| Home | Log In | Register | Our Services | My Account | Contact | Help |

You are NOT currently logged in

Avanti Communications (AVN)

hlyeo98 - 04 Aug 2010 11:22

This is a BUY tip from Tom Winnifrith...

Sorry if this is rather boring as the market cap is now c 350 million but at 470p Avanti Communications (AVN) - a stock held in the SF t1ps Growth Fund - is really very cheap whichever way you look at it. It is now funded to launch 3 satellites into space ( and fully insured if the worst happens which will only delay the programme by 6 months anyway). You value Avanti by discounting back the net cashflows these satellites will generate. That depends on how much capacity is sold and at what price. Use a model based on very conservative assumptions and this stock is worth 13 ( the lowest valuation in the market). But that model uses assumptions about sales prices which are already being beaten by forward sales Avanti is booking today. Use those prices and you head up to the 22.50 value of house broker Cenkos. My own view is that Avanti will do better still and this stock could therefore be worth 25. Exc itement will mount as the first satellite is launched later this year. Remember those valuations are the Net Present Value of future cashflows ( i.e. what they are worth today). If you can buy at under 600p ( as you can now) you should do so and sit back and wait. I suspect after HYLAS 1 is launched you will never again be able to buy at less than 600p.

Sorry if this is rather boring as the market cap is now c 350 million but at 470p Avanti Communications (AVN) - a stock held in the SF t1ps Growth Fund - is really very cheap whichever way you look at it. It is now funded to launch 3 satellites into space ( and fully insured if the worst happens which will only delay the programme by 6 months anyway). You value Avanti by discounting back the net cashflows these satellites will generate. That depends on how much capacity is sold and at what price. Use a model based on very conservative assumptions and this stock is worth 13 ( the lowest valuation in the market). But that model uses assumptions about sales prices which are already being beaten by forward sales Avanti is booking today. Use those prices and you head up to the 22.50 value of house broker Cenkos. My own view is that Avanti will do better still and this stock could therefore be worth 25. Exc itement will mount as the first satellite is launched later this year. Remember those valuations are the Net Present Value of future cashflows ( i.e. what they are worth today). If you can buy at under 600p ( as you can now) you should do so and sit back and wait. I suspect after HYLAS 1 is launched you will never again be able to buy at less than 600p.

goldfinger

- 26 Mar 2012 09:13

- 334 of 382

- 26 Mar 2012 09:13

- 334 of 382

Got a banger up its ass this morning, make that a missile.

goldfinger

- 26 Mar 2012 09:36

- 335 of 382

On its way up to resistance at 287p

At this rate it should get through that easy.

just wondering if its been tipped somewhere.

At this rate it should get through that easy.

just wondering if its been tipped somewhere.

goldfinger

- 26 Mar 2012 14:30

- 336 of 382

From T1ps:-

Why we are buying more Avanti Communications*

31 Days ago (2012-02-24 13:33:02)

I met up with Avanti (AVN) the other day and have been pondering this for a while but our SF t1ps Smaller Companies Growth Fund has been nibbling away at the shares and here is why.

I can understand why Evil shorted it. On a current year PE of a zillion or whatever he was able to make a compelling case. It was all the more compelling given that he blinded us with science – a raft of factual inaccuracies. So I just stick to facts.

HYLAS 1 is now in orbit. Capacity is filling up gently and is now, I reckon, at c.40% (of capacity sold). It should be at 50% during this year and will be fully sold out 3 years after launch.

HYLAS 2 launches in June/July. After 3 months of testing it goes operational and is already 10% sold out. Again it will be fully sold out by September 2015.

HYLAS 3 is now fully funded to launch in a couple of years. It should thus be fully sold out by late 2017.

