| Home | Log In | Register | Our Services | My Account | Contact | Help |

Taylor Wimpey (TW.)

skinny

- 26 Jun 2014 12:12

- 26 Jun 2014 12:12

Link to old thread

About us

We are one of the UK's largest residential developers. As a responsible developer we are committed to working with local people and communities.

Company Website

Financial calendar

Recent Broker notes

BarChart Indicators

Recent Market news

Taylor Wimpey Fundamentals (TW.)

mentor - 12 Jul 2016 10:21 - 238 of 372

a gain of 37.20p or 32.92 % on 11 working days

cynic

- 12 Jul 2016 11:17

- 239 of 372

amazingly high volume today (already 56m+), but suspect it's just a freaky day rather than anything of note

HARRYCAT

- 13 Jul 2016 11:37

- 240 of 372

mentor - 26 Jul 2016 23:59 - 241 of 372

By Harriet Mann | Tue, 26th July 2016 - 13:44

For a sector partially demolished by Brexit uncertainty, analysts remain confident a turn in the current cycle will not be anything like as severe as the aftermath of 2008. Downgrades this time reflect just a "modest" 10% fall in volumes and prices.

Given price targets were too optimistic ahead of the EU referendum, one analyst has decided now is a convenient time to bring sky-high expectations more in line with reality, although they still expect 40% upside and blockbuster dividend yields sector-wide.

Despite claiming a downturn would be "moderate", Deutsche Bank has slashed its 2017 cash profit estimates by 50% and pre-tax profit guidance by 60%. This risk to profit should weaken from 2018, as the sector benefits from cost-cutting and cheaper land, although pre-tax profit is still expected to fall 40% and 30% in 2018 and 2019.

"Whether this proves to be a correct assumption or not only time will tell - but it enables us to explore valuation in such a downside scenario and participate in the debate," explains analyst Glynis Johnson.

Deutsche Bank still reckons dividends can be maintained, confident the sector yields an attractive 5.2%. Even with reduced forecasts, Taylor Wimpey (TW.) leads the way with a 9% yield thanks to its special dividend commitment.

"However, for many of those with dividend policies based on P&L pay-out ratios, our forecasts suggest significantly excess cash accumulation, which could provide scope for significant higher returns to shareholders, with Barratt (BDEV) proving a strong example, with net cash in FY 2018 equivalent to a 16% yield," adds Johnson.

Identified as a driver of economic growth, government policy has prioritised housebuilding since 2007, with plans to build one million new homes from 2015-2020 reiterated post- referendum.

This commitment provides serious upside to the sector after decades of chronic undersupply. There's a chance the Help to Buy equity loan scheme could also be increased to 30%, too, which Johnson reckons will provide meaningful support to volumes.

Value opportunitiesThere is still opportunity to capture value in the sector, however. Collapsing after the referendum 'Leave' result, the housebuilders now trade on a price/net asset value (NAV) ratio of 1.4 times, although there is significant range within the sector - from 1-2.1 times. After downgrades, return on equity is expected to trough at 15% in 2017, indicating a 50% premium to cost of capital.

"We believe this suggests there remains significant value in the sector, particularly for those trading in the lower ranges of the peer group. Our pick in this category is Bovis (BVS)," says Johnson.

The analyst has her eye on the three big housebuilders she thinks offer good scope for return.

Barratt Developments

Reducing their target price by 13%, Johnson's team now reckon Barratt is worth 575p, which offers 40% upside to its current 410p price. It's yielding 7%, too.

Bovis Homes

Suffering a double-digit target price downgrade, Bovis could still be worth 55% more at 1,190p and there's a 5% yield for 2016.

