo has made a significant investment in providing customers with validated FIPS 140-2 encryption for both our enterprise mobility management and mobile app development solutions. This level of encryption allows companies to meet IT compliance requirements for the Payment Card Industry (PCI), Sarbanes-Oxley Act reporting, HIPAA compliance (Health Insurance Portability and AccountingAct), Financial Industry Regulatory Authority (FINRA) compliance and other highly-regulated markets."

The Globo FIPS 140-2 validated encryption modules will be available for use with the following operating systems:

• Apple iOS

• Google Android

• Windows Phone 7 and 8

• Windows Server 2013

Globo's offering with the encryption modules will be commercially available by the end of Q4 2014. Globo's certificates, 2268 and 2269, can be reviewed at:

http://csrc.nist.gov/groups/STM/cmvp/documents/140-1/1401val2014.htm#2268

Globo receives United States NIST Data Security Certification

Globo meets highest industry standard for application security, supporting its growth into highly regulated markets such as government, finance and healthcare.

Globo Plc (LSE-AIM: GBO), the international provider of enterprise mobility management (EMM) solutions and software as a service (SaaS), is pleased to announce that the United States National Institute of Standards and Technology (NIST) Cryptographic Module Validation Program (CMVP) has validated Globo's cryptographic modules as per Federal Information Processing Standards (FIPS) 140-2 Security Standard for Cryptographic Modules. FIPS 140-2 validated encryption has been added to the entire Globo solution suite, which consists of GO!Enterprise EMM and GO!AppZone MADP (Mobile Application Development Platform) offerings, which means that Globo's offering now satisfies the highest level of security required in the United States.

This certification gives Globo a competitive advantage in addressing commercial opportunities in highly-regulated markets such as government, finance and healthcare, which demand the highest level of validated encryption. Within Globo's EMM and MADP ecosystem thiscertificationapplies equally to functions such as email, messaging, file access or browsing, and connection to back-end systems or databases. FIPS validation represents an important milestone for Globo'sstrategy for expansion on the United States.

Further, Globo is the only vendor cited in Gartner's 2014 Magic Quadrant for Enterprise Mobility Managementthat has received US NIST FIPS 140-2 validation for each major operating environment; iOS, Android, Windows Phone and Windows Server. Globo is also unique in being the first MADP software vendor able to offer the ability to develop mobile applications that are suitable for these regulated markets and which require FIPS 140-2 Validated Cryptography.

Costis Papadimitrakopoulos, CEO of Globo, said:

"Globo has made a significant investment in providing customers with validated FIPS 140-2 encryption for both our enterprise mobility management and mobile app development solutions. This level of encryption allows companies to meet IT compliance requirements for the Payment Card Industry (PCI), Sarbanes-Oxley Act reporting, HIPAA compliance (Health Insurance Portability and AccountingAct), Financial Industry Regulatory Authority (FINRA) compliance and other highly-regulated markets."

The Globo FIPS 140-2 validated encryption modules will be available for use with the following operating systems:

• Apple iOS

• Google Android

• Windows Phone 7 and 8

• Windows Server 2013

Globo's offering with the encryption modules will be commercially available by the end of Q4 2014. Globo's certificates, 2268 and 2269, can be reviewed at:

http://csrc.nist.gov/groups/STM/cmvp/documents/140-1/1401val2014.htm#2268

mentor - 27 Oct 2014 10:09 - 165 of 250

Currently at 43.63p

Motley Fool today

3 Growth Companies I’d Buy Now: Globo PLC, Plus500 Ltd And Quindell PLC

With stock markets tumbling around the world, now is the time to bag a bargain. In particular, there are a wide range of growth companies which are as cheap as chips. So here are my three small-cap picks.

Globo

Globo (LSE: GBO) is a technology company that provides mobile apps and services to business. This is a fast-growing area, and the company has seen an impressive increase in its earnings, as the eps progression below shows:

2011: 3.26p, 2012: 4.22p, 2013: 6.2p, 2014: 8p, 2015: 10p

When a company grows as quickly as this, there can be a lot of volatility, but choose your moment well and you can bag a growth company at a value price.

I think this is one such moment: the 2014 P/E ratio is 5.6, falling to 4.5 in 2015.

Considering how quickly this company’s profits are growing, that is astonishingly cheap.

ps As I have previously stated, all the shorts have done is massively detach the co's share price from it's fundamentals.

A sensible 2015 p/e for a fast growing techcompany would be say 15, which implies a share price of around 150p, 13 months out.

If the share price continues to be depressed,I can't see Globo remaining independent.

Motley Fool today

3 Growth Companies I’d Buy Now: Globo PLC, Plus500 Ltd And Quindell PLC

With stock markets tumbling around the world, now is the time to bag a bargain. In particular, there are a wide range of growth companies which are as cheap as chips. So here are my three small-cap picks.