Avanti has fairly fixed PLC costs and so will – by my sums – be at cash breakeven within a couple of months. Thereafter as each month goes by and more capacity is sold on Hylas 1 & 2 (and eventually 3) it just generates more cash. I do not really care what EBITDA is this year to June 30th (I think it will be a tiny positive) or indeed next year or the year after (c.£30 million and c.£80 million is my private forecast). The point is what it should be by, say 2018, when HYLAS 3 is fully operational. I estimate the number then will be c£200 million (earnings per share of c130p!).

At 263p Avanti is capitalised at c£290 million. It has debt (when fully drawn) of c£200 million. So the Enterprise Value is £490 million. By 2018 the company will have chucked off a couple of hundred million pounds of free cashflow and so – were that to be used to repay debt - it would be trading on an EV/EBITDA multiple of 1.5. Now to put that in perspective, Inmarsat, which is today where Avanti will be in five years time, is on a multiple of around 8. That implies a share price in a few years of at least £15 for Avanti.

There are other ways of looking at Avanti which might lead you to expect a £20 share price. I am not sure. But what I do expect is that:

a) Over the next few months there will be a constant diet of announcements on contract wins. The key point is that we are now at inflexion point so that every new contract drops through to the bottom line.

b) We will see some excitement when HYLAS 2 launches in June. This time the directors will not feed the bears by selling shares thereafter.

c) The maths are just compelling and so I really do not give a jot what the share price is next week or next month. We currently have 3% of the growth fund in Avanti and we are increasing that holding with a stream of buys. We are happy to wait.

Why we are buying more Avanti Communications*

31 Days ago (2012-02-24 13:33:02)

I met up with Avanti (AVN) the other day and have been pondering this for a while but our SF t1ps Smaller Companies Growth Fund has been nibbling away at the shares and here is why.

I can understand why Evil shorted it. On a current year PE of a zillion or whatever he was able to make a compelling case. It was all the more compelling given that he blinded us with science – a raft of factual inaccuracies. So I just stick to facts.

HYLAS 1 is now in orbit. Capacity is filling up gently and is now, I reckon, at c.40% (of capacity sold). It should be at 50% during this year and will be fully sold out 3 years after launch.

HYLAS 2 launches in June/July. After 3 months of testing it goes operational and is already 10% sold out. Again it will be fully sold out by September 2015.

HYLAS 3 is now fully funded to launch in a couple of years. It should thus be fully sold out by late 2017.

Avanti has fairly fixed PLC costs and so will – by my sums – be at cash breakeven within a couple of months. Thereafter as each month goes by and more capacity is sold on Hylas 1 & 2 (and eventually 3) it just generates more cash. I do not really care what EBITDA is this year to June 30th (I think it will be a tiny positive) or indeed next year or the year after (c.£30 million and c.£80 million is my private forecast). The point is what it should be by, say 2018, when HYLAS 3 is fully operational. I estimate the number then will be c£200 million (earnings per share of c130p!).

At 263p Avanti is capitalised at c£290 million. It has debt (when fully drawn) of c£200 million. So the Enterprise Value is £490 million. By 2018 the company will have chucked off a couple of hundred million pounds of free cashflow and so – were that to be used to repay debt - it would be trading on an EV/EBITDA multiple of 1.5. Now to put that in perspective, Inmarsat, which is today where Avanti will be in five years time, is on a multiple of around 8. That implies a share price in a few years of at least £15 for Avanti.

There are other ways of looking at Avanti which might lead you to expect a £20 share price. I am not sure. But what I do expect is that:

a) Over the next few months there will be a constant diet of announcements on contract wins. The key point is that we are now at inflexion point so that every new contract drops through to the bottom line.

b) We will see some excitement when HYLAS 2 launches in June. This time the directors will not feed the bears by selling shares thereafter.

c) The maths are just compelling and so I really do not give a jot what the share price is next week or next month. We currently have 3% of the growth fund in Avanti and we are increasing that holding with a stream of buys. We are happy to wait.

goldfinger

- 27 Mar 2012 10:38

- 337 of 382

Brokers seem to be very positive with AVN.