Taylor Wimpey

Now worth 147p, Taylor Wimpey has 48% potential upside with its new 218p target price and offers with a 7.4% prospective yield, which grows to a sector-leading 9.1% in 2017 and 10% in 2018.

http://www.iii.co.uk/articles/341463/three-bargains-bricks-and-mortar

Nar1

- 27 Jul 2016 13:55

- 242 of 372

skinny

- 27 Jul 2016 14:02

- 243 of 372

Peel Hunt Hold 153.95 215.00 215.00 Reiterates

mentor - 27 Jul 2016 22:33 - 244 of 372

Taylor Wimpey housebuilder profits increase good trading post Brexit earnings More than a month has passed since the UK decided to leave the European Union and, despite the rhetoric of uncertainty, lots of us are still buying Taylor Wimpey (TW.) homes. The group is more profitable than this time last year, its new £450 million dividend scheme is safe, and the share price continues to make a comeback, too.

Despite macro uncertainty, demand for homes and the government's Help to Buy scheme have underpinned the housing market since the referendum. There was a brief blip in the average cancellation rate immediately following the Brexit vote, although this is back in line with low levels, and the wider London market remains robust, says Taylor Wimpey.

"One month on from the EU referendum, current trading remains in line with normal seasonal patterns. Customer interest continues to be high, with a good level of visitors," said chief executive Pete Redfern.

"Whilst it is still too early to assess what the longer-term impact from the referendum result on the housing market may be, we are encouraged by the first month's trading and by continued competitive lending from the mortgage providers as well as the positive commentary from government and policymakers."

.jpg)

Taylor Wimpey built over 6,000 new homes in the six months to 3 July and its order book has swollen to over £2.2 billion, with 90% of its properties for 2016 already sold. Its homes sold for an average £238,000, 5.8% higher than this time last year, driving a 9.1% increase in revenue to £1.5 billion and 12% increase in pre-tax profit to £266.6 million. Earnings per share (EPS) rose 14% to 6.6p.

Taking the total payout to around 10.91p per share this year (£356 million), investors will get a 0.53p interim dividend in October. And, crucially, the company said it remained "fully committed" to the dividend policy announced in May.

Shareholders are promised an enhanced ordinary dividend in 2017, representing 5% of group net assets and at least £150 million each year through the cycle. They'll also get a special dividend of £300 million, or about 9.2p a share, next July.

Tangible net asset value per (TNAV) share rose 7.8% to 88.5p in the half-year to 3 July and net cash jumped by a third to £116.7 million. Return on net operating assets has increased by 2 percentage points to 25.2%.

.jpg)

Taylor Wimpey stuck within a solid trading channel for the 12 months before June's referendum, after which the housebuilder collapsed to a two-year low of 109p. Leaping 5% to 153p Wednesday, the shares have now recovered by 40% and are firmly above the significant 38% Fibonacci retracement level from its pre-referendum high.

In a research note yesterday, Deutsche bank analyst Glynis Johnson slashed price targets across the sector. However, she still thinks Taylor Wimpey will be worth 218p target price and offers a 7.4% prospective yield.

mentor - 29 Jul 2016 09:58 - 245 of 372

UK mortgage approvals slip in June

UK mortgage approvals slipped to their lowest level since May in 2015, with just 64,766 approved in June,

from 66,722 in May. The market had expected 65,650 approvals.

Meantime, M4 Money supply climbed to 8% on a 3-month annualised basis.

cynic

- 29 Jul 2016 10:25

- 246 of 372

FOXT's lousy figures and comment show a deeper malaise i fear

nevertheless, the country still needs an awful lot more housing and TW (in particular) offers a really good yield

grannyboy

- 01 Aug 2016 11:33

- 247 of 372

mentor - 08 Aug 2016 23:21 - 248 of 372

Shares in Taylor Wimpey (LSE:TW) crashed by more than 40% on the day after the Brexit vote, and while the shares have regained some of their losses over the past month, it still looks as if the company is undervalued compared to both its peers and the wider market.

Indeed, Taylor's shares currently trade at a forward P/E of 8.9. According to current City estimates the company's earnings per share are set to grow by 14% this year, indicating that the shares trade at a PEG ratio of 0.6. A PEG ratio of less than one implies that the shares offer growth at a reasonable price. Further, the wider FTSE 100 currently trades at a P/E ratio of 38.67 so compared to the UK's leading index, shares in Taylor look exceptionally cheap.