Globo

Globo (LSE: GBO) is a technology company that provides mobile apps and services to business. This is a fast-growing area, and the company has seen an impressive increase in its earnings, as the eps progression below shows:

2011: 3.26p, 2012: 4.22p, 2013: 6.2p, 2014: 8p, 2015: 10p

When a company grows as quickly as this, there can be a lot of volatility, but choose your moment well and you can bag a growth company at a value price.

I think this is one such moment: the 2014 P/E ratio is 5.6, falling to 4.5 in 2015.

Considering how quickly this company’s profits are growing, that is astonishingly cheap.

ps As I have previously stated, all the shorts have done is massively detach the co's share price from it's fundamentals.

A sensible 2015 p/e for a fast growing techcompany would be say 15, which implies a share price of around 150p, 13 months out.

If the share price continues to be depressed,I can't see Globo remaining independent.

mentor - 31 Oct 2014 16:23 - 166 of 250

Chart is looking promising with RSI and Stochastic around 50, but someone is controling the share price movement ( the shorting buggers)

mentor - 10 Nov 2014 12:25 - 167 of 250

Last Friday low of 40.50p, could be the double bottom, before the the next move up ahead of update. Shorters are managing to hold the price low and reducing their stakes at the same time.

About time FCA acts on the market abuse by those shorters

WERE others trades go on ISDX

http://www.isdx.com/forcompanies/ourcompanies/companydetail/default.aspx?securityid=100727

About time FCA acts on the market abuse by those shorters

WERE others trades go on ISDX

http://www.isdx.com/forcompanies/ourcompanies/companydetail/default.aspx?securityid=100727

chessplayer - 20 Nov 2014 10:25 - 168 of 250

Revenues at Globo - the international provider of enterprise mobility management solutions and software-as-a-service - rose by 46% to 73.2m in the nine months to the end of September.

GO!Enterprise revenues grew by 89% to 35.0m, including a maiden contribution from Sourcebits of 1.2m while CitronGO! revenues increased by 13% to 29.8m.

Gross profit margin improved to 62% (H1 2014: 58%) reflecting the positive impact of direct salescompared to indirect channels.

Chief executive Costis Papadimitrakopoulos said: "We are happy to report that, seventeen years after the Group's foundation, our business continues to innovate and grow on all fronts.

"After my move to California, the company has established a more US-driven development path. Our reputation and position in the market continues to go from strength to strength and I expect this to be reflected in the future performance of the Group. We are confident that the successes of the first nine months of the year will continue through the remainder of 2014 and beyond."

GO!Enterprise revenues grew by 89% to 35.0m, including a maiden contribution from Sourcebits of 1.2m while CitronGO! revenues increased by 13% to 29.8m.

Gross profit margin improved to 62% (H1 2014: 58%) reflecting the positive impact of direct salescompared to indirect channels.

Chief executive Costis Papadimitrakopoulos said: "We are happy to report that, seventeen years after the Group's foundation, our business continues to innovate and grow on all fronts.

"After my move to California, the company has established a more US-driven development path. Our reputation and position in the market continues to go from strength to strength and I expect this to be reflected in the future performance of the Group. We are confident that the successes of the first nine months of the year will continue through the remainder of 2014 and beyond."

mentor - 20 Nov 2014 11:27 - 169 of 250

Figures just to good for the share price to stay on those low prices

Trading Update for nine months ended 30 September 2014

Globo Plc (LSE-AIM: GBO),

· Revenues for the first 9 months of the year grew by 46% to €73.2 million (first 9 months 2013: €50.0 million):

# GO!Enterprise revenues grew by 89% to €35.0 million (first 9 months 2013: €18.5 million), including a maiden contribution from Sourcebits of €1.2 million;

# CitronGO! Revenues grew by 13% to €29.8 (first 9 months 2013: €26.4 million).

# The Group continued to generate free cash flow1 during the third quarter. The net cash position

at 30 September 2014 was €36.3 million (30 June 2014: €46.0m) after payment of US$12.0 million and associated costs for the acquisition of Sourcebits in July 2014, and other investment and setup costs associated with US expansion.

# We expect positive free cash flow generation to continue during the last quarter of 2014 and we remain confident that our year-end results will meet market expectations.

http://stockcharts.com/h-sc/ui?s=GBO.L

Trading Update for nine months ended 30 September 2014

Globo Plc (LSE-AIM: GBO),

· Revenues for the first 9 months of the year grew by 46% to €73.2 million (first 9 months 2013: €50.0 million):

# GO!Enterprise revenues grew by 89% to €35.0 million (first 9 months 2013: €18.5 million), including a maiden contribution from Sourcebits of €1.2 million;

# CitronGO! Revenues grew by 13% to €29.8 (first 9 months 2013: €26.4 million).

# The Group continued to generate free cash flow1 during the third quarter. The net cash position

at 30 September 2014 was €36.3 million (30 June 2014: €46.0m) after payment of US$12.0 million and associated costs for the acquisition of Sourcebits in July 2014, and other investment and setup costs associated with US expansion.