Didnt realise Cenkos had a Buy rating on it.

Avanti Communications Group PLC

FORECASTS 2012 2013

Date Rec Pre-tax (£) EPS (p) DPS (p) Pre-tax (£) EPS (p) DPS (p)

Daniel Stewart

19-03-12 BUY -12.20 -10.30 6.20 5.80

Cenkos Securities

08-03-12 BUY -7.91 -7.90 3.82 0.80

Investec Securities [R]

23-11-11 HOLD -31.95 -35.92 -9.20 -10.34

Growth Equity & Co Research

05-10-11 SBUY 3.30 4.00

2012 2013

Pre-tax (£) EPS (p) DPS (p) Pre-tax (£) EPS (p) DPS (p)

Consensus -11.91 -11.55 3.25 1.60

1 Month Change 0.02 0.04 0.02 0.05

3 Month Change -6.94 -6.18 -11.34 -13.45

GROWTH

2011 (A) 2012 (E) 2013 (E)

Norm. EPS % % %

DPS % % %

INVESTMENT RATIOS

2011 (A) 2012 (E) 2013 (E)

EBITDA £-11.64m £1.11m £34.81m

EBIT £-12.45m £-7.30m £16.40m

Dividend Yield % % %

Dividend Cover x x x

PER -23.08x -23.77x 171.03x

PEG f f f

Net Asset Value PS 244.09p p p

Didnt realise Cenkos had a Buy rating on it.

Avanti Communications Group PLC

FORECASTS 2012 2013

Date Rec Pre-tax (£) EPS (p) DPS (p) Pre-tax (£) EPS (p) DPS (p)

Daniel Stewart

19-03-12 BUY -12.20 -10.30 6.20 5.80

Cenkos Securities

08-03-12 BUY -7.91 -7.90 3.82 0.80

Investec Securities [R]

23-11-11 HOLD -31.95 -35.92 -9.20 -10.34

Growth Equity & Co Research

05-10-11 SBUY 3.30 4.00

2012 2013

Pre-tax (£) EPS (p) DPS (p) Pre-tax (£) EPS (p) DPS (p)

Consensus -11.91 -11.55 3.25 1.60

1 Month Change 0.02 0.04 0.02 0.05

3 Month Change -6.94 -6.18 -11.34 -13.45

GROWTH

2011 (A) 2012 (E) 2013 (E)

Norm. EPS % % %

DPS % % %

INVESTMENT RATIOS

2011 (A) 2012 (E) 2013 (E)

EBITDA £-11.64m £1.11m £34.81m

EBIT £-12.45m £-7.30m £16.40m

Dividend Yield % % %

Dividend Cover x x x

PER -23.08x -23.77x 171.03x

PEG f f f

Net Asset Value PS 244.09p p p

goldfinger

- 28 Mar 2012 09:15

- 338 of 382

AVN

But what I do expect is that:

a) Over the next few months therTom Winnifrith of T1ps.cpom writes: At 275p Avanti is capitalised at c£307 million. It has debt (when fully drawn) of c£200 million. So the Enterprise Value is £507 million. By 2018 the company will have chucked off a couple of hundred million pounds of free cashflow and so – were that to be used to repay debt - it would be trading on an EV/EBITDA multiple of 1.5. Now to put that in perspective, Inmarsat, which is today where Avanti will be in five years time, is on a multiple of around 8. That implies a share price in a few years of at least £15 for Avanti.

There are other ways of looking at Avanti which might lead you to expect a £20 share price. I am not suree will be a constant diet of announcements on contract wins. The key point is that we are now at inflexion point so that every new contract drops through to the bottom line.

b) We will see some excitement when HYLAS 2 launches in June. This time the directors will not feed the bears by selling shares thereafter.

c) The maths are just compelling. I really do not give a jot what the share price is next week or next month. We currently have 3% of the growth fund in Avanti and we are increasing that holding with a stream of buys. We are happy to wait.