An attractive long-term investment

Even after Brexit Taylor remains an extremely attractive investment. The UK is facing a structural housing shortage and this deficit won't disappear following the country's decision to leave the EU.

The country needs hundreds of thousands of new houses every year, and Taylor is one of the few large homebuilders that can be relied on to contribute significantly to this growth. The Bank of England's decision to ease credit conditions further last week, lowering interest rates and increasing the volume of funds available for lending by banks, should only increase the demand for new homes.

In a trading statement published on 27 July, Taylor's management announced that one month after the EU referendum, trading conditions remained in line with normal seasonal patterns. In other words, it seems as if Taylor's sales are unlikely to be impacted by Brexit in the near term. For the first half of 2016 pre-tax profit increased 12.1%.

So overall, shares in Taylor look undervalued at current levels, and the company's trading performance is still going strong.

mentor - 11 Aug 2016 09:50 - 249 of 372

The UK housing market paused for breath after the Brexit vote, but could take off again over the next 12 months, a poll of surveyors suggests.

The Royal Institution of Chartered Surveyors (Rics) survey showed house price rises slowed significantly in the three months to the end of July.

The surveyors said new buyer enquiries, home sales and new instructions all fell over the period.

The number reporting price increases dropped to its lowest in three years.

They outnumbered those seeing price falls by 5%, compared to 15% in June.

And the survey found prices had fallen outright in London, East Anglia, the North of England and the West Midlands.

'Rebound'

However, the Rics survey suggests that house price inflation could resume its upward path within a year.

A month ago - in the wake of the EU vote - surveyors were evenly divided about whether prices would rise or fall over the next 12 months.

Now a clear majority of them - 23% - expect prices to go up.

However, any such growth is likely to be modest compared to 2015, or the start of 2016, when prices were rising by up to 10% a year.

"It is not altogether surprising that near term activity measures remain relatively flat," said Rics chief economist Simon Rubinsohn.

"However, the rebound in the key twelve month indicators in the July survey suggests that confidence remains more resilient than might have been anticipated."

Inflation

Most surveyors responded to the questionnaire before the news came through last week that the Bank of England was cutting base rates by 0.25%.

Cheaper mortgages - if they happen on a significant scale - are likely to boost house prices.

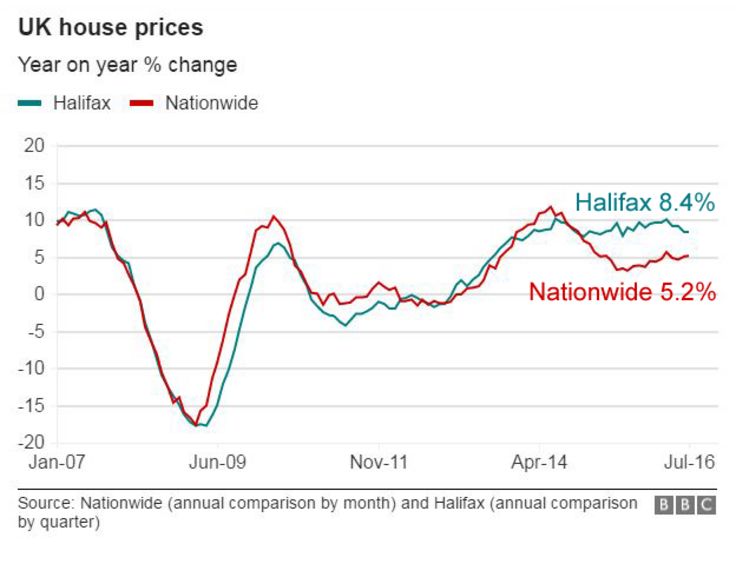

The Halifax said last week that it was still too early to say how the Brexit vote would affect values.

