| Home | Log In | Register | Our Services | My Account | Contact | Help |

You are NOT currently logged in

AIM listed telecoms/tech company - astounding growth (GBO)

Greyhound - 14 Apr 2011 21:53

mentor - 10 Apr 2015 12:48 - 177 of 250

ISDX - is having a good volume and is 30 minutes delayed... 251,368K

LSE - Cum Vol ---- 324,467

LSE - Cum Vol ---- 324,467

mentor - 12 Apr 2015 23:10 - 178 of 250

RESUME of various places.............

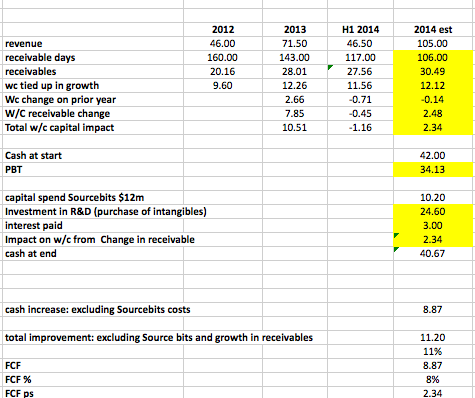

The conclusion is that GBO is investing heavily in growth. All items that diminish its cash are growth driven expenditure. ie source bits, invest in R&D and w/c impact of receivables. (the recivables are down from 160 days in 2012 to 110-117 in 2014 but notwistanding it costs cash to fund the w/c to grow.

A net Free cash flow of 10.38m (10% or revenue) is not shoddy

Strip Source bits and w/c tie up the cash would be improved to 15.13m (14%)

Now lets get real:

Globo FCF per share : 5.97% of current sp

ARM is 1.2% of current SP

RR. is 0.96% of current sp.

Admiral is 2.8%

Diagio 3.2%

------------------

Last year's increase in working capitalresulted in cash outflow of 13.5m, this year's forecast is 11.9m. EBITDA forecast is 46.8m. The Sourcebits acquisition was $12m (USD) which is 9.6m euros but there was 0.6m in H1 (deferred consideration in respect of Notify) so total acquisition costs will be 10.2m euros. Forecasting capitalised R&D of 24.6m, interest payments of 3.1m. At year end net cash was 40.3m (vs 42.7m in 2013) so free cash flow for the year will be 7.8m euros (40.3 - 42.7 +10.2 = 7.8).

EBITDA figure of 34m looks low, we're forecasting an operating profit of 35m so adding back depreciation and amortisation costs (non cash costs reported in the P+L) of 11.8m takes us to 46.8m EBITDA.

The conclusion is that GBO is investing heavily in growth. All items that diminish its cash are growth driven expenditure. ie source bits, invest in R&D and w/c impact of receivables. (the recivables are down from 160 days in 2012 to 110-117 in 2014 but notwistanding it costs cash to fund the w/c to grow.

A net Free cash flow of 10.38m (10% or revenue) is not shoddy

Strip Source bits and w/c tie up the cash would be improved to 15.13m (14%)

Now lets get real:

Globo FCF per share : 5.97% of current sp

ARM is 1.2% of current SP

RR. is 0.96% of current sp.

Admiral is 2.8%

Diagio 3.2%

------------------

Last year's increase in working capitalresulted in cash outflow of 13.5m, this year's forecast is 11.9m. EBITDA forecast is 46.8m. The Sourcebits acquisition was $12m (USD) which is 9.6m euros but there was 0.6m in H1 (deferred consideration in respect of Notify) so total acquisition costs will be 10.2m euros. Forecasting capitalised R&D of 24.6m, interest payments of 3.1m. At year end net cash was 40.3m (vs 42.7m in 2013) so free cash flow for the year will be 7.8m euros (40.3 - 42.7 +10.2 = 7.8).

EBITDA figure of 34m looks low, we're forecasting an operating profit of 35m so adding back depreciation and amortisation costs (non cash costs reported in the P+L) of 11.8m takes us to 46.8m EBITDA.

mentor - 14 Apr 2015 10:15 - 179 of 250

another steady rise, though not large it is better this way ahead of news of when the results are going to be announce, expectations going from previous years is before the end of this month

spread 47 v 48

a very strong order book 21 v 10

and bid/offer price 78K v 35K

not much volume on the LSE and not better on the ISDX

spread 47 v 48

a very strong order book 21 v 10

and bid/offer price 78K v 35K

not much volume on the LSE and not better on the ISDX

Greyhound - 16 Apr 2015 12:06 - 180 of 250

A long time treading water but I still think we will move materially higher at some point. When is the question! Canaccord buy rating maintained this month, tp 90p. RBC 120p from February.

mentor - 17 Apr 2015 16:02 - 181 of 250

Looking better this afternoon, though very volatile and the higher bid that someone is placing is being taken soon by "AT"

volume is rising also, soon should be news of when results are announce

spread 47 v 47.75p, was a bit earlier at 47.75 v 48.25p

Level2 / order book DEPTH is strong at 23 v 13

volume is rising also, soon should be news of when results are announce

spread 47 v 47.75p, was a bit earlier at 47.75 v 48.25p

Level2 / order book DEPTH is strong at 23 v 13

Greyhound - 17 Apr 2015 16:14 - 182 of 250

Let's hope the results will be the catalyst.