# We expect positive free cash flow generation to continue during the last quarter of 2014 and we remain confident that our year-end results will meet market expectations.

http://stockcharts.com/h-sc/ui?s=GBO.L

chessplayer - 21 Nov 2014 09:36 - 170 of 250

down a touch after recent gains, but continued buying suggests more gains to come.

mentor - 09 Apr 2015 13:45 - 171 of 250

Bought some stock at 45p

Has been moving lower for some time and again today, but at this price 45p offer plenty of trades go on every time it comes to this price. Well undervalued on a historic PE of 7.2 and the latest update is everything OK for results at the end of the month, small spread

other trades at ISDX .......... GBO trades at ISDX

Has been moving lower for some time and again today, but at this price 45p offer plenty of trades go on every time it comes to this price. Well undervalued on a historic PE of 7.2 and the latest update is everything OK for results at the end of the month, small spread

other trades at ISDX .......... GBO trades at ISDX

mentor - 09 Apr 2015 14:12 - 172 of 250

CHART

&IND=&Layout=2Line;Default;Price;HisDate&XCycle=&XFormat=)

mentor - 09 Apr 2015 16:23 - 173 of 250

for the last 30 minutes the order book got stronger and a few large trades are taking the price higher from the 45p offer lasting most of the afternoon

spread 45p v 45.25p

56K at bid price 6K at offer

DEPH at 18 trades both sides

spread 45p v 45.25p

56K at bid price 6K at offer

DEPH at 18 trades both sides

mentor - 10 Apr 2015 09:30 - 174 of 250

the turning point of this cycle could have been the 45p support yesterday

spread 46 v 47 now on a complete change of order book, yesterday the DEPTH was about 4 trades down on the bid side

today is about 9 up

spread 46 v 47 now on a complete change of order book, yesterday the DEPTH was about 4 trades down on the bid side

today is about 9 up

mentor - 10 Apr 2015 09:41 - 175 of 250

Future bid prospects

Any company trading at a 75% discount to it's peers, in a rapidly consolidating market, does not stay independent for long

-------------------------

From the 2013 consolidated accounts, intangibles including goodwill were €33m. Total shareholders’ funds were €138m so even deducting the intangibles shareholders’ funds would be €105m. That compares with a market value of about €250m, i.e. net tangible assets are about 20p per share.

Within those net assets we have net cash of €43m, gross cash of €64m and a further €20 of undrawn facilities. Since Globo generated significant free cash flow from operations (about €12m) for 2014, they really don’t need anything like that amount of cash – if anything the balance sheet is too strong to the point that it is inefficient.

Of course the cash also gives them the resources to make acquisitions although to date the acquisitions they have made have been of relatively modest “infill” nature.

the amount capitalised to-date must account for most of €48.8m (= €39.8m + 9.0m) of intangible assets + goodwill (as of HY 2014). For a company on the high end of EMM technology hoping to maintain and improve on its position among the global leaders in the sector, it is essential to spend money on R&D.

One can but compared the annual spending and amounts and spending by its competitors. Then the €49m might look modest!

Any company trading at a 75% discount to it's peers, in a rapidly consolidating market, does not stay independent for long

-------------------------

From the 2013 consolidated accounts, intangibles including goodwill were €33m. Total shareholders’ funds were €138m so even deducting the intangibles shareholders’ funds would be €105m. That compares with a market value of about €250m, i.e. net tangible assets are about 20p per share.

Within those net assets we have net cash of €43m, gross cash of €64m and a further €20 of undrawn facilities. Since Globo generated significant free cash flow from operations (about €12m) for 2014, they really don’t need anything like that amount of cash – if anything the balance sheet is too strong to the point that it is inefficient.

Of course the cash also gives them the resources to make acquisitions although to date the acquisitions they have made have been of relatively modest “infill” nature.

the amount capitalised to-date must account for most of €48.8m (= €39.8m + 9.0m) of intangible assets + goodwill (as of HY 2014). For a company on the high end of EMM technology hoping to maintain and improve on its position among the global leaders in the sector, it is essential to spend money on R&D.

One can but compared the annual spending and amounts and spending by its competitors. Then the €49m might look modest!

mentor - 10 Apr 2015 11:11 - 176 of 250

BINGO

steady as she goes 48.38p +3.25p +7.20%

there was a large trade earlier 60K paying almost 49p at ISDX.............

10/04/2015 11:01 GBX/ISDX-exn 60,000 48.89p

steady as she goes 48.38p +3.25p +7.20%

there was a large trade earlier 60K paying almost 49p at ISDX.............