Zak writes: It would appear that while the technicals of Avanti in recent weeks have been pointing to the shares hammering out a floor, the end of what has been a relatively cruel pullback for the stock remains a difficult one to call / trade. What helps at the moment is that in addition to the tentative rebound off a falling August support line, there is also clear bullish divergence in the RSI window. On this basis one would suggest that while there is no end of day close back below 240p we can finally look for an initial test of former early December support at 280p.

But what I do expect is that:

a) Over the next few months therTom Winnifrith of T1ps.cpom writes: At 275p Avanti is capitalised at c£307 million. It has debt (when fully drawn) of c£200 million. So the Enterprise Value is £507 million. By 2018 the company will have chucked off a couple of hundred million pounds of free cashflow and so – were that to be used to repay debt - it would be trading on an EV/EBITDA multiple of 1.5. Now to put that in perspective, Inmarsat, which is today where Avanti will be in five years time, is on a multiple of around 8. That implies a share price in a few years of at least £15 for Avanti.

There are other ways of looking at Avanti which might lead you to expect a £20 share price. I am not suree will be a constant diet of announcements on contract wins. The key point is that we are now at inflexion point so that every new contract drops through to the bottom line.

b) We will see some excitement when HYLAS 2 launches in June. This time the directors will not feed the bears by selling shares thereafter.

c) The maths are just compelling. I really do not give a jot what the share price is next week or next month. We currently have 3% of the growth fund in Avanti and we are increasing that holding with a stream of buys. We are happy to wait.

Zak writes: It would appear that while the technicals of Avanti in recent weeks have been pointing to the shares hammering out a floor, the end of what has been a relatively cruel pullback for the stock remains a difficult one to call / trade. What helps at the moment is that in addition to the tentative rebound off a falling August support line, there is also clear bullish divergence in the RSI window. On this basis one would suggest that while there is no end of day close back below 240p we can finally look for an initial test of former early December support at 280p.

goldfinger

- 03 Apr 2012 13:19

- 339 of 382

Appearing now on IG Index broker list

note went out today.......

Avanti Communications Group

ALL-AIM

Communications

Buy

600

257.5

133.0%

Jefferies

600p SP target 133% upside.

note went out today.......

Avanti Communications Group

ALL-AIM

Communications

Buy

600

257.5

133.0%

Jefferies

600p SP target 133% upside.

Shortie - 27 Apr 2012 12:56 - 340 of 382

Seeing some upside today, about time I must say.

humpback321 - 27 Apr 2012 13:03 - 341 of 382

On the run.

goldfinger

- 27 Apr 2012 13:29

- 342 of 382

Up 11% as I post. Nice....very nice.

goldfinger

- 27 Apr 2012 13:39

- 343 of 382

AVN Avanti Screen Media

Brokers Mostly onside

Avanti Communications Group PLC

FORECASTS 2012 2013

Date Rec Pre-tax (£) EPS (p) DPS (p) Pre-tax (£) EPS (p) DPS (p)

Daniel Stewart

23-04-12 BUY -12.20 -10.30 6.20 5.80

Equity Development

27-03-12 None -5.30 -5.70 7.00 6.30

Cenkos Securities

08-03-12 BUY -7.91 -7.90 3.82 0.80

Investec Securities [R]

23-11-11 HOLD -31.95 -35.92 -9.20 -10.34

Growth Equity & Co Research

05-10-11 SBUY 3.30 4.00

2012 2013

Pre-tax (£) EPS (p) DPS (p) Pre-tax (£) EPS (p) DPS (p)

Consensus -10.00 -9.82 4.46 3.13

1 Month Change -0.05 -0.01 0.04 0.06

3 Month Change -5.21 -4.65 -10.23 -12.10

GROWTH

2011 (A) 2012 (E) 2013 (E)

Norm. EPS % % %

DPS % % %

INVESTMENT RATIOS

2011 (A) 2012 (E) 2013 (E)