Greyhound - 17 Apr 2015 16:16 - 183 of 250

Results were 30th April last year.

mentor - 23 Apr 2015 11:53 - 184 of 250

finally the company has announce the date of results ............

Notice of 2014 Final Results

Globo plc (LSE-AIM: GBO), the international provider of Enterprise Mobility Management, mobile solutions and software as a service, will announce its preliminary results for the year ended 31 December 2014, on Thursday 30 April 2015.

A presentation to analysts and private client brokers will be held at 10.30 on that day at the MWB Business Exchange, 55 Old Broad Street, London, EC2M 1RX.

&MA(50)&IND=MACD(26,12,9);RSI(14);SlowSTO(14,3,3)&Layout=2Line;Default;Price;HisDate&XCycle=&XFormat=)

Notice of 2014 Final Results

Globo plc (LSE-AIM: GBO), the international provider of Enterprise Mobility Management, mobile solutions and software as a service, will announce its preliminary results for the year ended 31 December 2014, on Thursday 30 April 2015.

A presentation to analysts and private client brokers will be held at 10.30 on that day at the MWB Business Exchange, 55 Old Broad Street, London, EC2M 1RX.

Greyhound - 24 Apr 2015 09:24 - 185 of 250

Not long to wait perhaps we'll start to see a move northwards

required field - 24 Apr 2015 09:25 - 186 of 250

Isn't this based in Greece ?....

VICTIM - 24 Apr 2015 09:36 - 187 of 250

I think now it has a small percentage only in Greece now , it sold most Greek business.

mentor - 28 Apr 2015 10:40 - 188 of 250

spread 47.50 v 48p

Since yesterday there is some sense of fresh air on the trading front, and though the closing price yesterday was still @ 47p one could see plenty of trades well above that.

today has started where late yesterday finished and the fruit of it is showing on the share price and also on the trades and much the same on the order book, very strong on the bid side

Since yesterday there is some sense of fresh air on the trading front, and though the closing price yesterday was still @ 47p one could see plenty of trades well above that.

today has started where late yesterday finished and the fruit of it is showing on the share price and also on the trades and much the same on the order book, very strong on the bid side

Greyhound - 28 Apr 2015 11:11 - 189 of 250

I would hope to see us edging 50p before the results on Thursday...

mentor - 28 Apr 2015 12:00 - 190 of 250

Well looking good for the Thursday's results as it reaches highs not seeing for some time

the order book continues strong and glad the sell order at 48.50p was not large and now over.

order book DEPTH 29 v 21

the order book continues strong and glad the sell order at 48.50p was not large and now over.

order book DEPTH 29 v 21

Greyhound - 28 Apr 2015 14:52 - 191 of 250

So perhaps today then!

mentor - 28 Apr 2015 22:54 - 192 of 250

GBO results due on Thursday

Forecasts

Year Ending - Profit(£m)- EPS - P/E - PEG - EPS Grth.

31-Dec-14 ------ 23.20 - 6.21p - 7.7 - 0.4 - +17%

31-Dec-15 ------ 28.08 - 7.51p - 6.4 - 0.3 - +21%

31-Dec-16 ------ 33.69 - 9.02p - 5.3 - 0.3 - +20%

Revenue (£m)

31-Dec-2015 97

31-Dec-2016 112

--------------------------

Last month ST covered GBO, 2014 eps expectation in line with Arthurlys:-

This news can only underpin prospects for this year and expectations that Globo will deliver on analysts’ pre-tax profit estimates of €50.7m on revenues of €122m, up from €34.3m and €99.8m forecast for calendar 2014. On this basis, EPS are predicted to increase by 11 per cent to 8.2 cents (5.8p) in 2014, rising to 11.9 cents (8.5p) this year.

This means that even after factoring in the near 10 per cent appreciation of sterling against the euro since the start of 2015, Globo’s shares are still only priced on 10 times likely fiscal 2014 earnings, falling to 7 times 2015 estimates assuming of course it delivers the robust growth anticipated by sector analysts.