However, its figures show that prices fell during the month of July by 1%.

Conversely, the Nationwide Building Society said prices rose by 0.5% during the month.

Annual house price inflation is running at 8.4% according to the Halifax, and 5.2% according to the Nationwide.

cynic

- 11 Aug 2016 10:13

- 250 of 372

sooner or later this will be broken, and my guess would be to the north as houses are still desperately needed - as mentioned by many sources

HARRYCAT

- 11 Aug 2016 10:18

- 251 of 372

CC

- 11 Aug 2016 12:29

- 252 of 372

Chris Carson

- 11 Aug 2016 12:36

- 253 of 372

mentor - 15 Aug 2016 13:21 - 254 of 372

The average asking price for a house in the UK slipped 1.2% on month in August, property tracking

website Rightmove said on Monday - coming in at GBP304,222. That follows the 0.9% decline in July.

On a yearly basis, house prices advanced 4.1%, slowing from 4.5% in the previous month.

"Many prospective buyers take a summer break from home-hunting, and those who come to market at

this quieter time of year tend to price more aggressively," Rightmove Director Miles Shipside said.

mentor - 22 Aug 2016 23:15 - 255 of 372

Shares of UK-focused housebuilders such as Persimmon (LSE:PSN), Taylor Wimpey (LSE:TW) and Bovis Homes Group (LSE:BVS) continue their recovery today after falling earlier in the year.

Is this a bounce you should hop aboard or is more caution warranted?

Declining earnings

I'm cautious on the housebuilders and won't be rushing to buy their shares.

Looking back to the aftermath of the financial crisis, the housebuilders have travelled a long way in terms of rebuilding and growing their profits and in the way their share prices recovered from the depths that saw them trade with penny share status.

However, the halcyon days of double-digit growth in earnings year after year appear to be over -- at least for this wider economic cycle. City analysts following these three firms predict declines in earnings per share for 2017, Persimmon's to fall by 9%, Taylor Wimpey's by 6%, and Bovis Homes' by 6%.

The big advances as earnings recovered look done and forward growth seems set to become much harder for the housebuilders to achieve. Perhaps we're already seeing peak earnings for the sector in this wider macroeconomic cycle, despite a favourable interest rate environment and an ongoing need for further housing in Britain.

Downside risk

Affordability will likely act as a brake on demand at some point. House prices won't go up forever and people can't buy houses if they can't afford them, even if they need somewhere to live. Perhaps the ramifications of the process of Britain leaving the European Union will upset the balance of variables that has hitherto kept property prices rising. If it does, and property prices start to ease in a significant way, I can't see such a situation doing the housebuilding firms' profits and share prices any good whatsoever.

I think it's dangerous to flirt with out-and-out cyclical businesses after a long period of robust profits. When profits and share prices are elevated, as now, the risk to the downside for investors is at its most acute and the upside potential at its most limited. The stock market as a whole isn't as stupid as we might sometimes think. The market figured out cyclicality long ago and tries to mark down the valuations of cyclical firms as their profits rise in anticipation of the next cyclical down-leg.

Such valuation-compression will likely drag on investor total returns from here, so is it really worth flirting with the unknown location of the next cyclical plunge that could take away years of dividend gains in capital losses? I don't think so, especially when there are so many other less cyclical investment opportunities available on the London stock market paying more reliable dividends than the housebuilding companies right now.

The time to invest in uber-cyclical housebuilding firms is when their profits have vanished and their share prices are under the floorboards, such as in the immediate aftermath of the financial crisis. Right now, their businesses look far too healthy, so I'm avoiding them.

CC

- 24 Aug 2016 15:02

- 256 of 372

I think the dividend yield supports the price regardless of the economic and political dynamics.

hlyeo98 - 26 Oct 2016 10:32 - 257 of 372

| About MoneyAM | Ts and Cs | Privacy Policy | Investment Warning | Content Standards | Corporate Solutions | Advertise With Us | Site Map | © 2026 MoneyAM |