EBITDA £-12.06m £1.09m £34.82m

EBIT £-12.88m £-7.30m £16.40m

Dividend Yield % % %

Dividend Cover x x x

PER -21.86x -26.49x 83.01x

PEG f f f

Net Asset Value PS 244.09p p p

Brokers Mostly onside

Avanti Communications Group PLC

FORECASTS 2012 2013

Date Rec Pre-tax (£) EPS (p) DPS (p) Pre-tax (£) EPS (p) DPS (p)

Daniel Stewart

23-04-12 BUY -12.20 -10.30 6.20 5.80

Equity Development

27-03-12 None -5.30 -5.70 7.00 6.30

Cenkos Securities

08-03-12 BUY -7.91 -7.90 3.82 0.80

Investec Securities [R]

23-11-11 HOLD -31.95 -35.92 -9.20 -10.34

Growth Equity & Co Research

05-10-11 SBUY 3.30 4.00

2012 2013

Pre-tax (£) EPS (p) DPS (p) Pre-tax (£) EPS (p) DPS (p)

Consensus -10.00 -9.82 4.46 3.13

1 Month Change -0.05 -0.01 0.04 0.06

3 Month Change -5.21 -4.65 -10.23 -12.10

GROWTH

2011 (A) 2012 (E) 2013 (E)

Norm. EPS % % %

DPS % % %

INVESTMENT RATIOS

2011 (A) 2012 (E) 2013 (E)

EBITDA £-12.06m £1.09m £34.82m

EBIT £-12.88m £-7.30m £16.40m

Dividend Yield % % %

Dividend Cover x x x

PER -21.86x -26.49x 83.01x

PEG f f f

Net Asset Value PS 244.09p p p

goldfinger

- 27 Apr 2012 15:20

- 344 of 382

AVN Avanti Screen Media

Technicals point of view now.

It has broken out above prior resistance.

Technicals point of view now.

It has broken out above prior resistance.

humpback321 - 02 May 2012 13:09 - 345 of 382

Onwards and upwards.

Davai - 02 May 2012 19:17 - 346 of 382

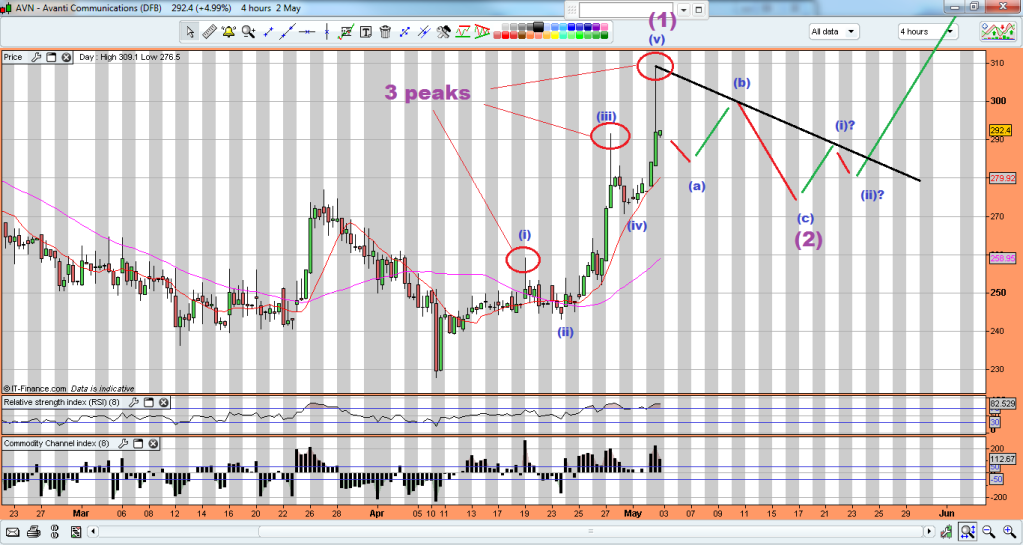

Noticed this one after GF flagged the rise on the 27th. Thought i would post my thoughts on here as its one i will now watch myself. I don't know the first thing about the company so this is purely a charting perspective, but it looks like having completed an impulsive move. I would expect a bit of chop for a few days, while it pulls back correctively in 3 waves where i hope it will form a flagline, look for a minor 'i'&'ii' to confirm the drop has finished and/or a break of the flagline for a big move up to follow.