Forecasts

Year Ending - Profit(£m)- EPS - P/E - PEG - EPS Grth.

31-Dec-14 ------ 23.20 - 6.21p - 7.7 - 0.4 - +17%

31-Dec-15 ------ 28.08 - 7.51p - 6.4 - 0.3 - +21%

31-Dec-16 ------ 33.69 - 9.02p - 5.3 - 0.3 - +20%

Revenue (£m)

31-Dec-2015 97

31-Dec-2016 112

--------------------------

Last month ST covered GBO, 2014 eps expectation in line with Arthurlys:-

This news can only underpin prospects for this year and expectations that Globo will deliver on analysts’ pre-tax profit estimates of €50.7m on revenues of €122m, up from €34.3m and €99.8m forecast for calendar 2014. On this basis, EPS are predicted to increase by 11 per cent to 8.2 cents (5.8p) in 2014, rising to 11.9 cents (8.5p) this year.

This means that even after factoring in the near 10 per cent appreciation of sterling against the euro since the start of 2015, Globo’s shares are still only priced on 10 times likely fiscal 2014 earnings, falling to 7 times 2015 estimates assuming of course it delivers the robust growth anticipated by sector analysts.

mentor - 29 Apr 2015 10:53 - 193 of 250

The Company

Globo is an international leader and technology innovator delivering multi-platform Enterprise Mobility Management and Telecom software solutions.

Product offerings include:

Enterprise Mobility solutions including GO!Enterprise Office, GO!Enterprise Mobilizer, GO!Enterprise Reach, GO!Enterprise247 Cloud, and GO!Enterprise Mobility in a Box. Additionally, through several combinations of the GO!Enterprise Mobility Management Platform, the most comprehensive mobile application platform, Globo empowers enterprise developers and ISVs to create secure mobile applications by utilizing the patented technology of secure containerization for both corporate-liable devices and BYOD initiatives.

Consumer Mobility solutions including CitronGO! and GO!Social offering a unique smartphone user experience on feature phones, empowering MNOs and MVASPs to maximize ARPU, user retention and network utilization and efficiency.

Globo was founded in 1997 and is run through its head offices in New York, London and Athens.

Since 2007, Globo has been listed on London Stock Exchange’s AIM market as (GBO:LN).

The Group operates internationally through subsidiaries and offices in the US, the UK, the Europe, the Middle East and the South East Asia.

Globo mobile solutions currently operate in more than 45 countries and serve more than 6 million users on a monthly basis.

Globo has partnerships with industry leaders including Samsung, Fujitsu, Ingram Micro, Computerlinks, ASBIS and leading software and systems integrators who combine to support the industry’s broadest range of mobile devices.

Globo has received numerous awards for its innovative technology and superior financial performance and is recognized as one of the key players in its field in numerous Technology reports such as Gartner, VDC, OVUM etc.

Since December 2012, Globo has divested from its Greek legacy business (e-business software) operations and is focusing solely in its international expansion which today represents more than 85% of its operations.

Globo is an international leader and technology innovator delivering multi-platform Enterprise Mobility Management and Telecom software solutions.

Product offerings include:

Enterprise Mobility solutions including GO!Enterprise Office, GO!Enterprise Mobilizer, GO!Enterprise Reach, GO!Enterprise247 Cloud, and GO!Enterprise Mobility in a Box. Additionally, through several combinations of the GO!Enterprise Mobility Management Platform, the most comprehensive mobile application platform, Globo empowers enterprise developers and ISVs to create secure mobile applications by utilizing the patented technology of secure containerization for both corporate-liable devices and BYOD initiatives.

Consumer Mobility solutions including CitronGO! and GO!Social offering a unique smartphone user experience on feature phones, empowering MNOs and MVASPs to maximize ARPU, user retention and network utilization and efficiency.

Globo was founded in 1997 and is run through its head offices in New York, London and Athens.

Since 2007, Globo has been listed on London Stock Exchange’s AIM market as (GBO:LN).

The Group operates internationally through subsidiaries and offices in the US, the UK, the Europe, the Middle East and the South East Asia.

Globo mobile solutions currently operate in more than 45 countries and serve more than 6 million users on a monthly basis.

Globo has partnerships with industry leaders including Samsung, Fujitsu, Ingram Micro, Computerlinks, ASBIS and leading software and systems integrators who combine to support the industry’s broadest range of mobile devices.

Globo has received numerous awards for its innovative technology and superior financial performance and is recognized as one of the key players in its field in numerous Technology reports such as Gartner, VDC, OVUM etc.