10/04/2015 11:01 GBX/ISDX-exn 60,000 48.89p

mentor - 10 Apr 2015 12:48 - 177 of 250

ISDX - is having a good volume and is 30 minutes delayed... 251,368K

LSE - Cum Vol ---- 324,467

LSE - Cum Vol ---- 324,467

mentor - 12 Apr 2015 23:10 - 178 of 250

RESUME of various places.............

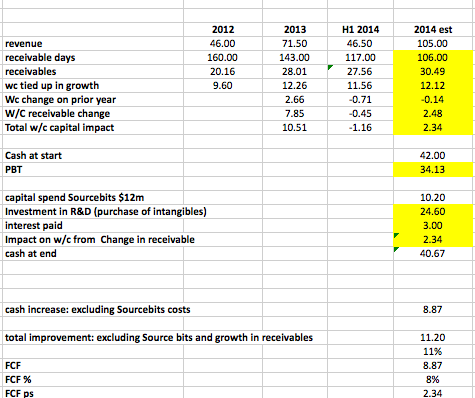

The conclusion is that GBO is investing heavily in growth. All items that diminish its cash are growth driven expenditure. ie source bits, invest in R&D and w/c impact of receivables. (the recivables are down from 160 days in 2012 to 110-117 in 2014 but notwistanding it costs cash to fund the w/c to grow.

A net Free cash flow of 10.38m (10% or revenue) is not shoddy

Strip Source bits and w/c tie up the cash would be improved to 15.13m (14%)

Now lets get real:

Globo FCF per share : 5.97% of current sp

ARM is 1.2% of current SP

RR. is 0.96% of current sp.

Admiral is 2.8%

Diagio 3.2%

------------------

Last year's increase in working capitalresulted in cash outflow of 13.5m, this year's forecast is 11.9m. EBITDA forecast is 46.8m. The Sourcebits acquisition was $12m (USD) which is 9.6m euros but there was 0.6m in H1 (deferred consideration in respect of Notify) so total acquisition costs will be 10.2m euros. Forecasting capitalised R&D of 24.6m, interest payments of 3.1m. At year end net cash was 40.3m (vs 42.7m in 2013) so free cash flow for the year will be 7.8m euros (40.3 - 42.7 +10.2 = 7.8).

EBITDA figure of 34m looks low, we're forecasting an operating profit of 35m so adding back depreciation and amortisation costs (non cash costs reported in the P+L) of 11.8m takes us to 46.8m EBITDA.

The conclusion is that GBO is investing heavily in growth. All items that diminish its cash are growth driven expenditure. ie source bits, invest in R&D and w/c impact of receivables. (the recivables are down from 160 days in 2012 to 110-117 in 2014 but notwistanding it costs cash to fund the w/c to grow.

A net Free cash flow of 10.38m (10% or revenue) is not shoddy

Strip Source bits and w/c tie up the cash would be improved to 15.13m (14%)

Now lets get real:

Globo FCF per share : 5.97% of current sp

ARM is 1.2% of current SP

RR. is 0.96% of current sp.

Admiral is 2.8%

Diagio 3.2%

------------------

Last year's increase in working capitalresulted in cash outflow of 13.5m, this year's forecast is 11.9m. EBITDA forecast is 46.8m. The Sourcebits acquisition was $12m (USD) which is 9.6m euros but there was 0.6m in H1 (deferred consideration in respect of Notify) so total acquisition costs will be 10.2m euros. Forecasting capitalised R&D of 24.6m, interest payments of 3.1m. At year end net cash was 40.3m (vs 42.7m in 2013) so free cash flow for the year will be 7.8m euros (40.3 - 42.7 +10.2 = 7.8).

EBITDA figure of 34m looks low, we're forecasting an operating profit of 35m so adding back depreciation and amortisation costs (non cash costs reported in the P+L) of 11.8m takes us to 46.8m EBITDA.

mentor - 14 Apr 2015 10:15 - 179 of 250

another steady rise, though not large it is better this way ahead of news of when the results are going to be announce, expectations going from previous years is before the end of this month

spread 47 v 48

a very strong order book 21 v 10

and bid/offer price 78K v 35K

not much volume on the LSE and not better on the ISDX

spread 47 v 48

a very strong order book 21 v 10

and bid/offer price 78K v 35K

not much volume on the LSE and not better on the ISDX

| About MoneyAM | Ts and Cs | Privacy Policy | Investment Warning | Content Standards | Corporate Solutions | Advertise With Us | Site Map | © 2026 MoneyAM |

Register now for FREE

Share Prices,

Stock Quotes,

Charts, Bulletin Boards, Indices, Watchlists, Portfolio, Market News, Research

or see our Premium Services including Level 2, Terminal and much more.