As i said, purely speculative according to how i see the chart;

As i said, purely speculative according to how i see the chart;

Shortie - 03 May 2012 10:00 - 347 of 382

My long spread off 263 now looking rather nice. 250 support did hold as suspected. I'd add another line to the above chart, 27th March, 27th April joined and through to cross roughly in where (ii)? cross sits. I see this as being the start of the new trend line higher.

ahoj

- 03 May 2012 10:03

- 348 of 382

Are they going to launch another satellite?

Shortie - 03 May 2012 10:08 - 349 of 382

ahoj

- 08 May 2012 10:11

- 350 of 382

I wish I held my shares. Sold 6K at 314 last week!!!

humpback321 - 08 May 2012 10:29 - 351 of 382

Share price continues to advance ahead of second satallite launch 30th. of june.

Shortie - 08 May 2012 11:45 - 352 of 382

Sold at 346, nice profit made.

dreamcatcher

- 15 May 2012 21:35

- 353 of 382

..Questor share tip: Avanti orbit looks inviting as satellite launch approaches

By Garry White | Telegraph – 14 hours ago

Shares in satellite group Avanti Communications have plunged over the past year and many investors are sitting on losses. What should Questor readers do next?

Avanti Communications 313¾p -14 ¼p Questor says BUY

Avanti sells satellite broadband services to telecoms providers, which then resells the service to households and businesses.

The company's first satellite, HYLAS 1, launched in November (Stuttgart: A0Z24E - news) 2010, is the first superfast broadband satellite launched in Europe (Chicago Options: ^REURUSD - news) .

Avanti's second satellite, called HYLAS 2, is fully funded and is scheduled for launch in the next few months. This satellite will extend Avanti's coverage to Africa and the Middle East.

The third satellite, HYLAS 3, is currently in the design phase, but this is also fully funded to launch.

Things have been going reasonably well at the group as a trading update released yesterday showed but the shares took a bath last year on negative sentiment.

The company was subject to what is known as a "bear raid". A high profile City player took a significant short position in the shares and then proceeded to make this fact known to the market.

Also last year, broker Numis had to issue an apology after publishing misleading statements about the group relating to contracts signed with clients.

"Numis has raised doubts about the contract Avanti Communications has signed with TigrisNet in widely distributed emails and conversations. Numis apologises if the previous communication led to a misunderstanding," the City broker said.

Unfortunately, mud sticks. This sort of thing can become a self-fulfilling prophecy and the share price has sunk. However, what is more important now is the future.

The company has undertaken a fund-raising and needs to raise no more cash to complete its launch plans. Indeed, at the interim stage Avanti had £26m of cash on its balance sheet. The launch of HYLAS 2, which will happen in a 30-day window from June 30, should be the next positive catalyst going forward. The group also plans to move from Aim to a full listing next year.

Avanti confirmed that in the four-month period to April 30 it had added £42.3m of backlog. These are contracts signed for bandwidth on both HYLAS 1 and 2. This brought the total backlog to £213m and Avanti said its pipeline of potential sales stood at £529m.

The company needs to make about £11m of sales each month to meet its target of filling capacity on HYLAS 1 by 2014 and HYLAS 2 by 2016. The figures indicate it is on track to do just that.

The company is currently loss-making, but it is expected to move into profit next year, with earnings rising quickly thereafter. The 2013 multiple is a very heady 163 times, but this falls to 9.3 in 2014 and just 4.4 in 2015.