Since December 2012, Globo has divested from its Greek legacy business (e-business software) operations and is focusing solely in its international expansion which today represents more than 85% of its operations.

mentor - 29 Apr 2015 11:05 - 194 of 250

with regards to "upenn "

Share price has not grown with profits

Share price now 48p

Share price has not grown with profits

Share price now 48p

Greyhound - 30 Apr 2015 07:47 - 195 of 250

FY pretax up 30% to EUR 35.7m, above expectations. Strong momentum of 2014 has continued in first quarter. Perhaps today the start of a re-rating.

mentor - 30 Apr 2015 08:24 - 196 of 250

Astounding Results results with EPS of 6.70p so worth around 100p

52p +4p

GLOBO Plc ("Globo" or the "Group")

Preliminary Unaudited Results for the Full Year ended 31 December 2014

Strong revenue growth; third consecutive year of positive free cash flow1, of €7.3 million

Globo plc (LSE-AIM: GBO), the international provider of Enterprise Mobility Management (EMM), mobile solutions and software as a service (SaaS), announces preliminary unaudited results for the year ended 31 December 2014.

Financial Highlights

• Revenues up 49% to €106.4 million (2013: €71.5 million), ahead of market expectations

· GO!Enterprise revenue up 94% to €57.9 million (2013: €29.9 million)

· CitronGO! and GO!Social revenue up 11% to €38.5 million (2013: €34.8 million)

• Revenues from North America increased by 334% to €15.5 million (2013: €3.6 million) representing the 15% of the total Group revenues.

· EBITDA up 41% to €50.9 million (2013: €36.0 million), ahead of market expectations

• Profit Before Tax up 30% to €35.7 million (2013: €27.4 million), ahead of market expectations

• Earnings Per Share of €0.094 (2013: €0.074), ahead of market expectations

• Free Cash Flow1 of €7.3 million (2013: €5.2 million)

• Year-end cash position of €82.8 million (2013: €64.2 million) with Net Cash position (cash minus debt) of €40.4 million (2013: €42.8 million)

1 Free Cash Flow (FCF). Free cash flow is calculated by taking the net cash flow from operating and investing activities, adding back the cost of acquisitions.

Operating Highlights

Growth in Customer Base

• GO!Enterprise customer base grew to 834,000 business-to-employee device licenses (2013: 340,600) and 31.8 million business-to-consumer licenses (2013: 13.1 million)

• CitronGO! and GO!Social customer base increased to 3.50 million monthly active users (2013: 2.98 million)

52p +4p

GLOBO Plc ("Globo" or the "Group")

Preliminary Unaudited Results for the Full Year ended 31 December 2014

Strong revenue growth; third consecutive year of positive free cash flow1, of €7.3 million

Globo plc (LSE-AIM: GBO), the international provider of Enterprise Mobility Management (EMM), mobile solutions and software as a service (SaaS), announces preliminary unaudited results for the year ended 31 December 2014.

Financial Highlights

• Revenues up 49% to €106.4 million (2013: €71.5 million), ahead of market expectations

· GO!Enterprise revenue up 94% to €57.9 million (2013: €29.9 million)

· CitronGO! and GO!Social revenue up 11% to €38.5 million (2013: €34.8 million)

• Revenues from North America increased by 334% to €15.5 million (2013: €3.6 million) representing the 15% of the total Group revenues.

· EBITDA up 41% to €50.9 million (2013: €36.0 million), ahead of market expectations

• Profit Before Tax up 30% to €35.7 million (2013: €27.4 million), ahead of market expectations

• Earnings Per Share of €0.094 (2013: €0.074), ahead of market expectations

• Free Cash Flow1 of €7.3 million (2013: €5.2 million)

• Year-end cash position of €82.8 million (2013: €64.2 million) with Net Cash position (cash minus debt) of €40.4 million (2013: €42.8 million)

1 Free Cash Flow (FCF). Free cash flow is calculated by taking the net cash flow from operating and investing activities, adding back the cost of acquisitions.

Operating Highlights

Growth in Customer Base

• GO!Enterprise customer base grew to 834,000 business-to-employee device licenses (2013: 340,600) and 31.8 million business-to-consumer licenses (2013: 13.1 million)

• CitronGO! and GO!Social customer base increased to 3.50 million monthly active users (2013: 2.98 million)

| About MoneyAM | Ts and Cs | Privacy Policy | Investment Warning | Content Standards | Corporate Solutions | Advertise With Us | Site Map | © 2026 MoneyAM |

Register now for FREE

Share Prices,

Stock Quotes,

Charts, Bulletin Boards, Indices, Watchlists, Portfolio, Market News, Research

or see our Premium Services including Level 2, Terminal and much more.