The shares were first recommended on January 8, 2010, at 467½p and they are now down 33pc compared with a market up 1pc. The shares have drifted from a high of 735p. Questor noted that the investment could be very volatile and it was "not one on which to bet the farm" and that view still stands. The shares are now looking pretty cheap, should the group manage to fill all of its satellites. City analysts have some pretty punchy targets, with the average of the three analysts monitored by Bloomberg being £16.50, a staggering 430pc above the current levels.

Questor maintains a buy stance and looks forward to the launch of HYLAS 2 as the next major catalyst.

..

By Garry White | Telegraph – 14 hours ago

Shares in satellite group Avanti Communications have plunged over the past year and many investors are sitting on losses. What should Questor readers do next?

Avanti Communications 313¾p -14 ¼p Questor says BUY

Avanti sells satellite broadband services to telecoms providers, which then resells the service to households and businesses.

The company's first satellite, HYLAS 1, launched in November (Stuttgart: A0Z24E - news) 2010, is the first superfast broadband satellite launched in Europe (Chicago Options: ^REURUSD - news) .

Avanti's second satellite, called HYLAS 2, is fully funded and is scheduled for launch in the next few months. This satellite will extend Avanti's coverage to Africa and the Middle East.

The third satellite, HYLAS 3, is currently in the design phase, but this is also fully funded to launch.

Things have been going reasonably well at the group as a trading update released yesterday showed but the shares took a bath last year on negative sentiment.

The company was subject to what is known as a "bear raid". A high profile City player took a significant short position in the shares and then proceeded to make this fact known to the market.

Also last year, broker Numis had to issue an apology after publishing misleading statements about the group relating to contracts signed with clients.

"Numis has raised doubts about the contract Avanti Communications has signed with TigrisNet in widely distributed emails and conversations. Numis apologises if the previous communication led to a misunderstanding," the City broker said.

Unfortunately, mud sticks. This sort of thing can become a self-fulfilling prophecy and the share price has sunk. However, what is more important now is the future.

The company has undertaken a fund-raising and needs to raise no more cash to complete its launch plans. Indeed, at the interim stage Avanti had £26m of cash on its balance sheet. The launch of HYLAS 2, which will happen in a 30-day window from June 30, should be the next positive catalyst going forward. The group also plans to move from Aim to a full listing next year.

Avanti confirmed that in the four-month period to April 30 it had added £42.3m of backlog. These are contracts signed for bandwidth on both HYLAS 1 and 2. This brought the total backlog to £213m and Avanti said its pipeline of potential sales stood at £529m.

The company needs to make about £11m of sales each month to meet its target of filling capacity on HYLAS 1 by 2014 and HYLAS 2 by 2016. The figures indicate it is on track to do just that.

The company is currently loss-making, but it is expected to move into profit next year, with earnings rising quickly thereafter. The 2013 multiple is a very heady 163 times, but this falls to 9.3 in 2014 and just 4.4 in 2015.

The shares were first recommended on January 8, 2010, at 467½p and they are now down 33pc compared with a market up 1pc. The shares have drifted from a high of 735p. Questor noted that the investment could be very volatile and it was "not one on which to bet the farm" and that view still stands. The shares are now looking pretty cheap, should the group manage to fill all of its satellites. City analysts have some pretty punchy targets, with the average of the three analysts monitored by Bloomberg being £16.50, a staggering 430pc above the current levels.

Questor maintains a buy stance and looks forward to the launch of HYLAS 2 as the next major catalyst.

..

| About MoneyAM | Ts and Cs | Privacy Policy | Investment Warning | Content Standards | Corporate Solutions | Advertise With Us | Site Map | © 2026 MoneyAM |

Register now for FREE

Share Prices,

Stock Quotes,

Charts, Bulletin Boards, Indices, Watchlists, Portfolio, Market News, Research

or see our Premium Services including Level 2, Terminal and much more.